IES Holdings Advances with Q2 Profit Growth Despite Cyclical Headwinds and Fixed-Price Contract Risks

Q2 2026 results highlight operational progress and margin resilience within IES Holdings’ diversified industrial services portfolio.

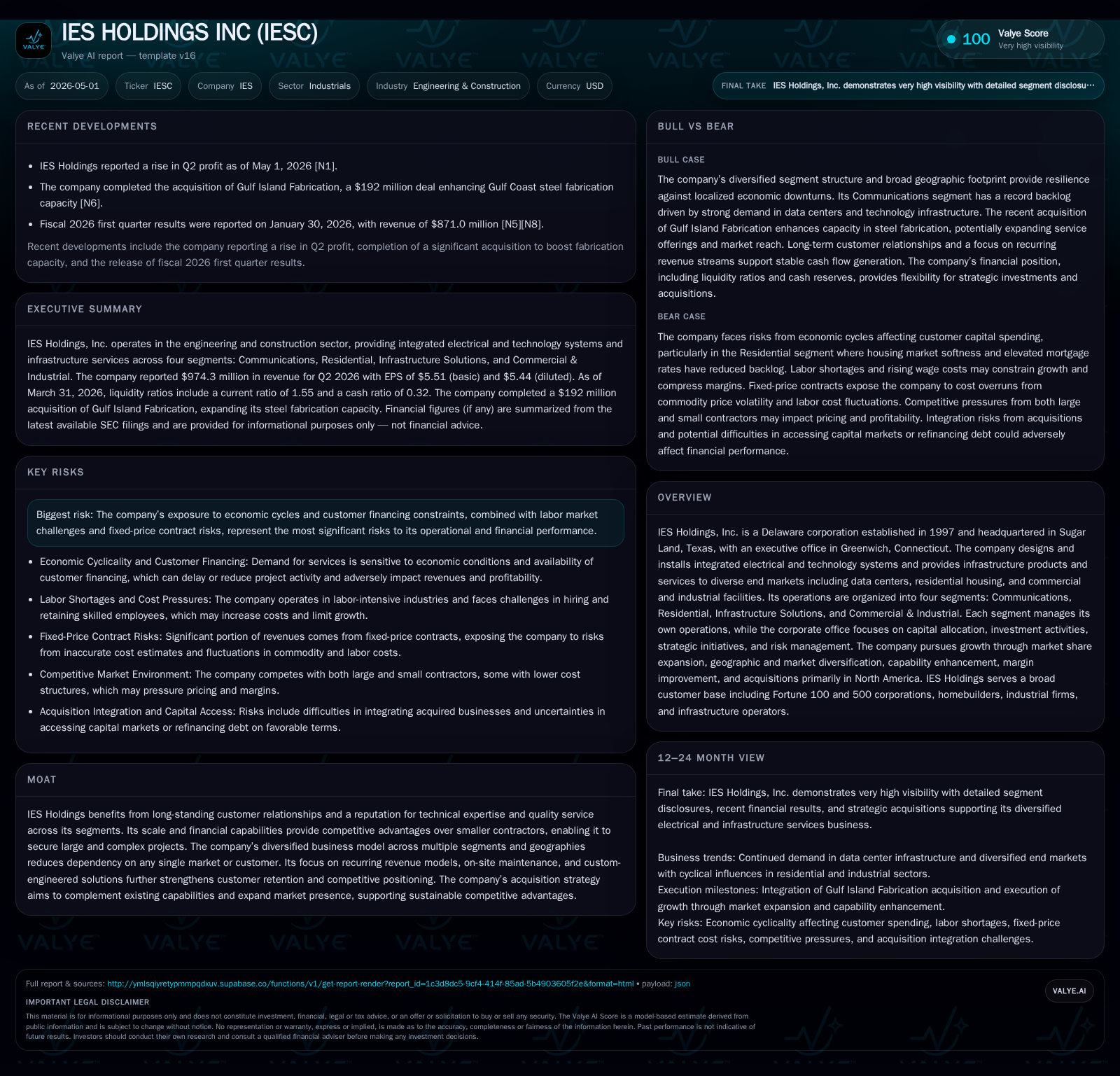

IES Holdings reported improved profitability in its fiscal 2026 second quarter, emphasizing the strength of its diversified segments and disciplined capital allocation. The company’s business model spans communications, residential, infrastructure solutions, and commercial industrial services, leveraging technical expertise and recurring revenue to offset cyclical softness in key markets. Competitive advantages stem from scale, longstanding customer relationships, and a strategic acquisition approach. Risks remain from economic cyclicality, fixed price contracts, and labor constraints, but recent execution reflects solid backlog and margin management.

Recent Operating Update: Q2 Fiscal 2026

In its May 1, 2026 quarterly filing (Form 10-Q), IES Holdings disclosed an earnings improvement for the second quarter of fiscal year 2026, underscoring ongoing demand for its integrated electrical and technology system installation services alongside infrastructure product offerings across multiple segments [S2][S3][N2]. This operating update reflects progress despite cyclical headwinds faced particularly in the Residential segment due to persistent housing affordability challenges tied to elevated mortgage rates.

The company reaffirmed no material changes to risk factors disclosed in the previous annual report (10-K), signaling stable operating conditions albeit within a competitive and economically sensitive environment [S28]. The quarterly presentation posted publicly details segment-level backlog strength especially within Communications and Infrastructure Solutions, supporting medium-term revenue visibility despite some near-term variability in project timing.

Business Model

IES Holdings operates through four distinct yet synergistic segments:

Communications: Nationwide provider specializing in design, build, and maintenance of network infrastructure primarily for data centers hosting large-scale corporate clients. This segment captures recurring revenues through on-site maintenance contracts while engaging in complex build-outs driven by data consumption trends [S1][S4][S21].

Residential: Regional electrical installation services focused on single-family homes and multi-family complexes augmented by expansions into HVAC and plumbing installations. Revenue here is sensitive to seasonal construction cycles and general housing market dynamics primarily in Texas, Florida, Midwest, Mid-Atlantic, and Southeast regions [S1][S11][S23].

Infrastructure Solutions: Offers electro-mechanical industrial solutions including manufacturing custom-engineered generator enclosures and power distribution equipment alongside maintenance and repair services. This segment's project timing influences quarterly results due to variable capital spending cycles in heavy industrial customers [S1][S12][S15].

Commercial & Industrial: Provides full-service electrical/mechanical design, construction, and maintenance across commercial buildings (data centers, healthcare facilities) and industrial sectors such as power generation. It combines recurrent service contracts with long-duration construction projects spanning various U.S. regions [S1][S7][S13].

The company’s model generates revenues predominantly through fixed-price contracts which require meticulous cost estimation for labor and commodities. Recurring revenue is bolstered by maintenance agreements which provide steady cash flow even during downturns. Customers range from Fortune-level corporations in telecom/data centers to regional builders in residential markets.

Revenue Drivers Mechanics

Revenue depends on the volume of projects initiated or maintained in each segment:

- In Communications, growth correlates with data center construction trends and digital infrastructure investment.

- Residential revenues follow housing start rates influenced by mortgage rates and credit availability.

- The Infrastructure Solutions segment’s revenue is tied to industrial capital expenditure cycles relevant to sectors like petrochemical or energy utilities.

- Commercial & Industrial depends heavily on regional construction activity including new builds or retrofits in commercial/industrial facilities.

Margins are affected by contract mix (fixed vs service), commodity pricing volatility (copper wire, steel), labor costs, subcontractor efficiency, and project execution capabilities.

Industry Structure and Competitive Position

The industries served by IES Holdings are inherently fragmented with numerous small to medium-sized contractors competing locally alongside a few large public players. Fragmentation results from relatively low barriers to entry in electrical contracting; however, larger firms like IES benefit from:

- Scale enabling participation in large/complex projects requiring significant financial capacity.

- Technical expertise that supports engineering-heavy service offerings particularly in data center communications.

- Long-term customer relationships fostering preferred supplier status enhancing repeat business.

- Geographic diversification mitigating localized demand swings.

- Acquisition strategy targeting complementary businesses increasing market presence without substantial integration risk [S5][S14][S26].

Competitors often have narrower service offerings or limited access to capital compared to IES’s broad platform covering tech infrastructure to residential HVAC/plumbing expansions. The company's reputation for quality service builds switching costs particularly among mission critical facility clients.

Growth Drivers

Several key drivers underpin IES Holdings’ potential expansion:

- Data Center Investment Growth: The expanding need for robust communications infrastructure supports recurring service contracts as well as new build work within the Communications segment.

- Diversification of Residential Services: Expanding beyond electrical into HVAC/plumbing taps additional market demand areas with cross-selling opportunities.

- Infrastructure Modernization Trends: Industrial customers needing electro-mechanical upgrades or repairs present steady demand for Infrastructure Solutions.

- Strategic Acquisitions: Ongoing acquisitions focused on geographic expansion or adding technological capabilities reinforce organic growth while enhancing margins.

- Recurring Revenue Focus: Increasing maintenance/service contract penetration stabilizes cash flows reducing sensitivity to project timing volatility.

- Technological Integration Offering: Continued enhancement as integrators for building technology (e.g., distributed antenna systems) creates differentiation especially in commercial end-markets.

Risks / Watchpoints / Growth Constraints

Operational risks clouding IES Holdings’ outlook include:

- Economic Cyclicality: Demand correlates closely with national/regional economic conditions impacting construction volumes across all segments but notably Residential.

- Fixed Price Contract Exposure: Material/labor cost inflation can compress margins if not fully covered by contract escalators leading to unexpected losses.

- Labor Market Challenges: Skilled labor shortages raise costs or delay project delivery impairing profitability.

- Supply Chain Volatility: Lengthening lead times for key materials can disrupt schedules creating inefficiencies.

- Customer Concentration: While no single customer dominates total revenues, dependence on large accounts per segment creates exposure if such clients reduce capital budgets.

- Regulatory Compliance Costs: Multi-state footprint entails complex licensing/regulatory adherence adding operational overhead.

- Competitive Pricing Pressure: Fragmented industry structure means price competition remains intense potentially pressuring margins if quality differentiators weaken.

Monitoring commodity price inflation protections embedded within contracts remains critical given significant copper/steel/materials input exposure.

What to Watch Next

Key markers for future performance clarity include:

- Backlog trends across Communications and Infrastructure Solutions indicating sustained demand levels post Q2 earnings announcement.

- Execution on planned geographic/service expansions particularly launch of new HVAC/plumbing operations beyond current markets.

- Updates on acquisition completions expanding niche technological capabilities or regional presence.

- Quarterly service contract renewal rates confirming stability of recurring revenue streams.

- Customer capital spending patterns amid macroeconomic uncertainty influencing Residential order flow.

- Management commentary on margin outlook vis-à-vis inflationary pressures impacting fixed-price contracting profitability.

Financial Profile Summary

Latest financial snapshot

| Metric | Value | Period |

|---|---|---|

| Cash & equivalents | $48.7 M | |

| 2026-03-31 | ||

| Total debt | $0 | |

| 2025-12-31 | ||

| Net debt | -$48.7 M | |

| 2025-12-31 | ||

| Current assets | $1.29 B | |

| 2026-03-31 | ||

| Current liabilities | $833 M | |

| 2026-03-31 | ||

| Current ratio | 1.55 | |

| 2026-03-31 |

Source: SEC companyfacts cache [F1].

As of March 31, 2026, IES Holdings maintains a strong liquidity position highlighted by $48.7 million in cash equivalents against current liabilities of $833 million resulting in a current ratio of approximately 1.55 supporting working capital needs [F1]. Available data indicates zero reported debt as of December 31, 2025 yielding a net cash balance favorable for funding acquisitions as part of the growth strategy without near-term refinancing pressures [F1].

Profitability metrics from the latest annual data show operating income at $383.5 million on $3.37 billion revenue basis illustrating mid-single digit operating margins consistent with an engineering-heavy contracting business model requiring capital deployment efficiency [F1].

Its strategic emphasis on acquiring complementary businesses combined with expansion into adjacencies such as HVAC bolster growth levers while recurring maintenance contracts shore up revenue stability. Investors watching cyclical industry players will find value in monitoring backlog progression across its technically demanding Communications segment alongside cost discipline under volatile commodity environments influencing fixed price contracts.

This analysis is based solely on publicly available information as of May 1, 2026 including SEC filings and does not constitute investment advice or a recommendation regarding securities buying or selling decisions.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments