Fast Casual Concepts Shifts to Marketing Services with AI Integration Facing Intensifying Competition

FCCI recently completed its first quarter post-pivot to marketing services, highlighting modest revenue and liquidity challenges amid fierce agency competition.

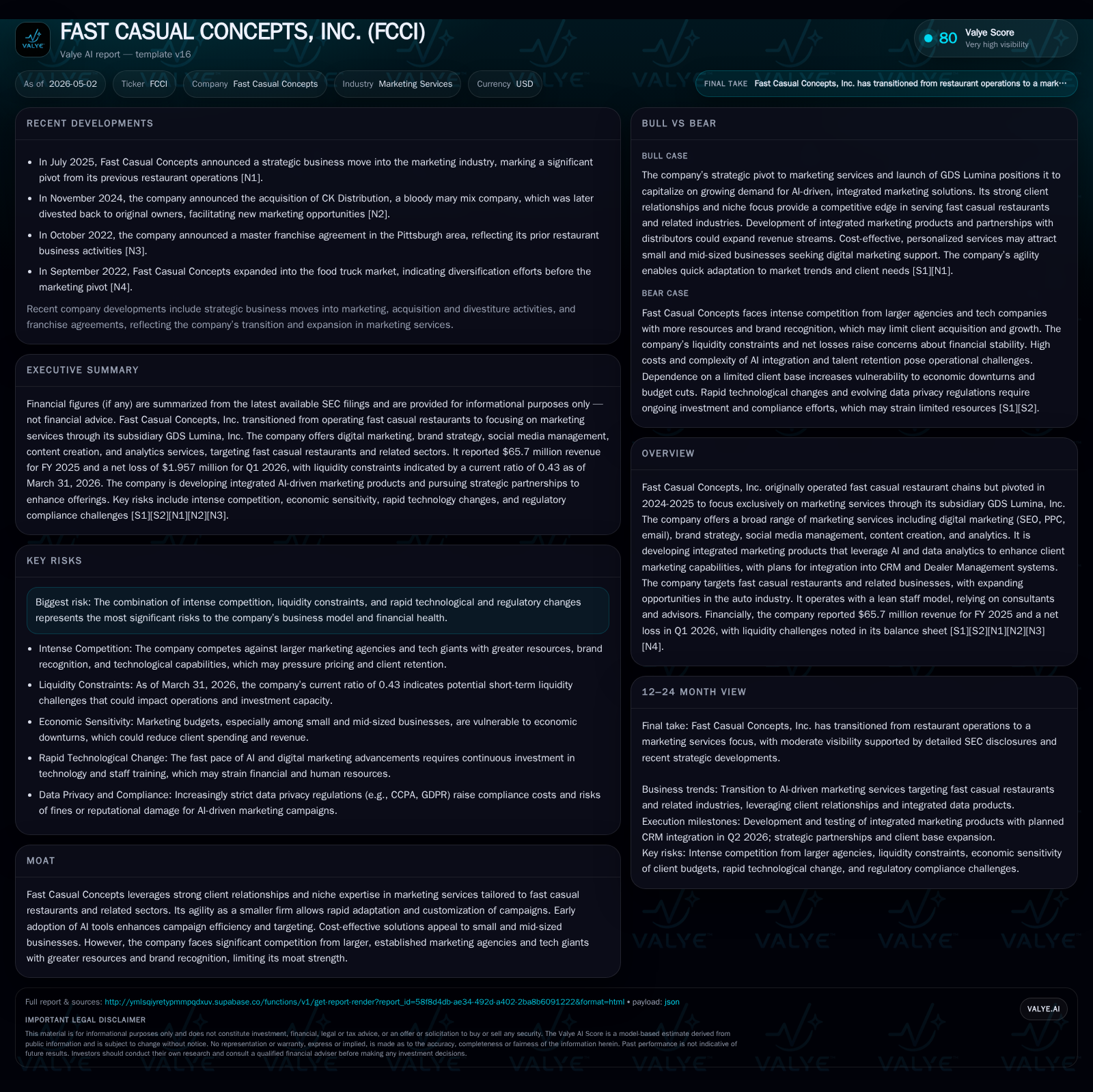

Fast Casual Concepts, Inc. has fully exited its original fast casual restaurant operations to focus exclusively on marketing services through its subsidiary GDS Lumina, Inc., targeting fast casual chains and adjacent sectors. The latest 10-Q reveals ongoing operating losses and a current ratio below 0.5, signaling liquidity pressure as it invests in AI-enabled integrated marketing solutions. While leveraging its niche expertise and client relationships provides some differentiation, the company confronts significant competitive headwinds from large digital agencies and tech giants. Key growth drivers include expanding into auto industry marketing and embedding AI analytics into CRM/Dealer Management platforms. Watch for client acquisition metrics, product integration progress, and quarterly cash flow improvements as near-term milestones.

Recent Operating Update

Fast Casual Concepts, Inc. (FCCI) reported its latest quarterly results on May 1, 2026 via Form 10-Q [S2], reinforcing its strategic pivot concluded by the end of 2025. The company transitioned away from direct fast casual restaurant operations and now exclusively offers marketing services through its wholly owned subsidiary GDS Lumina, Inc. The recent filings disclose no material legal proceedings but highlight ongoing financial pressures including a net loss position in Q1 2026 despite generating full-year revenues of about $65.7 million in calendar year 2025 [F1]. Notably, the balance sheet evidences working capital constraints with current assets roughly $15.9 million against current liabilities of $37.2 million as of March 31, reflecting a sub-0.5 current ratio (approx 0.43) indicative of tight liquidity headroom [F1]. This financial snapshot aligns with the company’s stated intention to invest heavily in developing integrated AI-driven marketing solutions designed for their core client base.

Business Model and Service Offering

Originally formed to operate fast casual restaurant chains such as Holy Cow Burgers and Ice Cream as well as Independent Taco and Third Eye Pies [S1], FCCI underwent a major strategic transformation during 2024-2025. The firm divested restaurant operations to concentrate entirely on delivering advanced digital marketing services aimed at fast casual food businesses alongside a growing footprint in automotive dealership marketing.

The core business is conducted via GDS Lumina, which provides a range of marketing capabilities:

- Digital advertising services including paid search (PPC) and search engine optimization (SEO)

- Email marketing campaigns and customer engagement tools

- Social media content creation and channel management

- Brand strategy consulting

- Data analytics incorporating artificial intelligence methods aiming to optimize campaign targeting and improve return-on-investment metrics

Importantly, FCCI is investing to integrate these offerings into broader customer relationship management (CRM) systems and Dealer Management Systems (DMS), particularly for automotive clients where cross-platform data aggregation can unlock enhanced insights.

Revenue generation primarily comes from service fees charged to clients on contracts likely combining retainer-based access plus performance-linked components keyed to campaign outcomes or volume thresholds. Margins depend heavily on the balance between labor costs (outsourced consultants/advisors vs direct employees), technology investments (AI development), and scale economies achieved by broad adoption.

Industry Structure and Competitive Position

Digital marketing is a fragmented industry with dominant large players such as Ignite Visibility and Merkle commanding substantial market share through scale advantages and broad capability portfolios [S1]. Additionally, major technology firms now embed AI-driven marketing automation tools directly accessible by clients themselves or via premium partnerships intensifying competitive pressure.

For FCCI—positioned as a smaller player specializing historically in fast casual dining chains’ marketing—the transition represents both an opportunity and challenge. Its competitive moat derives mainly from:

- Deep sector-specific knowledge enabling tailored campaigns over generic agency offerings

- Established client relationships built during restaurant ownership phase providing an entry point into targeted engagements

- Agility of a lean organizational structure that can customize solutions quickly relative to cumbersome larger competitors

- Early incorporation of AI analytics enhancing targeting precision beyond standard campaign management software

However:

- Scale remains limited relative to larger agencies able to amortize expensive technology infrastructure investments across many clients

- Customer switching costs are moderate; clients may migrate toward bundled offerings or proprietary tools offered by bigger firms or tech vendors

- Marketing budget volatility in fast casual restaurants tied partly to discretionary consumer spending suggests potential cyclical revenue swings

Growth Drivers

Several factors underpin FCCI’s pathway toward growth:

Client Expansion: Leveraging its foundational restaurant sector relationships while expanding aggressively into automotive dealership networks represents an addressable market expansion with significant upside.

AI & Data Integration: Development of proprietary AI-powered analytics embedded within CRM/DMS workflows promises differentiated value-add through real-time insights driving better campaign outcomes—a timely advantage given industry-wide push for data-driven decisions.

Service Diversification: Beyond traditional digital ads and social media management, adding brand strategy consulting positions FCCI higher up the value chain capturing greater wallet share per client engagement.

Consultant Model Flexibility: A lean core team supplemented by specialists affords rapid scaling capability without proportionate fixed cost increases enhancing margin potential when volumes grow.

Cross-Selling Opportunities: Integrated offerings combining digital content creation with analytics may stimulate upselling through bundled contracts strengthening client lock-in.

Risks and Watchpoints

Several operational hazards may constrain FCCI’s prospects:

Liquidity Constraints: Current ratio below 0.5 warns near-term cash flow stress requiring prudent working capital management or potential financing to fund growth investments.[F1]

Intense Competition: Larger agencies wield significant resource advantages including branded AI tooling threatening FCCI’s pricing power unless differentiation is pronounced.[S1]

Technology Pace: Rapid advances in AI capabilities necessitate continuous R&D outlays; failure to maintain innovation pace risks obsolescence.

Client Concentration / Retention: Reliance on niche segments implies vulnerability if major clients reduce budgets or defect.

Regulatory Environment: Potential changes around digital advertising regulations might affect some service lines especially regarding data privacy standards impacting analytics usage.

What to Watch Next

Key indicators for monitoring FCCI’s trajectory include:

- Quarterly revenue trends gauging customer acquisition velocity beyond initial pivot year results.

- Client bookings growth particularly within the automotive vertical demonstrating successful sector expansion.

- Progress reports or announcements concerning AI product deployment timelines integrated with CRM/DMS platforms validating strategic roadmap execution.

- Operating cost leverage improvements signifying scaling efficiency gains amid lean consultant-heavy model.

- Updates in risk disclosures or liquidity management signaling whether short-term financial risks are being mitigated effectively.

- Any shift in guidance or commentary from management providing clarity around anticipated profitability timeline or new market entries.

Financial Profile Summary

Latest financial snapshot

| Metric | Value | Period |

|---|---|---|

| Current assets | $15903 | |

| 2026-03-31 | ||

| Current liabilities | $37195 | |

| 2026-03-31 | ||

| Current ratio | 0.43x | |

| 2026-03-31 |

Source: SEC companyfacts cache [F1].

The most recent fiscal data available covers the full year ended December 31, 2025 plus Q1 ending March 31, 2026 quarter data [F1][S2]:

The financials reflect a nascent services company still transitioning income streams post-pivot with minimal debt but tight liquidity due to elevated current liabilities relative to cash equivalents. Slight positive net income for FY 2025 indicates early stabilization but operating losses persist pointing toward ongoing R&D/marketing investments dampening profitability meanwhile.

Conclusion

Fast Casual Concepts has undertaken a decisive shift away from its original restaurant operation model toward becoming a specialized marketing services provider focused on digitally-enabled solutions powered by AI analytics targeting fast casual dining and automotive sectors. This repositioning leverages legacy client relationships combined with emerging tech capabilities but places FCCI in an intensely competitive environment dominated by larger agencies augmented by tech giants embedding AI at scale.

While growth opportunities appear multi-dimensional—centered around platform integration, market expansion into dealerships, and enhanced service bundles—the company must manage liquidity constraints closely while proving scalable margins amid fierce price competition. Execution discipline around technology deployment and client retention will be critical factors shaping whether FCCI can emerge as a viable midsized player or remain challenged by structural market pressures inherent in digital marketing today.

This analysis is based solely on public SEC filings dated through May 1, 2026 ([S1],[S2]) supplemented with validated financial metrics ([F1]) without speculative forecasts or investment recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments