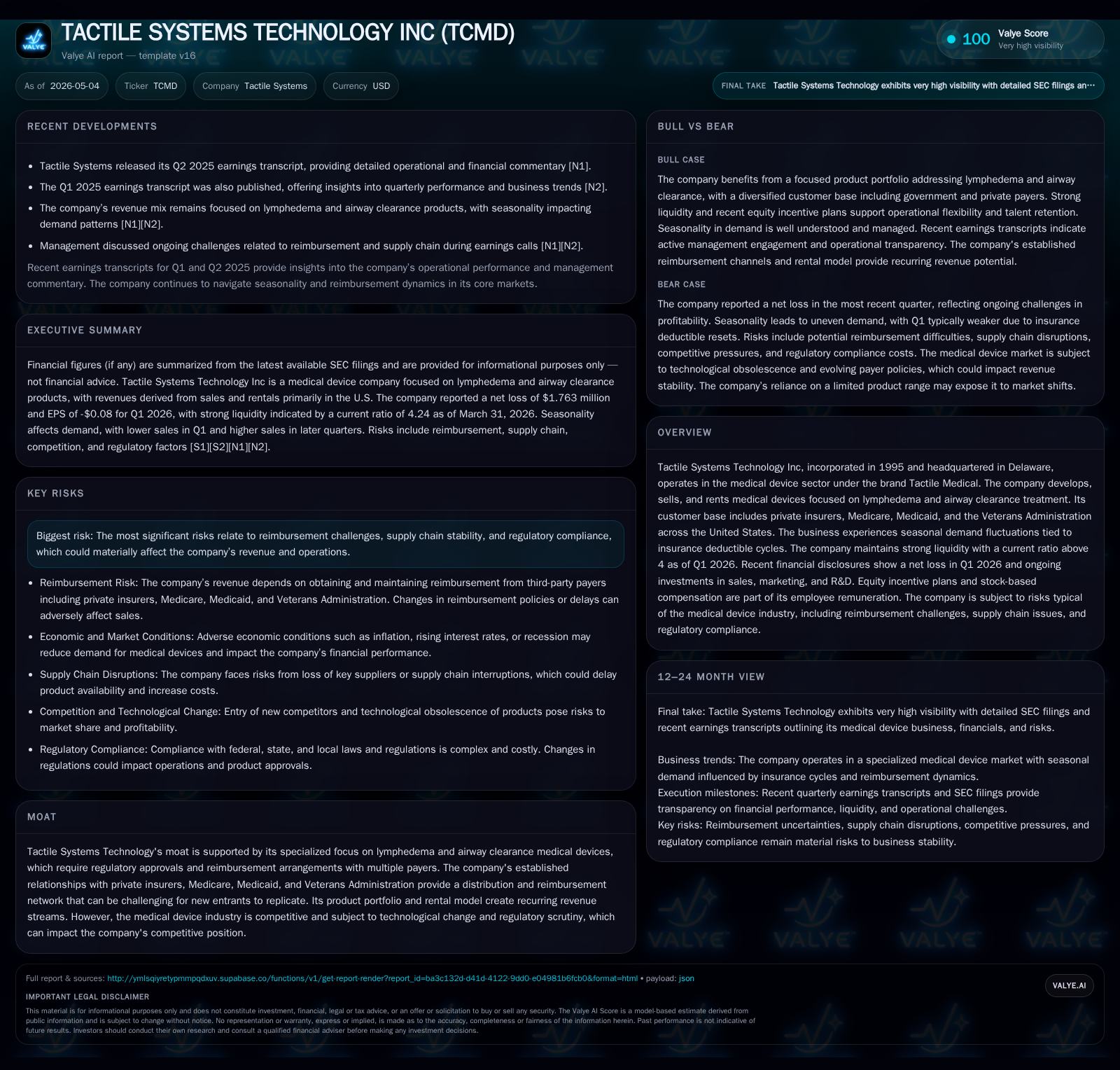

Tactile Systems Advances with Rental Growth and Strong Liquidity Amid Narrowing Net Loss in Q1 2026

Q1 2026 showed meaningful sales revenue growth and stable rentals for Tactile Systems Technology, while maintaining robust liquidity and modest net losses.

Tactile Systems Technology (TCMD) reported solid quarterly revenue growth driven by sales increases, offsetting a slight decline in rental revenue in Q1 2026. The company continues investing in sales, marketing, and R&D to expand its niche medical device offerings targeting lymphedema and airway clearance therapies. Its balance sheet remains strong with no debt and cash reserves exceeding $74 million, supporting ongoing share repurchases. While the business benefits from payer relationships and recurring rental streams, reimbursement and regulatory risks persist as watchpoints.

Recent Operating Update: Q1 2026 Highlights

In its latest quarterly filing ending March 31, 2026 ([S2], [S3]), Tactile Systems Technology reported total revenue of $75.3 million, marking a robust increase from the $61.3 million recorded a year earlier. This growth was primarily fueled by an increase in sales revenue to nearly $67 million — a gain of roughly 28% year-over-year — while rental revenue saw a modest contraction to $8.3 million from $8.8 million the prior year [S2],[S15].

Gross profit expanded accordingly to $57.6 million, yet rising operating expenses—up from about $49.9 million to $59.1 million—led to an operating loss of approximately $1.5 million, an improvement compared to the prior year’s operating loss of about $4.5 million [S2],[S15]. Despite increased investments particularly in sales & marketing (up roughly 19%) and R&D (up nearly 60%), these efforts have yet to return the company to profitability in the quarter.

Net loss narrowed significantly to around $1.76 million versus a loss near $2.97 million last year [S2],[S15]. Favorable variances included lower interest expense ($28k vs. $424k) thanks to elimination of term loan borrowings [F1],[S22], partially offset by income tax expense reversing from a small benefit last year.

Liquidity remains a highlight; cash & equivalents totaled almost $75 million at quarter end with zero outstanding debt under its credit agreements as per disclosures ([F1],[S22]). The company also actively repurchased shares during Q1 totaling about 40k shares at ~$26.67 average cost per share with approximately $24 million still authorized for buybacks [S2],[S18].

Business Model: Specialized Device Sales Plus Recurring Rentals

Tactile Systems operates within the niche medical device segment under the Tactile Medical brand primarily targeting lymphedema management and airway clearance therapies ([S1]). The company derives revenue through two complementary channels:

- Sales Revenue: One-time device purchases primarily driven by healthcare providers or patients covered by private insurers or government programs.

- Rental Revenue: Recurring charges for devices used over extended periods, creating predictable cash flow.

This dual revenue stream supports margin stability; sales generate upfront gross profit while rentals ensure long-term recurring income contributing positively after initial capital recovery due to maintenance fees embedded in rental pricing [S1],[S15].

The company's customers include major US payers such as Medicare, Medicaid, Veterans Administration alongside private insurance plans ([S1]). As reimbursement policies remain critical drivers of patient access and adoption rates, managing payer relationships forms a competitive barrier difficult for new entrants given regulatory hurdles.

Investments funnel heavily into sales & marketing aimed at expanding payer coverage acceptance among clinicians and educating end-users about therapeutic benefits ([S2]). Ongoing research & development focuses on upgrading device functionality and compliance with evolving FDA standards which may affect approval timelines but are necessary for sustained product relevance.

Industry Structure and Competitive Position

Operating within the broader durable medical equipment (DME) sector but specializing in lymphedema and airway clearance niches allows Tactile Systems carving out defensible market segments ([S1]). Key structural features supporting its position include:

- Complex regulatory environment necessitating FDA clearances that constrain easy market entry.

- Intricate reimbursement landscape involving multiple governmental payers requiring contract negotiations.

- Established relationships with distribution networks that integrate devices into care management plans.

- A sizable installed base benefiting from switching costs due to familiarization with protocols and ease of use.

- Rental model offering differentiation versus competitors focused solely on outright sales.

However, competitive threats persist from larger diversified med-tech companies offering alternative therapies or lower-cost devices potentially pressuring pricing or market share ([S1],[N8]). Technological innovation cycles require ongoing R&D investment which can strain margins especially if reimbursement policies shift unfavorably.

Growth Drivers

Several factors underpin Tactile System’s growth trajectory:

- Expanding Insurance Coverage: Incremental addition of insurers adopting reimbursement for lymphedema/airway clearance devices helps drive volumes.

- Aging Population: Rising incidence of chronic conditions like cancer-related lymphedema amplifies demand over longer horizon.

- Customer Education & Sales Penetration: Enhanced clinician engagement improves treatment adoption rates accelerating device placements.

- Product Innovation: Newer generations of more effective or user-friendly devices can unlock incremental market demand or premium pricing tiers.

- Optimizing Rental Utilization: Better customer retention on rentals translates into steadier recurring revenues reflecting in improved lifetime value metrics.

Seasonal demand patterns tied to patient insurance deductible resets imply some volatility quarter-to-quarter necessitating proactive sales cadence strategies ([S1]).

Risks / Watchpoints / Growth Constraints

Key risks that could temper upside include:

- Reimbursement Changes: Any adverse adjustments by Medicare/Medicaid affecting coverage or payment rates could materially hit revenues given reliance on government payers.

- Supply Chain Disruptions: Dependency on component suppliers means production bottlenecks could delay shipments impacting customer satisfaction.

- Regulatory Hurdles: Failure or delay obtaining FDA clearances on product enhancements risks technology obsolescence against rivals.

- Pricing Pressure: Increased competition potentially compressing margins leading to profitability challenges given fixed R&D & SG&A costs.

- Seasonality Impact: Insurance deductible timing influencing buying cycles calls for agile operational planning to manage working capital effectively.

Management's continued investment despite near-term losses signals commitment but execution risk remains elevated while balancing growth investments against cost control ([S2]).

What To Watch Next

Key developments that will illuminate future prospects include:

- Quarterly bookings or order backlog disclosures indicating sustainability of sales momentum.

- Updates on reimbursement policy shifts from CMS or large private carriers impacting demand visibility.

- Product launch announcements evidencing R&D pipeline productivity driving competitive differentiation.

- Execution on share repurchase programs providing insight into capital return priorities alongside cash flow generation strength.

- Any commentary around supply chain resilience strategies amid inflationary pressures or geopolitical uncertainties affecting sourcing.

- Trending net margin improvements confirming leverage of revenue growth against fixed cost base expansions.

Monitoring these will help gauge whether recent operational progress translates into durable profitability gains or highlights ongoing constraints.[S2],[N1]

Latest financial snapshot

| Metric | Value | Period |

|---|---|---|

| Cash & equivalents | $75mm | |

| 2026-03-31 | ||

| Total debt | 0 USD | |

| 2026-03-31 | ||

| Net debt | $-75mm | |

| 2026-03-31 | ||

| Current assets | $153mm | |

| 2026-03-31 | ||

| Current liabilities | $36mm | |

| 2026-03-31 | ||

| Current ratio | 4.24x | |

| 2026-03-31 |

Source: SEC companyfacts cache [F1].

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments