Reading International's Dual-Segment Strategy Challenges and Opportunities in 2025

The company’s combined cinema and real estate operations show signs of operational stabilization amid liquidity pressures and strategic asset consolidation.

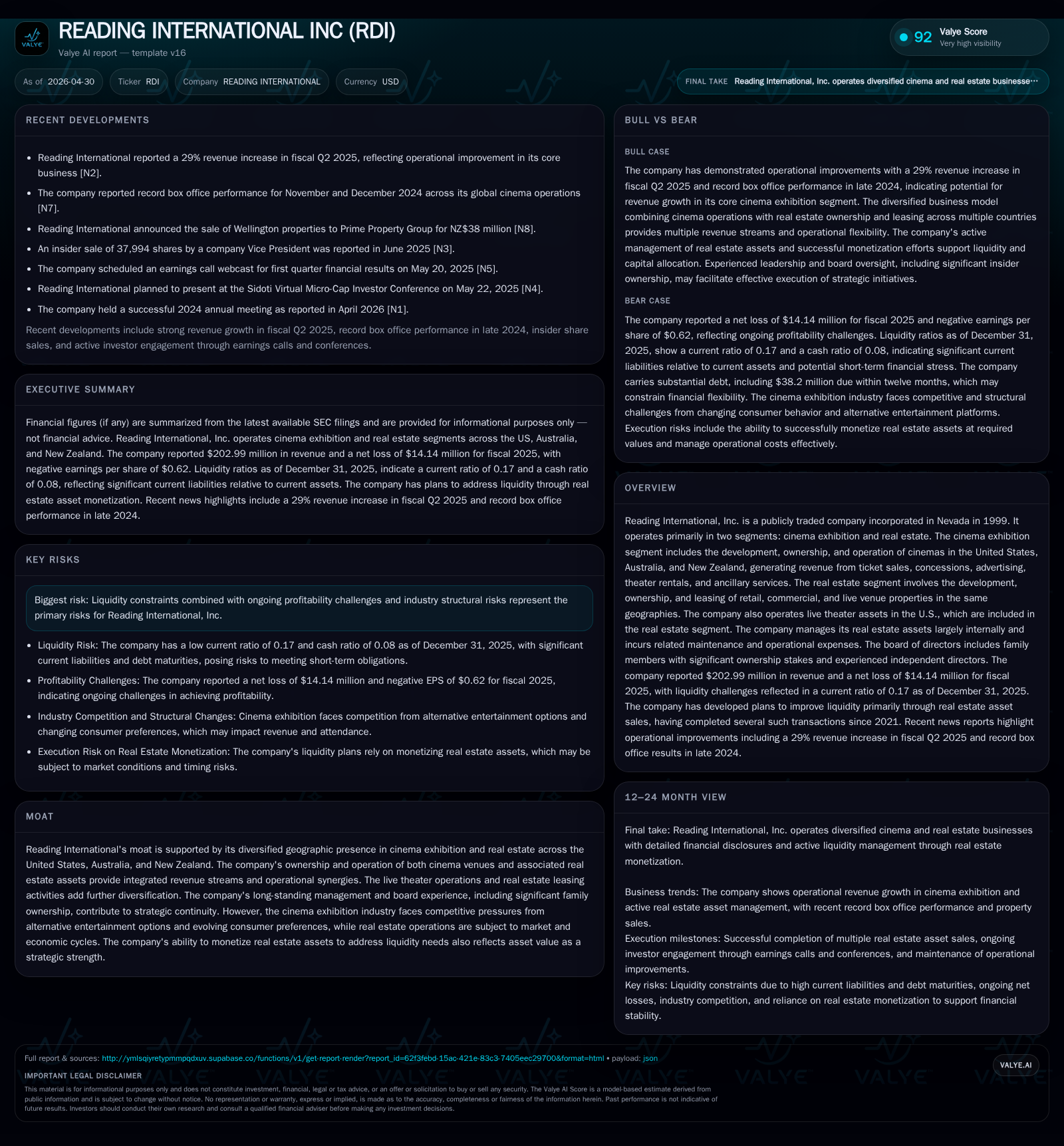

Reading International reported improved revenue and operating income through the first nine months of 2025, leading to no impairment charges for key asset groups as per its latest 10-Q. The company secured full ownership of the critical Cinema 1,2&3 property by ending a master lease arrangement, strengthening its real estate control and refinancing short-term debt to shore up liquidity. Its diversified footprint across cinema exhibition and real estate in the US, Australia, and New Zealand enables integrated revenue generation but also exposes it to sector-specific risks such as shifting entertainment consumption and cyclical property markets. Key challenges remain around heavy leverage and working capital deficits that heighten refinancing needs despite ongoing improvement in operating metrics.

Recent Operational Developments Reinforcing Stability

Reading International's latest quarterly filing (Q3 2025) reveals meaningful operational progress relative to prior periods. The company generated higher revenues and operating income through the first nine months ended September 30, 2025 when compared to the same period in 2024. This improved performance justified the absence of impairment charges against its asset groups under ASC guidance— an important signal given the historically weak profitability backdrop. Management expressed confidence that these favorable trends will extend into the final quarter of 2025 [S2].

A transformative corporate development highlighted in the subsequent 8-K filing is Reading's completion of acquiring full legal ownership of its critical Village East cinema property (Cinema 1,2&3) in New York City by winding up the longstanding master lease agreement with Sutton Hill Associates. This ends Reading's prior status as a beneficial tenant and transitions it into a direct owner/operator for this prime asset [S3], [S1]. Coupled with refinancing certain short-term debts via long-term instruments as part of this transaction, these moves materially enhance the company's strategic footing over this flagship asset.

This consolidation reduces counterpart risk inherent in third-party leases and provides more holistic control over one of its marquee properties that anchors its exhibition segment revenues.

Integrated Business Model: Cinema Exhibition Combined with Real Estate Assets

Reading operates primarily through two synergistic divisions: cinema exhibition and real estate management. The exhibition segment spans the developmental footprint, ownership, and operation of cinemas distributed across highly key markets in the United States, Australia, and New Zealand. Revenue within this division is multifaceted: patrons pay for ticket admissions while additional cash flow arises from concessions sales (food & beverage), advertising placements within theaters, theater rentals for events or screenings outside regular programming hours, plus various ancillary services linked to customer experience enhancement [S1].

In parallel, Reading owns diverse real estate assets comprising retail outlets, commercial properties including office space, as well as venues suited for live performances—all strategically situated within close proximity to or integrally linked to their cinema locations across geographies. These assets are internally managed which allows Reading to control operational upkeep costs while generating lease income from third parties or event tenants for its live theater spaces primarily located within the U.S. This dual-segment integration creates cross-leverage opportunities where real estate can underpin physical attendance drivers at cinemas/livetheaters and vice versa; conversely ownership enables Reading to optimize location economics better than common operators who lease venues externally.

Crucially for industry practitioners evaluating Reading's model: the company's ability to charge intersegment fees or allocate internal cost responsibilities aligns incentives between segments while realizing incremental margin improvements through operational synergies.

Industry Dynamics and Competitive Positioning

The cinema exhibition sector globally faces a pivotal inflection stemming from rising consumer preference shifts toward digital streaming platforms which compete directly against theatrical attendance demand. Cinema operators must increasingly focus on enhancing experiential appeal through modernized infrastructure upgrades (e.g., premium seating tech like recliners), content exclusives that incentivize visits (limited theatrical windows), and aggressive marketing of concession offerings where margins remain attractive yet increasingly contested.

Reading’s geographic spread across three countries offers a buffer against localized regulatory shifts or economic downturns but also demands adaptability to region-specific operational norms ranging from film licensing rules to property tax regimes.

Its integrated business model—combining ownership/control over both cinemas and adjacent/related real estate—differentiates it slightly from pure-play cinema chains or passive landlords by compressing revenue cycles vertically. Nonetheless competitive pressure exists from larger consolidated chains globally who possess greater scale advantages or from independent multiplexes competitively pricing admission or concession products.

These drivers collectively depend upon execution quality especially balancing capital outlays versus returns given tight liquidity profiles noted elsewhere [S1], [S2].

Risks, Liquidity Challenges, and Operational Constraints

Despite positive operational indicators recent filings paint a challenging picture related primarily to financial leverage:

- Total debt stands roughly at $185 million against cash reserves near $10.5 million leaving net indebtedness above $174 million illustrating significant reliance on refinancing capability amidst ongoing losses reported in net income figures (-$12.06 million for nine months ended September 30, 2025) [F1], [S2].

- Current liabilities notably exceed current assets producing a low current ratio (~0.17) which signals working capital strain tied possibly to timing mismatches or seasonal payables incurred within real estate operations [F1].

- The cinematic exhibition business remains vulnerable structurally from prolonged shifts in consumer behavior favoring at-home media consumption reducing foot traffic sustainably.

- Real estate activities carry cyclical risk exposure where downturns in commercial leasing markets or live venue event curtailments could exacerbate profit volatility.

- The company continues to navigate uncertainties around implementing liquidity improvement plans including potential asset sales or refinancing terms subject to market conditions at each milestone date. These constraints advise caution when evaluating future cash flow sustainability absent clear de-leveraging outcomes.

Upcoming Milestones and Market Signals to Monitor

Investors tracking Reading should prioritize monitoring:

- Debt refinancing progress particularly upcoming maturities within next twelve months requiring successful extension or conversion into longer durations without onerous terms as flagged in recent filings [S2], [S3].

- Quarterly earnings releases beyond end-2025 unfold whether revenue momentum sustains or deteriorates amid stiff macroeconomic headwinds.

- Decisions emanating from annual meetings including any proposed changes in capital structure or executive incentives which may impact strategic direction [N1].

- Asset monetization developments providing incremental liquidity evidence supporting going concern evaluations outlined repeatedly by management. Clear communication around these factors will materially influence perceived risk/reward balance regarding Reading’s ongoing dual-segment engagements.

Condensed Financial Profile and Balance Sheet Health

Latest financial snapshot

| Metric | Value | Period |

|---|---|---|

| Cash & equivalents | $10.53mm | |

| 2025-12-31 | ||

| Total debt | $185.09mm | |

| 2025-12-31 | ||

| Net debt | $174.56mm | |

| 2025-12-31 | ||

| Current assets | $21.82mm | |

| 2025-12-31 | ||

| Current liabilities | $128.58mm | |

| 2025-12-31 | ||

| Current ratio | 0.17x | |

| 2025-12-31 |

Source: SEC companyfacts cache [F1].

| Metric | Amount (USD millions) |

|---|---|

| Cash & Equivalents | $10.53 |

| Total Debt | $185.09 |

| Net Debt | $174.56 |

| Current Assets | $21.82 |

| Current Liabilities | $128.58 |

| Current Ratio | 0.17 |

Latest financial disclosures confirm these leverage ratios underpin substantial liquidity risk notwithstanding improved operating performance during 2025’s first nine months [F1], [S2]. Operating income still resides modestly negative netting -$5.31 million annually masking positive segment metrics that have yet fully offset corporate expenses including interest burdens mounting near $13 million on trailing twelve month basis per quarterly data reconstructions.

Conclusion

Reading International presents a case study of a company leveraging asset integration between cinema exhibition operations and associated real estate holdings across multiple international regions amid a challenging economic environment for both sectors. Its recent strategic milestones—including removing lease constraints on key properties combined with proactive refinancing efforts—have bolstered its strategic autonomy while underscoring persistent financial vulnerabilities centered on leverage levels that require decisive remediation for sustainable growth trajectory realization.

This analysis does not constitute investment advice but is intended strictly as an independent examination informed by public SEC filings and recent company disclosures.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments