Zhengye Biotechnology’s Strategic Corporate Changes: Implications for Growth and Governance

The company's March 2026 Annual General Meeting resolutions introduce corporate governance updates amid ongoing operational and financial challenges.

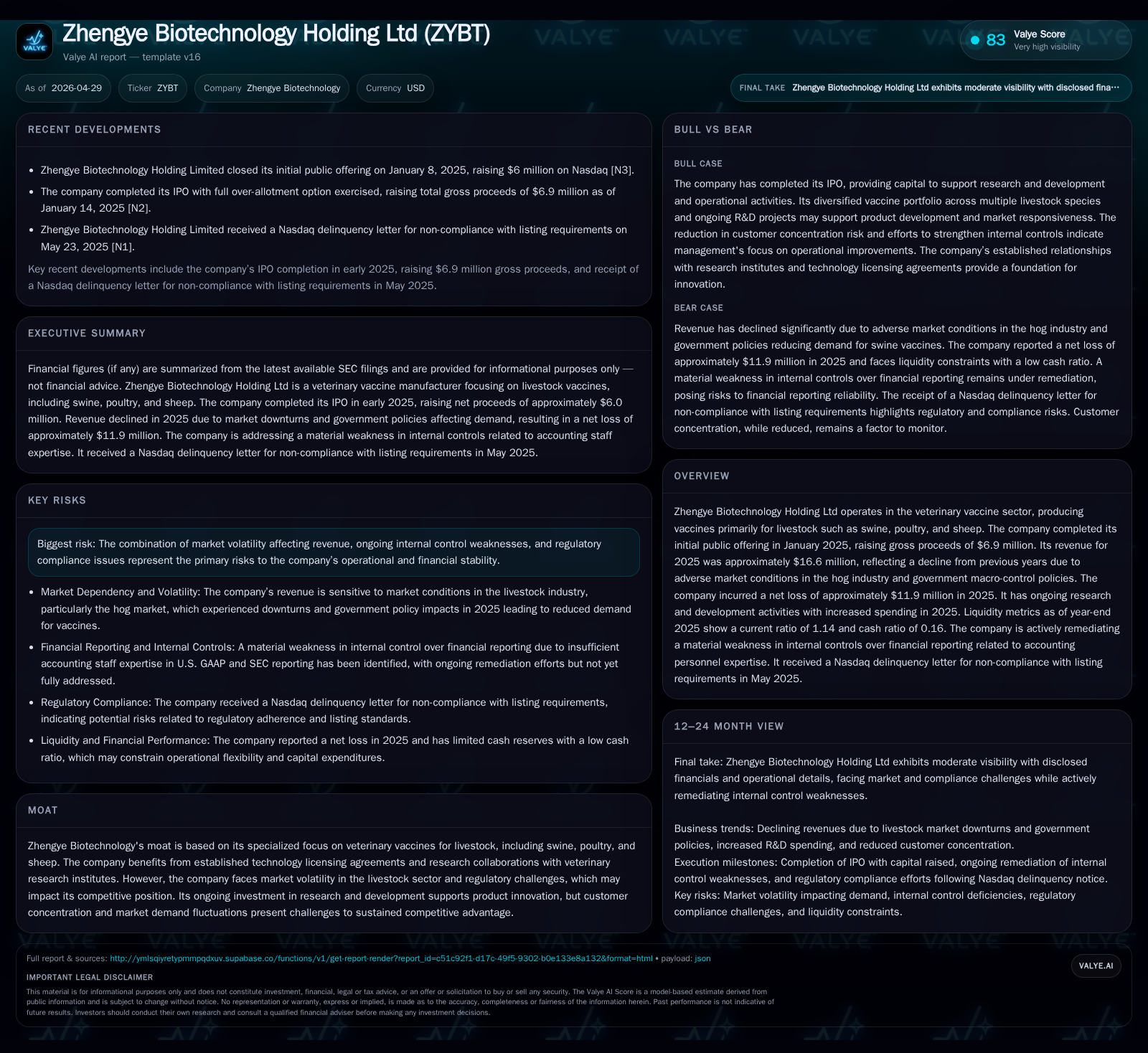

In its latest quarterly disclosure, Zhengye Biotechnology Holding Ltd approved critical governance changes, including share reclassification and adoption of new corporate articles, signaling a strategic alignment to enhance compliance and shareholder confidence. The veterinary vaccine producer faces a challenging 2025 marked by revenue declines driven by livestock market volatility and regulatory constraints, compounded by internal controls weaknesses. Zhengye’s business relies heavily on livestock vaccine sales backed by research collaborations, but customer concentration and demand fluctuations present growth challenges. Ongoing R&D investment and steps to remediate governance issues set the stage for potential recovery in operational stability.

Recent Operating Developments: Corporate Governance Refresh

Zhengye Biotechnology Holding Ltd advanced important corporate governance initiatives at its March 24, 2026 Annual General Meeting (AGM). Shareholders approved the election of two new directors alongside the re-election of incumbent board members — standard moves that maintain board functionality. More notably, the AGM ratified an ordinary resolution for share reclassification and consolidation designed likely to optimize capital structure or enhance shareholder equity representation. The assembly also passed a special resolution adopting new memorandum and articles of association aimed at streamlining corporate governance frameworks[S2][S3].

These actions reflect a deliberate effort to address investor expectations and regulatory pressures linked to Nasdaq listing compliance amid Zhengye's receipt of delinquency notices. Adoption of updated corporate bylaws enhances procedural clarity and may ease future governance-related filings or capital raises. This reshaping of legal structures arrives against a backdrop of challenging financial results and operational volatility underscoring the need for transparent management oversight.

Business Model: Veterinary Vaccines Revenue Streams and Contractual Nuances

Zhengye operates squarely within the veterinary vaccine market with its product portfolio spanning vaccines tailored for swine, poultry, sheep, cattle, goats, and dogs distributed across China’s extensive agricultural regions plus select international destinations such as Vietnam, Pakistan, and Egypt[S1]. Its core revenue mechanism hinges on supplying vaccines under contracts identified with single performance obligations — delivering finished goods without bundled services or additional promises. Revenue recognition occurs at point of transfer when control passes to customers typically evidenced by acceptance[S1].

Functioning as principal in these transactions means Zhengye assumes inventory risks including costs of unsold stock while controlling pricing strategies. The company offers sales rebates to distributors structured as product credits contingent upon purchase volumes; these discounts represent variable consideration incorporated into revenue estimates updated each reporting period[S1]. Notably absent are product return rights or further customer incentives beyond rebates which simplifies net revenue calculations.

Customer concentration is significant though somewhat diversified relative to prior years. Swine vaccine sales remain dominant — comprising over three-quarters of total revenues — aligned with China's large pork production industry[S1]. Distribution channels split between direct sales to large farms and broader distributor networks providing market penetration depth. This business model emphasizes volume-based growth subject to livestock health demands and policy-driven immunization mandates.

Industry Positioning: Competitive Landscape and Regulatory Environment

Zhengye nestles competitively within China’s veterinary vaccine industry which benefits from supportive government policies aimed at epidemic detection and compulsory animal vaccination programs[S1]. While industry expansion is buoyed by rising farm scale modernization and government macro-control initiatives targeting disease containment, such policies also inject regulatory complexity impacting market stability.

The company's moat derives largely from exclusive technology licensing agreements with veterinary research institutes coupled with cooperative research partnerships that bolster vaccine innovation pipelines[S1]. These collaborations offer a barrier against commoditization in a sector otherwise subject to pricing pressures from generic alternatives.

However, challenges remain pronounced given nascent Nasdaq compliance irregularities spotlighted in recent SEC communications requiring bolstered internal controls over financial reporting[S5]. Competitive rivalry includes domestic peers similarly pursuing expanded portfolios into household pet vaccines — an arena Zhengye targets for diversification yet still embryonic compared to livestock offerings.

Growth Drivers: Technological Innovation and Market Expansion Opportunities

Zhengye's post-IPO capital infusion—approximately $6.9 million gross raised in January 2025—has underpinned increased research & development expenditure focused on refreshing its vaccine offerings portfolio[S1]. With RMB20.2 million ($2.9 million) dedicated thus far to R&D projects since the IPO registration effectiveness date, the company clearly prioritizes technological advancement as a lever for sustained market relevance.

Expanding product breadth beyond traditional livestock vaccines toward household pet disease prevention represents an incremental growth vector supported by specialized R&D projects[S2]. Furthermore, scaling its sales distribution network enhances reach across China’s heterogeneous farm operations while enabling exposure to emerging export markets with recent trade links established.

Investments in upgrading manufacturing technologies seek operational efficiencies alongside quality improvements essential in meeting stringent regulatory standards imposed domestically while preserving pricing power amidst volatile raw material inputs[S2]. Frequent engagement with provincial agricultural administrations helps cement Zhengye’s presence in immunization campaigns.

Risks and Constraints: Market Volatility, Compliance, and Operational Challenges

Revenue volatility rooted in agriculture commodity price swings—primarily hog prices—has materially impacted Zhengye’s top line which contracted from RMB186 million in 2024 to RMB116 million ($16.6 million) in 2025 reflecting weakened farmer demand under restrictive domestic hog inventories due to government macro-control policies[F1].

Further constraints stem from customer concentration risks; although major clients have diminished as a share of receivables recently—with top two customers representing approximately 23% combined—the reliance on few large-scale farms leaves revenue exposed if any key account reduces order volumes or disputes pricing terms[S20]. Regulatory uncertainty remains given evolving animal health policies that may alter mandatory immunization schedules adversely affecting volume demand.

Forward Focus: What to Monitor Next in Strategy Execution and Demand Signals

Key milestones will pivot on observable progress in internal control remediation activities through new accounting hires completion metrics alongside successful external audits confirming improved disclosure compliance[S2][S5][S23].

Operationally important will be quarterly tracking of revenue stabilization or early signs of increase especially within swine vaccine segments post-2025 losses complemented by growth evidence stemming from newer poultry or other livestock vaccines. Attention should also be directed at efficacy and commercialization timing of R&D outputs targeting household pet vaccinations potentially diversifying income streams.

Monitoring transparency enhancements via corporate governance modifications adopted at AGM—including share consolidation effects on shareholder structure—and consistent application of newly ratified memorandum provisions will be crucial indicators of management discipline.[S2][S3]

Financial Snapshot: Liquidity, Profitability, and Balance Sheet Health

Latest financial snapshot

| Metric | Value | Period |

|---|---|---|

| Total debt | $1,366,000 | |

| 2025-12-31 | ||

| Net debt | -$1,183,000 | |

| 2025-12-31 | ||

| Current assets | $19,650,000 | |

| 2025-12-31 | ||

| Current liabilities | $17,230,000 | |

| 2025-12-31 | ||

| Current ratio | 1.14x | |

| 2025-12-31 |

Source: SEC companyfacts cache [F1].

| Metric | Value | Period End |

|---|---|---|

| Revenue | $16.6 million | |

| 2025-12-31 | ||

| Net Loss | -$11.9 million | |

| 2025-12-31 | ||

| Cash & Equivalents | $2.55 million | |

| 2024-12-31 | ||

| Total Debt | $1.37 million | |

| 2025-12-31 | ||

| Current Ratio | 1.14 | |

| 2025-12-31 |

The company reported substantial losses nearing $12 million on revenue shrinking below $17 million during fiscal year 2025 [F1]. Total debt stood at approximately $1.37 million at year-end 2025, partially offset by cash reserves of $2.55 million as of December 2024[F1].

High research spending contributes heavily to operating deficits yet represents strategic investment supporting medium-term competitiveness.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments