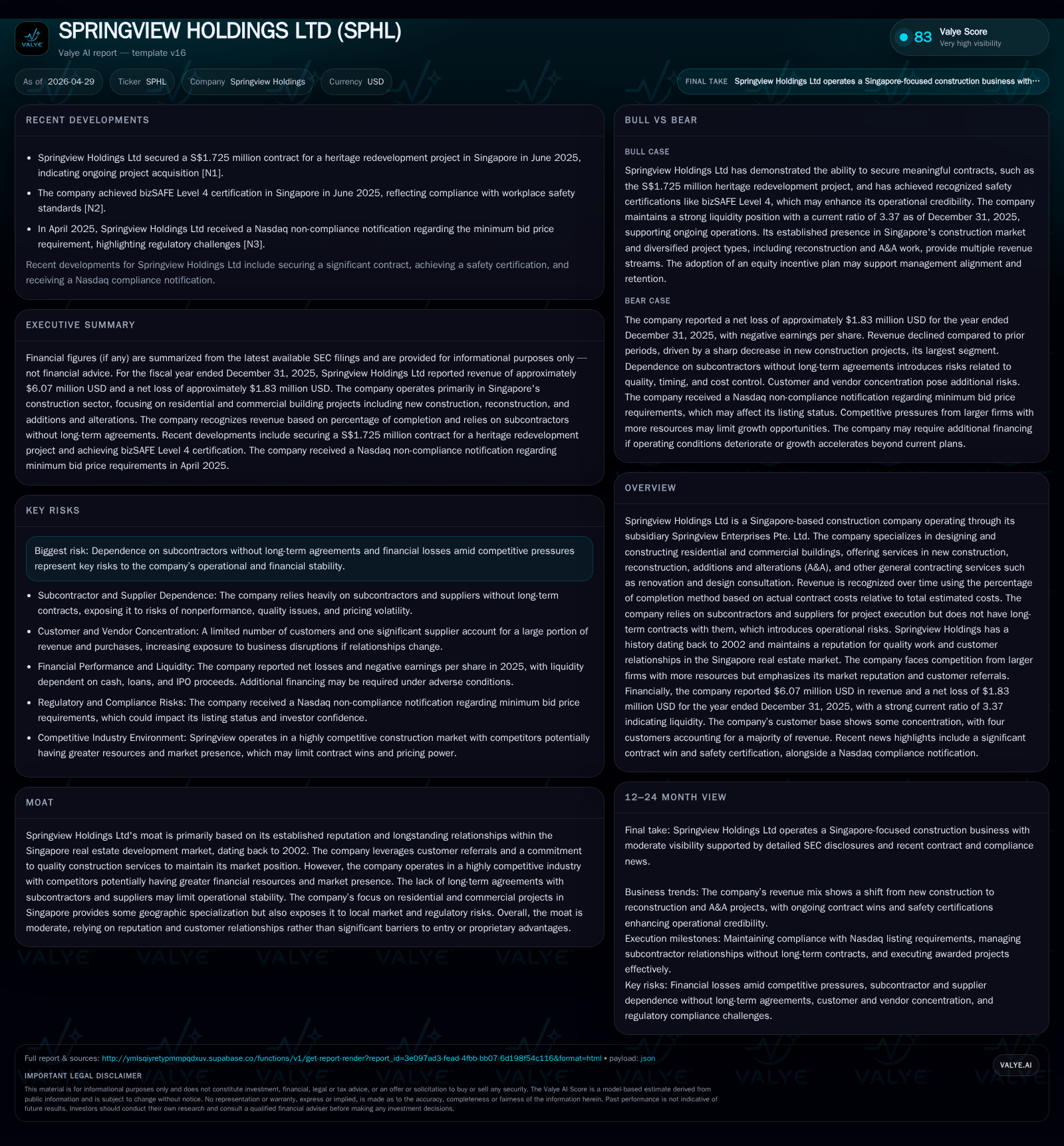

Springview Holdings Introduces Equity Incentive Plan Amid Market Shift

Springview Holdings enacts governance and incentive changes to bolster competitiveness in a challenging Singapore construction market.

In March 2026, Springview Holdings Ltd adopted a new equity incentive plan authorizing issuance of up to 400,000 shares and appointed a new independent director with audit committee leadership. These governance upgrades arrive as the company navigates a competitive Singapore construction landscape marked by fluctuating revenues and margin pressures. Springview’s business model centers on design-build and general contracting services in residential and commercial segments, relying heavily on subcontractors without long-term agreements. The company’s growth hinges on shifting project mix toward higher-margin reconstruction and addition & alteration works while managing operational risks from subcontractor dependencies and market cyclicality.

Recent Quarterly Developments Reshape Governance and Incentives

Springview Holdings Ltd took pivotal steps in governance and compensation structure during Q1 2026 that reflect a strategic recalibration during market challenges. On March 27, 2026, the company officially adopted its 2026 Equity Incentive Plan authorizing issuance of up to 400,000 class A ordinary shares as equity awards [S2]. This move signals management’s intent to closely align employee incentives with shareholder value creation amidst a competitive environment.

Complementing this initiative was the leadership transition effective March 13, where Mr. Hung Yu Wu resigned as independent director and audit committee chair without any operational disagreements cited. Stepping into these key oversight roles was Mr. Chin Leng Tan – an experienced executive with extensive background in business development across Asia – appointed as independent director and chairperson of the audit committee [S3]. This strengthens the company’s corporate governance framework at a critical juncture when transparent financial oversight gains heightened importance.

Together, these developments address both internal alignment and external scrutiny needs as Springview contends with evolving market dynamics.

Business Model: Integrated Design-Build and Contracting Services

Springview operates principally through its wholly-owned subsidiary Springview Enterprises Pte. Ltd., focused on Singapore-based construction projects spanning residential and commercial categories [S1]. The company provides comprehensive services encompassing four main streams:

- New construction (demolition plus rebuilding existing structures)

- Reconstruction (substantial replacement portions within houses)

- Additions & Alterations (minor structural modifications within existing buildings)

- Other general contracting services including renovations and design consultation

The firm executes projects either in design-build mode where it leads both conceptual design and construction or purely as contractor under established architectural plans. Collaboration with architectural firms supports tailored solution delivery in the design-build role while longstanding subcontractor relationships facilitate quality-driven execution [S1].

Springview recognizes revenue using the percentage of completion method based mainly on actual contract costs relative to estimated total costs—a critical accounting policy that makes accurate cost forecasting essential for revenue timing and margin realization [S1][S5]. Importantly, the reliance on subcontractors—and absence of long-term agreements—adds an operational risk layer whereby fluctuations in subcontractor availability or cost can impact execution.

Competitive Position within Singapore’s Construction Industry

The company's competitive edge rests largely on its established reputation since inception in 2002 coupled with deep customer relationships that foster referrals—factors constituting its moderate moat [S1]. This local specialization allows Springview to maintain credibility amid numerous competitors.

However, the sector itself is marked by fierce competition involving larger players wielding greater financial resources, scale efficiencies, broader service offerings, and potentially aggressive pricing strategies that challenge smaller firms like Springview. Such competitive intensity compresses margins and necessitates consistent high-quality delivery to sustain client trust.

Regulatory factors governing building codes and urban planning impose additional compliance complexity but do not currently present insurmountable barriers given Springview’s experience within Singapore’s market context.

Operational and Financial Growth Drivers

Since tightening margins afflicted the company notably in 2024 due to aggressive market pricing and incremental renovation costs requested by some customers, recent performance trends point toward improvement driven by prudent project selection shifts [S1].

The movement from lower-margin new residential construction toward higher-margin reconstruction projects along with additions & alterations has aided gross profit margin expansion—from approximately 10.3% in 2024 to around 13.7% in 2025 on a Singapore dollar basis—with tighter control over subcontractor expenses playing an essential role [S1].

Additionally, entry into more commercial projects contributes positively given typically better margin profiles compared to purely residential undertakings.

Operational efficiencies through improved project management procedures further underpin this progress by reducing overheads onsite.

These drivers collectively point toward gradual margin recovery potential alongside steady revenue growth contingent on successful contract wins.

Key Risks and Potential Headwinds Ahead

Significant risks center around operational dependencies on third-party subcontractors who lack binding long-term contracts with Springview. This dynamic risks supply chain disruptions or last-minute cost escalations impacting project profitability.

Market cyclicality inherent in Singapore’s real estate development sphere—affected by macroeconomic cycles or regulatory shifts—creates unpredictability in securing new projects consistently at favorable terms.

Intensified sector competition increases price pressures and may constrain contract awards or compel concessionary pricing that erodes margins further if not managed prudently.

There is also exposure to cost overruns stemming from inaccurate initial cost estimates or unforeseen project delays which influence percentage-of-completion revenue recognition adversely.

Financial losses experienced recently highlight the need for continual pipeline replenishment via aggressive tender participation balanced against cautious risk management.

What Investors Should Monitor Next

Upcoming critical milestones include announcements regarding new project awards which will provide forward-looking visibility on revenue streams.

Monitoring execution timelines for ongoing contracts is valuable to anticipate the pace of revenue recognition given percentage completion accounting methodology.

Results linked to incentivization from the newly implemented equity incentive plan will reveal management engagement efficacy over subsequent reporting periods.

Further changes or additions to board composition or governance structures will be also noteworthy as they could influence strategic direction or oversight rigor.

Moreover, diversification efforts between residential renovations/additions versus commercial projects constitute an important metric affecting margin quality.

Customer satisfaction indicators reflecting successful problem resolution through effective communication channels remain key qualitative signposts affecting referral generation capacity.

Financial Snapshot: Performance and Liquidity Overview

Latest financial snapshot

| Metric | Value | Period |

|---|---|---|

| Total debt | $497,531 | |

| 2025-12-31 | ||

| Net debt | $497,531 | |

| 2025-12-31 | ||

| Current assets | $7,714,034 | |

| 2025-12-31 | ||

| Current liabilities | $2,285,748 | |

| 2025-12-31 | ||

| Current ratio | 3.37x | |

| 2025-12-31 |

Source: SEC companyfacts cache [F1].

| Metric | Amount (USD) |

|---|---|

| Revenue | 6,072,681 |

| Operating Income | -1,929,881 |

| Net Income | -1,829,848 |

| Total Debt | 497,531 |

| Current Ratio | 3.37 |

As of fiscal year-end December 31, 2025, Springview reported $6.07 million in revenues but incurred an operating loss near $1.93 million alongside a net loss approximating $1.83 million USD indicating profitability challenges persisting despite margin improvements [F1].

The company’s total debt at about $498K USD remains modest relative to current assets around $7.71 million USD resulting in a robust current ratio of approximately 3.37 that suggests sufficient short-term liquidity capacity [F1].

Operating cash flows registered negative outflows reflecting working capital demands particularly from increased payments settling accounts payable balances during the year [S22]. Meanwhile net cash provided by investing activity chiefly resulted from loan repayments received from third parties supporting cash inflows [S22]. Financing activities contributed positive net inflows with proceeds primarily connected to IPO-related capital injections underscoring dependency on external funding sources for ongoing operations [S10].

This analysis reflects information publicly disclosed by Springview Holdings Ltd through SEC filings as of mid-2026; it emphasizes operating dynamics without offering investment advice or price forecasts.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments