Lichen International Expands Share Capital and Navigates Revenue Decline with AI Investment

After a significant revenue drop in 2025, Lichen International ramps up share capital and focuses on AI-driven service transformation.

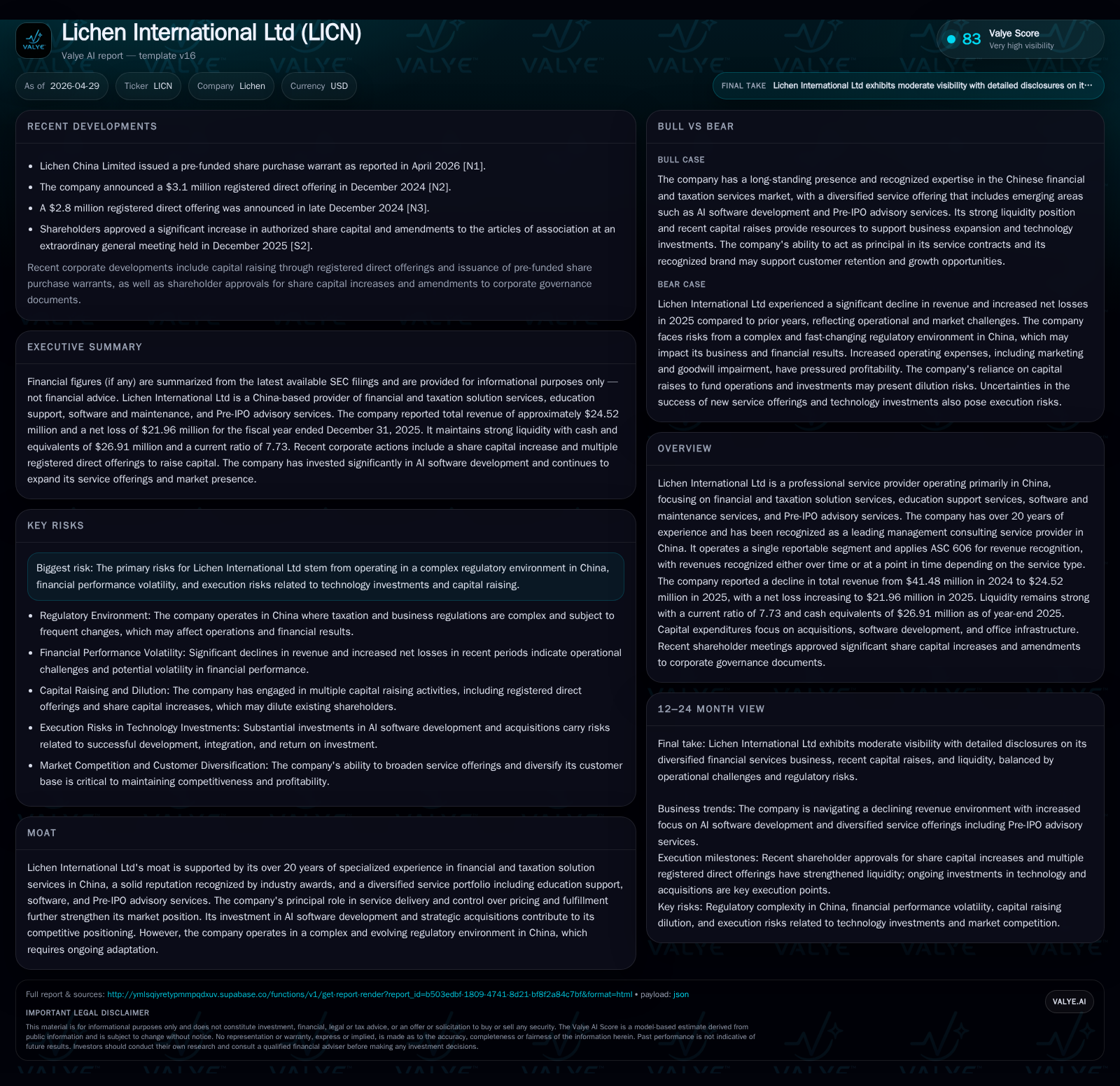

Lichen International Ltd reported a sharp revenue decline to $24.5 million in 2025 from $41.5 million in 2024, resulting in a net loss exceeding $21 million. The company held an extraordinary general meeting approving a substantial increase in authorized share capital to support expansion and strategic initiatives. Its core business, financial and taxation consulting services in China, faces intensifying competition and evolving regulations, partly addressed by its growing investment in AI software development. While liquidity remains robust with over $26 million cash on hand, operational challenges persist, notably declining revenues and goodwill impairments. Strategic growth will hinge on successful integration of AI, broadened service offerings, and acquisitions in a complex regulatory landscape.

Recent Operating Update

Lichen International Ltd convened an extraordinary shareholder meeting on December 30, 2025, approving a dramatic increase in its authorized share capital from $1 million to $200 million by issuing tens of billions of new shares [S2]. This strategic move underscores the company's need for substantial financing to support its transformational initiatives amid deteriorating financial results. The meeting outcomes indicate shareholder backing for aggressive capital raising to fuel growth ventures including acquisitions and technology investments.

The latest annual report showed that Lichen’s total revenues dwindled by roughly 41% year-over-year to $24.5 million as of December 31, 2025, down from $41.5 million in 2024 [F1][S1]. This decline pressured the bottom line into a net loss of nearly $22 million after prior profitable years. Operating income turned sharply negative at about -$18 million reflecting both revenue erosion and considerably elevated operating expenses linked partly to goodwill impairments and investments in AI projects [F1][S14].

Business Model

Lichen International's core business revolves around professional services in the Chinese market: providing financial and taxation solution services, education support services, software maintenance services, and pre-IPO advisory under the "Lichen" brand [S1]. The company derives revenues primarily through contract engagements with corporate clients who pay fees based on service complexity—ranging from ongoing consulting to discrete project-based arrangements.

Revenue recognition follows ASC Topic 606 with some contracts recognized over time (e.g., education or ongoing consulting) while others are point-in-time (e.g., specific advisory reports or software licenses) [S1]. This mixed revenue model allows flexibility but also exposes the firm to variability stemming from shifts in client demand or contract renewals.

Margins have compressed due to higher selling expenses (notably marketing) nearly doubling between 2023-2024 and elevated general administrative costs aligned with organizational scaling and tech R&D efforts [S1]. The firm's expanded offerings include proprietary AI-enabled solutions intended to augment human expertise in complex tax planning and risk management—targeting premium advisory fees.

Industry Structure & Competitive Position

Operating mainly within China’s financial consultancy ecosystem—which is highly fragmented yet intensely competitive—Lichen benefits from over two decades of established market presence recognized through consistent national awards as a Top Management Consulting provider between 2012-2025 [S1]. Despite this stature, the company faces pressure from both domestic boutique firms specialized in niche consulting verticals and large multinational professional services firms expanding their footprint into China.

The evolving regulatory framework around taxation in China adds complexity requiring agile compliance capabilities that Lichen leverages via localized expertise combined with technology tools.

While Lichen has pricing power rooted in its reputation and breadth of offerings spanning advisory through technology provision, margin sustainability depends on balancing bespoke consulting with scalable software-based solutions.

Growth Drivers

Artificial Intelligence Integration

The surge of AI technologies constitutes a double-edged sword: reshaping market expectations for efficiency while escalating competition intensity. Lichen plans to harness AI-driven tools for enhancing accuracy in tax computations, automating routine tasks enabling consultants to focus on high-value strategic advising such as complex tax structures or risk mitigation strategies where human judgment is critical [S1]. Successful execution here could broaden service portfolios and command premium pricing.

Strategic Acquisitions

The company identified acquisition activity as fundamental for scale expansion and customer diversification. By targeting firms across different sizes or specialty niches within China's market—backed by improved capital structure post-share increase—Lichen aims to consolidate resources enhancing competitive positioning with wider geographic reach through new representative offices [S18].

Service Diversification & Customer Base Expansion

Broadening offerings beyond traditional financial/taxation solutions into education support services, dedicated software maintenance contracts, and pre-IPO advisory services anchors revenue streams more firmly across client segments reducing concentration risk [S1]. Diversification coupled with enhanced delivery efficiency can improve client retention rates.

Risks & Growth Constraints

Regulatory Complexity & Market Volatility

China’s rapidly shifting tax laws impose ongoing compliance burdens; any misinterpretation risks penalties or loss of client confidence. Furthermore, macroeconomic fluctuations affecting Chinese enterprise activities influence demand cyclically with uneven visibility.

Execution Risks on Technology Projects

AI software development represents significant investments carrying risk inherent to tech project overruns or failure to meet client adoption levels impacting anticipated returns.

Financial Performance Volatility & Internal Controls

Net losses have deepened driven partly by goodwill impairment charges reflecting asset write-downs due to past acquisitions underperforming expectations. Management disclosed material weaknesses in financial reporting controls signaling potential risks around timely accurate disclosure adherence [S21].

Capital Raising Dependence

Execution of growth strategies depends heavily on access to equity capital enabled by the recent share authorization surge—the dilution impact alongside deployment efficacy bears scrutiny.

What To Watch Next

- Completion status of the AI software under development anticipated through 2026 which could mark inflection toward technologically augmented advisory services.

- Utilization progress of increased share capital—timing/scale of equity issuances and spending deployment on acquisitions or R&D.

- Quarterly revenue stabilization or recovery indicators post-2025 steep declines focusing on client contract renewals,

- Improvements addressing internal control weaknesses announced potentially affecting investor confidence or compliance adherence,

- Adjustments responding to evolving Chinese taxation policy impacting service requirements.

Financial Profile Summary (Latest Full Year)

Latest financial snapshot

| Metric | Value | Period |

|---|---|---|

| Cash & equivalents | $27mm | |

| 2025-12-31 | ||

| Current assets | $36mm | |

| 2025-12-31 | ||

| Current liabilities | $5mm | |

| 2025-12-31 | ||

| Current ratio | 7.73x | |

| 2025-12-31 |

Source: SEC companyfacts cache [F1].

| Metric | Value | Period |

|---|---|---|

| Revenue | $24.52 million | |

| FY 2025 | ||

| Operating Income | $(18.07) million | |

| FY 2025 | ||

| Net Income | $(21.96) million | |

| FY 2025 | ||

| Cash & Equivalents | $26.91 million | |

| FY 2025 | ||

| Current Ratio | 7.73 | |

| FY 2025 | ||

| Total Debt | $1.59 million* | |

| End FY 2023* | ||

| *Debt figure is best effort from latest available data not fully current [F1] |

Liquidity remains robust driven by conservative debt usage maintaining a net cash position enabling tactical flexibility despite operating losses sustained through restructuring and technology pivot stages.

This analysis strictly uses publicly available SEC filings through April 28, 2026 ([S1],[S2],[F1]) along with contextual industry knowledge without providing investment recommendations or price forecasts. All numeric references adhere exclusively to verified sources cited herein.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments