Criteo S.A. Advances Retail Media Growth and Legal Domicile Shift in 2025

Criteo reported stable revenue with Retail Media expansion, amended bylaws, and plans to relocate its legal domicile to Luxembourg.

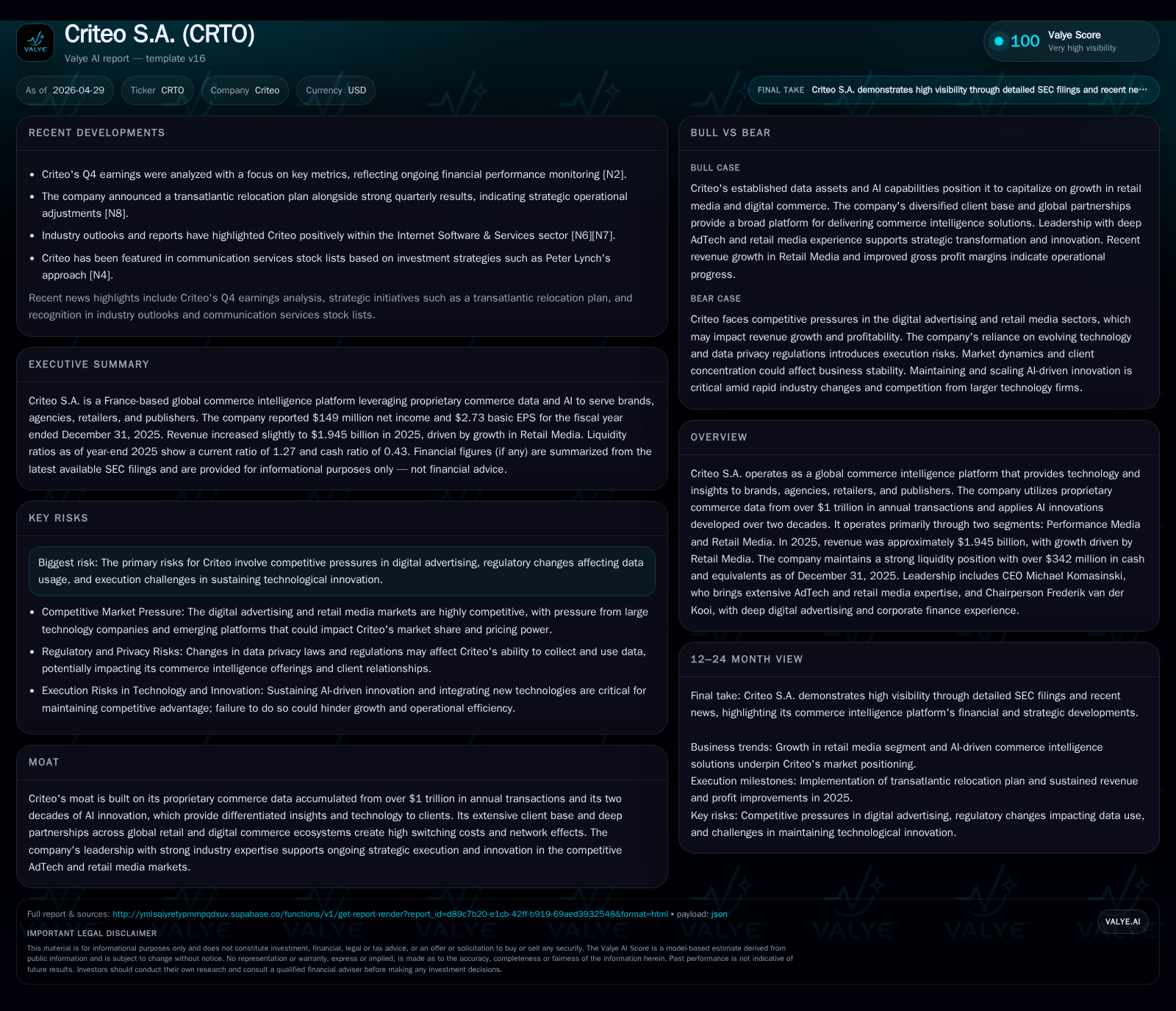

In its latest 8-K and amended 10-K/A filings dated April 28, 2026, Criteo S.A. confirmed a stable revenue environment for fiscal year 2025 with $1.945 billion in revenues driven by Retail Media growth despite flat performance in Performance Media. The company’s operational results showed improved gross profit and profitability metrics while retaining a strong liquidity position. Additionally, Criteo’s board amended its bylaws reflecting a slight decrease in shares outstanding and initiated shareholder approval for a cross-border conversion moving legal domicile from France to Luxembourg with direct Nasdaq listing of ordinary shares replacing American Depositary Shares (ADS). The company's business model remains centered on leveraging proprietary commerce data and AI technology across Performance and Retail Media segments. Growth is anchored in expanding retail media partnerships, with risks including digital ad market competition and regulatory pressures on data usage.

Recent Operating Update

Criteo S.A. released significant updates on April 28, 2026 via an 8-K form and an amended annual report (10-K/A) covering the fiscal year ended December 31, 2025 [S3][S16]. The company reported that total revenues modestly increased by 1%, reaching $1.945 billion, or were approximately flat on a constant currency basis compared to the prior year [S16][S24]. This top-line dynamic was led by strength in the Retail Media segment, partially offsetting flat contribution from Performance Media.

Profitability improved notably with gross profit rising 7% year-over-year to $1.049 billion and "Contribution ex-TAC" — a non-GAAP profitability measure excluding traffic acquisition costs — increasing by 5% [S16][S24]. Net income surged by nearly 30%, reaching $149 million [S24]. Free cash flow remained solid at $211 million supported by operating cash flow of $311 million and disciplined capex [S24]. Liquidity remains strong with cash and equivalents of approximately $342 million at year-end [F1].

Importantly, the board authorized an amendment of the company's bylaws effective April 28, decreasing the share capital slightly through reducing total shares outstanding from approximately 55.7 million to about 53.7 million at nominal value €0.025 per share [S3][S20]. Concurrently, Criteo is undergoing a strategic legal transformation via a cross-border conversion moving its registered headquarters from France to Luxembourg [S11][S18]. Shareholders overwhelmingly approved this move on February 27, 2026 [S15][S18]. This shift enables Criteo to replace its American Depositary Shares (ADS) ADR structure with ordinary shares directly listed on Nasdaq aimed at simplifying capital structure and potentially broadening investor access.

Business Model and Strategic Position

Criteo operates as a global commerce intelligence platform delivering technology solutions and insights primarily through two segments: Performance Media and Retail Media [S16]. The company monetizes its service offering by enabling brands, retailers, agencies, and publishers to optimize digital advertising spend through AI-driven targeting based on comprehensive commerce data derived from over $1 trillion in annual transactions.

Performance Media: Historically the core offering focuses on performance-based advertising across open web environments where Criteo employs machine learning models to engage shoppers at scale. Revenue derives mainly from advertisers paying for measurable clicks or conversions realized through personalized ads. Traffic acquisition costs (TAC) are material here due to programmatic media buying.

Retail Media: This segment has become increasingly strategic as retailers seek to monetize shopper intent within their ecommerce properties via sponsored product ads or display placements. Here Criteo leverages direct retailer relationships combined with its data analytics platform to facilitate demand generation for retail clients' first-party inventory at higher margins.

The revenue model depends on contractually negotiated rates that incorporate volume commitments, bid pricing tied to auction dynamics in digital advertising exchanges, and ongoing innovation in AI-powered targeting algorithms that aim at continuously improving campaign ROI for clients.

Operationally, Criteo differentiates itself through:

- Proprietary data scale: Unique access to vast transaction-level commerce datasets aggregated over two decades creates high-value predictive signals for ad personalization.

- AI advancements: Sophisticated machine learning frameworks enhance bidding decisions across multiple channels including web display, social media integration, and retailer networks.

- Ecosystem integration: Deep partnerships across global retail chains alongside digital publishers generate network effects enhancing client retention and switching costs.

Management under CEO Michael Komasinski brings extensive industry leadership experience advancing AdTech strategies aligned with shifting retail media landscapes [S26].

Industry Structure and Competitive Landscape

The AdTech ecosystem is characterized by rapid innovation cycles driven by advances in artificial intelligence, changes in consumer privacy regulations (e.g., GDPR, CCPA), evolving cookie deprecation impacts on targeting efficacy, and increasing retailer adoption of self-serve media platforms.

Criteo competes alongside major internet ecosystems (Google Ads, Meta Platforms), independent demand-side platforms (DSPs), retail media networks operated by large e-commerce players (Amazon Advertising), as well as emerging specialized providers focused exclusively on retail media.

While the broader digital advertising market remains highly competitive and fragmented:

- Criteo’s proprietary commerce dataset amassed over two decades provides differentiated predictive power relative to generic audience targeting platforms.

- Its hybrid business model straddling programmatic open web ads (Performance Media) and direct retail partnerships (Retail Media) helps hedge segment-specific cyclical pressures.

- Global footprint supports multinational clients seeking integrated campaign solutions across multiple regions where local competitive dynamics vary substantially.

Network effects stemming from sheer data volume combined with AI innovation reinforce high client retention metrics reported by management – cited same-retailer Contribution ex-TAC retention rates exceeded 110% excluding largest client scope reduction in 2025 [S24].

Growth Drivers

Several structural factors underpin Criteo’s growth prospects:

- Retail Media Expansion: Retailers increasingly allocate budget away from traditional brand advertising toward sponsored listings & digital shelf placements directly linked to purchase intent. As these ad budgets grow globally beyond early-adopter markets (e.g., US/Europe), Criteo benefits via both new client acquisitions and enhanced wallet share within existing relationships.

- AI Technology Evolution: Continued advancement in AI models allows deeper personalization amid increasing user privacy restrictions limiting deterministic identifiers. Investments enable better predictions using anonymized/contextual signals less vulnerable to regulation.

- Cross-Segment Synergies: Combining insights from Performance Media programmatic campaigns with first-party retailer data drives more holistic customer journey measurement - enhancing advertiser confidence in return-on-ad-spend (ROAS).

- Geographic Diversification: Expanding presence in emerging digital commerce markets may provide incremental growth avenues beyond mature regions where penetration is high.

KPIs linked closely include Contribution ex-TAC growth rates per segment, client retention percentages especially in Retail Media accounts, incremental bookings from new retailer onboarding initiatives, innovation milestones around AI deployment phases, and expanding inter-segment campaign synergies measured via increased cross-sell revenues.

Risks / Watchpoints / Growth Constraints

- Competitive Pressure: Dominant tech incumbents continuously invest heavily creating risk of margin compression as marketplace bidding costs rise or pricing discipline weakens due to commoditized offerings.

- Privacy & Regulatory Changes: Heightened scrutiny over consumer data usage creates uncertainty regarding future permissible analytics capabilities. Changes like browser tracking prevention or legislation limiting cookie usage increase reliance on alternate identity resolution strategies which are still nascent.

- Technological Execution Risks: Maintaining pace of AI innovation at scale demands ongoing R&D investment coupled with seamless platform scalability amid volatile traffic volumes – failures could hinder client satisfaction or reduce solution effectiveness.

- Customer Concentration & Scope Reduction: Dependence on a limited number of large retailer clients can impose volatility if scope contracts unexpectedly downward or agreements lapse - noted impact excluded for retention rate calculation emphasizes this sensitivity.

- Cross-Border Conversion Complexity: Transitioning legal domicile requires operational focus ensuring compliance continuity without disrupting investor relations or stock liquidity as ADS replacement occurs.

What to Watch Next

The near-term milestones requiring monitoring include:

- Successful completion of the cross-border conversion registration process with Luxembourg authorities culminating in effective domicile transfer date post-February 27 shareholder vote [S18][S19].

- Execution progress replacing ADS structure with ordinary shares listed directly on Nasdaq impacting liquidity metrics or trading dynamics.

- Quarterly result announcements demonstrating sustained momentum in Retail Media bookings offsetting any softness in Performance Media channels.

- Management commentary updating medium-term strategy around new AI capabilities deployment especially aligned with privacy-first targeting innovations.

- Any regulatory developments potentially affecting operational assumptions particularly concerning data governance post-GDPR adjustments worldwide.

Financial Snapshot (end of FY 2025)

Latest financial snapshot

| Metric | Value | Period |

|---|---|---|

| Cash & equivalents | $342mm | |

| 2025-12-31 | ||

| Current assets | $1072mm | |

| 2025-12-31 | ||

| Current liabilities | $845mm | |

| 2025-12-31 | ||

| Current ratio | 1.27x | |

| 2025-12-31 |

Source: SEC companyfacts cache [F1].

Overall, Criteo presents a business evolving toward higher margin Retail Media opportunities built upon enduring AI-enabled commerce insights while navigating competitive intensity and regulation-driven complexity inherent within digital advertising markets. The strategic move relocating legal domicile coupled with stable financial outcomes suggests disciplined management execution aiming for growth resilience amid industry transformation.

This analysis is strictly informational without investment advice or forecasts. It reflects SEC filing disclosures as of the dates cited combined with sector knowledge.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments