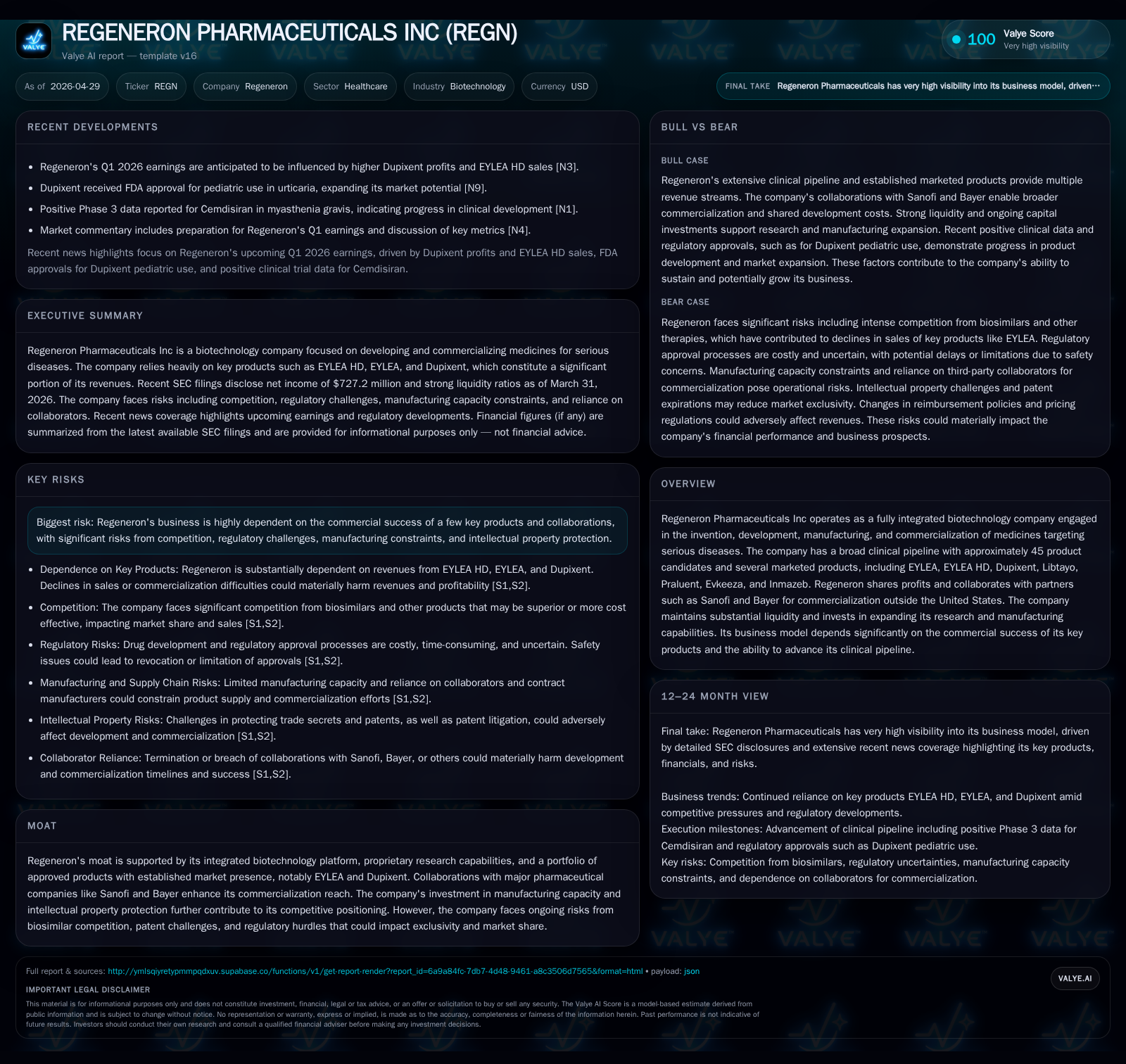

Regeneron Pharmaceuticals Faces Revenue Shifts as EYLEA HD Growth Offsets Competitive Pressures

Recent quarterly disclosures highlight Regeneron’s evolving product revenue mix amid intensifying competition and ongoing development investments.

Regeneron Pharmaceuticals' latest quarterly filing reveals a growing reliance on EYLEA HD to counterbalance declining sales of EYLEA due to increased biosimilar competition. Dupixent remains a critical revenue driver alongside a broad clinical pipeline supporting future growth. However, manufacturing capacity constraints and regulatory uncertainties pose risks. Collaborative partnerships with Sanofi and Bayer remain central to global commercialization efforts. The company’s substantial liquidity and investment in R&D underpin its integrated biotech platform, though market exclusivity challenges require close monitoring.

Recent Operating Update

In its April 29, 2026 Form 10-Q filing ([S2]), Regeneron Pharmaceuticals underscored significant shifts in product revenue dynamics during the first quarter ended March 31, 2026. The company disclosed that while legacy EYLEA sales have declined sharply—down 36% year-over-year in the U.S.—this drop was partially offset by robust growth in its next-generation formulation, EYLEA HD, which now accounts for 50% of combined U.S. sales for the two products ([S18]). This evolution highlights a pivotal transition phase potentially extending Regeneron's commercial leadership in retinal diseases despite biosimilar encroachment.

Additionally, Dupixent continued to solidify its role as a core revenue engine, supported by regulatory approvals expanding its use into pediatric populations with conditions like urticaria ([N11]). The company reported an acquired in-process research and development (IPR&D) charge of approximately $102 million related to recent collaboration license payments that impacted earnings for the quarter ([S5]).

Operationally, Regeneron emphasized ongoing investments in manufacturing capabilities to support scaling product supply amidst increasing demand across key biologics ([S1][S9]). Collaboration terms with Sanofi (notably Dupixent) and Bayer (notably EYLEA outside the US) remain integral to global commercialization strategies but introduce execution dependencies ([S7]).

Business Model

Regeneron operates as a fully integrated biotechnology company combining internal discovery, clinical development, manufacturing, and global commercialization capabilities ([S1]). It generates revenue predominantly through net product sales of approved biologic therapies—principally EYLEA (and now EYLEA HD), Dupixent, Libtayo, Praluent, Evkeeza, and Inmazeb—with substantial dependence on two franchises: EYLEA variants for retinal diseases and Dupixent for inflammatory conditions.

The firm’s business model involves deriving royalties or profit-sharing revenues through partnerships — notably with Sanofi for Dupixent commercialization outside North America and Bayer for EYLEA outside the U.S., allowing Regeneron to leverage partners’ marketing infrastructures while retaining strong margin profiles for direct U.S. sales ([S1]).

Revenue mechanics rest on volume growth of existing products via expanded indications and new formulations (e.g., EYLEA HD), pricing power supported by clinical differentiation, reimbursement by third-party payors—including Medicare/Medicaid—and contract terms with collaborators dictating profit splits or royalties ([S1][S2]). Research and development expenses are significant due to the expansive clinical pipeline (~45 candidates) aiming to replenish future product launches but are partially offset by collaborator reimbursements ([S1]).

Manufacturing is vertically integrated but supplemented by contracted fill/finish facilities; maintaining scale and quality manufacturing is vital given biologics’ production complexity and quality regulations ([S9]). Potential excess fixed costs or underutilized capacity represent financial risk if product launches falter or demand slows ([S14]).

Industry Structure and Competitive Position

Regeneron is positioned within the biotechnology sector as a leader focused on monoclonal antibodies targeting serious diseases across ophthalmology, immunology, oncology, cardiovascular disease, and infectious diseases. Its competitive advantages stem from its proprietary integrated platform enabling efficient discovery-to-manufacturing workflows and a portfolio anchored by market-leading products such as EYLEA—one of the top-selling ophthalmologic drugs worldwide—and Dupixent—a rapidly growing multi-indication immunology drug jointly commercialized with Sanofi ([S1], Valye Report Excerpt).

Collaborations with Sanofi and Bayer expand Regeneron's global commercial footprint but create operational dependencies that must be managed carefully to sustain revenues outside the United States ([S7]). Intellectual property protection underpins market exclusivity; however, biosimilar entrants particularly threaten legacy products like EYLEA as exclusivity periods expire or face patent challenges ([S9][S15]).

Pricing pressures across the healthcare ecosystem—in particular drug price reforms at federal and state levels—pose ongoing headwinds affecting reimbursement levels across all biologics. Established competitors include Amgen (noted competitor pipeline overlap), Roche (in oncology), Novartis (ophthalmology), among others. The crowded biosimilar field elevates competitive threat intensity over time ([N8],[N3]).

Growth Drivers

- Shift to EYLEA HD: The launch of the higher dose EYLEA HD formulation supports revenue stabilization as it commands differentiated clinical profiles allowing premium pricing compared to declining biosimilar-exposed older formulations ([S18]).

- Dupixent Indication Expansion: Regulatory approvals extending Dupixent into pediatric uses such as urticaria are expected to deepen patient penetration and revenue growth globally through Sanofi partnership co-commercialization ([N11],[N7]).

- Pipeline Advancement: Approximately 45 candidates in clinical development provide multiple shots on goal across diverse therapeutic areas including oncology (Libtayo expansions), cardiovascular disease (Evkeeza), Ebola (Inmazeb), creating multiple avenues for future market launches pending positive data ([S1],).

- Manufacturing Scale-Up: Continued investment in Rensselaer NY and Limerick Ireland facilities aims to address supply constraints expected from volume ramping of existing products along with new approvals; securing supply chain robustness is essential for uninterrupted commercialization ([S9],).

- Collaborative Licensing Transactions: Recent in-license acquisitions contributing upfront milestones reflect strategic asset augmentation fueling mid-term pipeline depth despite short-term earnings impact from acquired IPR&D charges ([S5],[N8]).

Risks / Watchpoints / Growth Constraints

- EYLEA Revenue Pressure: Legacy EYLEA faces steep declines due to increasing biosimilar competition leading to shrinking revenue bases; success hinges critically on whether EYLEA HD can compensate without cannibalization or substantial pricing concessions ([S18],[S15]).

- Dependency on Key Products: Substantial dependence on three principal products—EYLEA variants combined with Dupixent—creates vulnerability if these franchises fail to sustain approvals or competitive advantage ([S15],).

- Manufacturing Capacity Risks: Expansion timelines or cost overruns could disrupt supply or reduce profitability; underutilized capacity due to delayed launches could inflate fixed costs forcing margin pressure ([S9],[S14]).

- Collaborator Risks: Any breach or termination of agreements with Sanofi or Bayer would materially impair international commercialization capabilities impacting revenues significantly ([S7],[S11]).

- Intellectual Property Challenges: Biosimilar threats coupled with patent litigation risk could erode exclusivity periods more quickly than expected risking long-term revenue streams especially for older assets like EYLEA ([S9],).

- Pricing Environment: Emerging drug pricing policies at federal/state levels could constrain effective pricing power reducing net sales realization amid payer pushback ([S15],[N10]).

- Development Risk: High R&D spend with uncertain clinical outcomes poses inherent risk; failure to secure timely regulatory approvals or produce compelling trial data could delay or derail anticipated launches ([S1],[N8]).

What to Watch Next

Investors and observers should monitor the quarterly progression of:

- Quarterly net sales trends in both U.S. EYLEA HD and total Dupixent franchises to assess replacement rate of legacy declines.

- Clinical trial readouts from mid-stage pipeline candidates providing indications of future drug approval timing.

- Updates on manufacturing facility expansions including timing adherence and anticipated capacity increases.

- Collaborator performance metrics especially outside North America noting any early signs of partnership strain.

- Regulatory decisions pertaining to biosimilar entries challenging flagship products.

- Pricing policy changes via legislative developments around drug cost containment measures.

- Subsequent quarterly filings clarifying magnitude or recurrence of acquired IPR&D charges affecting earnings quality.

Latest Financial Snapshot

Latest financial snapshot

| Metric | Value | Period |

|---|---|---|

| Cash & equivalents | $3.0bn | |

| 2026-03-31 | ||

| Total debt | $3.5bn | |

| 2026-03-31 | ||

| Net debt | $524mm | |

| 2026-03-31 | ||

| Current assets | $18.2bn | |

| 2026-03-31 | ||

| Current liabilities | $5.1bn | |

| 2026-03-31 | ||

| Current ratio | 3.57x | |

| 2026-03-31 |

Source: SEC companyfacts cache [F1].

*Net Debt approximated as total debt less cash & equivalents [F1]

The company maintains a solid liquidity profile supportive of near-term operational needs including extensive R&D expenditure commitments. Although net debt is relatively modest compared to cash holdings, gross leverage remains notable requiring disciplined capital management particularly amidst continued acquisition activity reflected by IPR&D charges ([F1],[S5],).

This analysis synthesizes Regeneron Pharmaceuticals’ most recent operating disclosures with broader historical context emphasizing business model nuances critical for assessing its ongoing competitive resilience amidst evolving industry dynamics. While financial data offers snapshot support for liquidity assessment, strategic operating elements dominate forward looking considerations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments