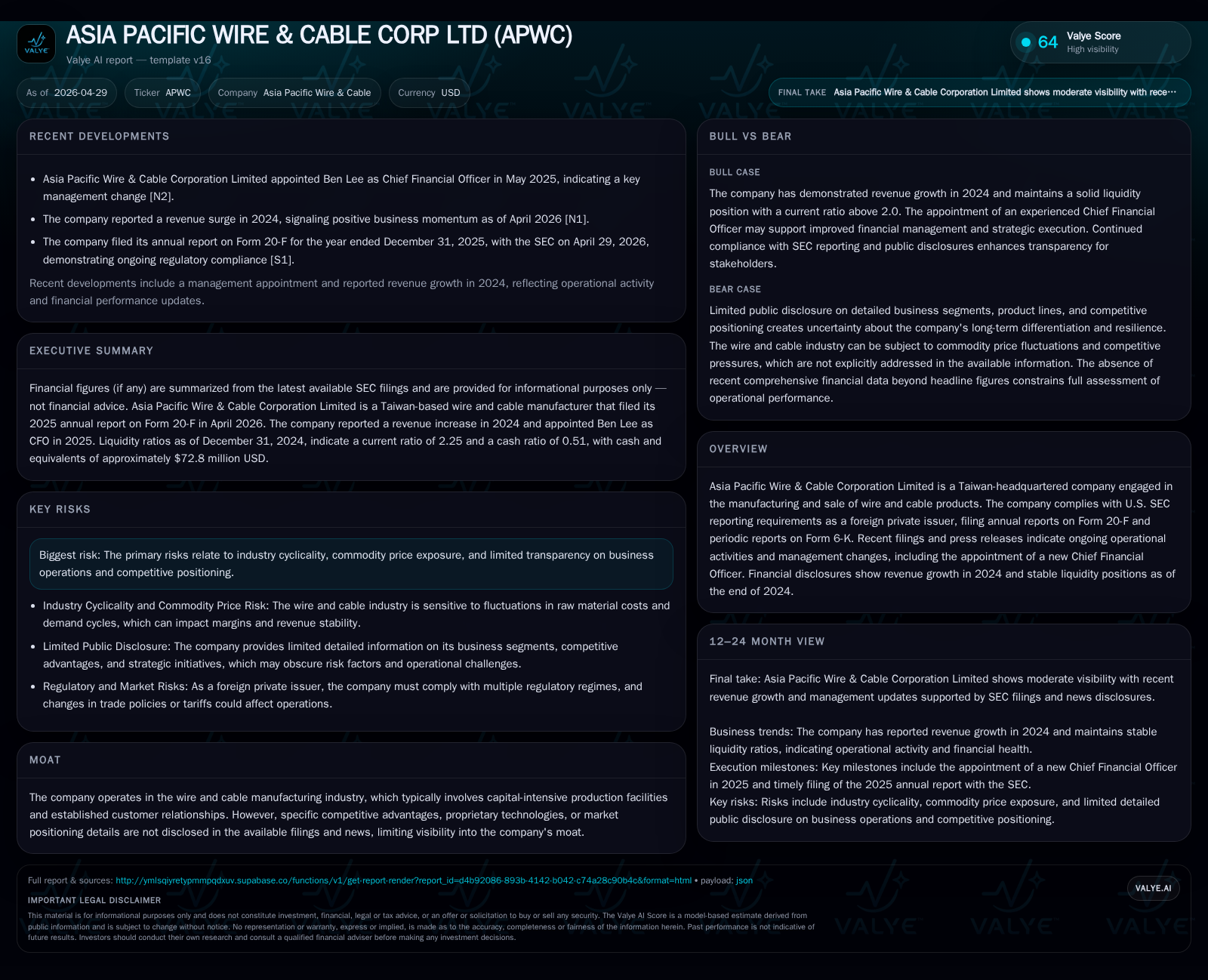

Asia Pacific Wire & Cable Posts Revenue Growth Despite Margin Pressure

The latest quarterly results reveal revenue gains for Asia Pacific Wire & Cable amid increased copper costs squeezing profit margins.

Asia Pacific Wire & Cable Corporation Limited reported a 3.6% revenue increase for the 2025 fiscal year, driven primarily by robust demand in the North Asia region. However, rising copper prices led to a decline in gross profit and operating profit margins, reflecting the challenge of passing through raw material cost increases fully and promptly. The company’s capital-intensive manufacturing business remains exposed to commodity price volatility and geopolitical trade tensions, yet ongoing infrastructure projects in core markets provide structural growth opportunities. Near-term prospects hinge on effective cost management, pricing adjustments, and monitoring copper price trends.

Latest Quarterly Operating Update: Revenue Growth Amid Cost Challenges

Asia Pacific Wire & Cable Corporation Limited disclosed its full-year and fourth-quarter results for the fiscal year ended December 31, 2025, via its April 29, 2026 Form 6-K filing [S2]. Reported revenue grew by 3.6% year-over-year to $489.7 million, buoyed largely by strong sales growth in the North Asia segment which surged 19% compared to the prior year [S1]. This top-line expansion was nonetheless accompanied by margin erosion — gross profit declined by 1.9% due to an increase in costs of sales outpacing revenue growth. Costs rose 4% mainly due to higher copper prices, with the average LME copper price increasing approximately 8.7% from $9,143 per metric ton in 2024 to $9,939 in 2025 [S1].

Operating profit contracted sharply by over a third (36.3%) from $10.0 million in 2024 to $6.4 million in 2025 [S1]. The North Asia region remained marginally profitable but at a markedly lower margin of 0.35% compared to a loss (-0.61%) the prior year [S1]. Meanwhile, Thailand’s operating margin fell to just under 2%, down from over 4%, while the Rest of World (ROW) segment held steady at around a 2.2% margin despite minimal revenue change [S1]. Corporate expenses also increased moderately further weighing on consolidated profitability [S1].

Overall, APWC’s latest quarterly reports highlight resilience in maintaining revenue growth amid rising input costs but also the persistent challenge of restoring sustainable margins given volatile copper prices that are difficult to fully and immediately pass onto customers.

Business Model and Product Portfolio Analysis

Asia Pacific Wire & Cable operates primarily as a manufacturer of wire and cable products serving multiple geographic markets segmented into North Asia, Thailand, and ROW [S1]. The business model centers on converting raw materials—chiefly copper—into value-added electrical cables for sale to infrastructure developers, industrial clients, and utilities.

The company generates revenues by selling these manufactured products at prices generally pegged to prevailing international copper spot prices with an attempted pass-through mechanism intended to mitigate raw material cost risk [S1]. However, price contracts sometimes lag behind commodity market movements leading to periods where APWC bears elevated costs that depress operating margins temporarily.

Production is capital intensive requiring maintained and periodically upgraded facilities capable of handling high-volume manufacturing runs with requisite quality standards demanded by infrastructure and construction sectors [S1]. APWC’s asset base spans its three segments with established customer relationships focusing on regional infrastructure growth drivers.

This value chain positioning places APWC as mainly a volume-driven processor of copper inputs rather than an innovator with proprietary technologies or high switching-cost offerings; thus it competes predominantly on product quality consistency, pricing competitiveness, and regional service capabilities.

Industry Structure and Competitive Positioning

The global wire and cable industry is highly sensitive to macroeconomic cycles given its heavy reliance on infrastructure investments and industrial capital projects [S1]. Demand within APWC’s key regions correlates strongly with government-led development initiatives plus broader economic activity.

Competition is intense both from other regional manufacturers and multinational firms with scale benefits. Pricing power is limited as customers exhibit some elasticity amid prevalent substitute suppliers; however product quality reliability and adherence to technical specifications remain critical differentiators.

Input cost volatility poses inherent challenges industry-wide since copper represents a large majority of production input costs [S1]. While hedging tools exist, timing mismatches between procurement costs and contract pricing often cause earnings variability.

Geopolitical trade issues—especially U.S.-China tensions noted as influencing APWC—add complexity through tariff uncertainties or supply chain disruptions potentially advantaging local competitors or complicating exports/imports [S1]. Currency fluctuations also affect cost structures given multi-currency operations across segments.

Growth Drivers and Strategic Opportunities

Revenue momentum in the North Asia region signifies strengthening demand linked closely to ongoing infrastructure expansions fueling cable consumption [N1][S1]. This region also provides a platform for potentially scaling sales volumes further amid favorable project pipelines.

Improved pricing mechanisms that shorten lag times between copper cost changes and product price adjustments would materially enhance margin stability [S1]. Operational excellence initiatives targeting efficiency gains could partially offset inflationary pressures on labor and overhead expenses.

Capacity utilization improvements leveraging existing manufacturing footprints might deliver incremental profitability without heavy capital reinvestment in the near term.

Emerging demand segments such as renewable energy grid expansions or smart city projects could offer longer-term diversification beyond traditional construction sectors if incorporated into product development strategies.

Risks and Constraints Impacting Future Performance

Copper price volatility remains APWC’s primary operational risk given its outsized impact on cost of sales [S1]. Price spikes expose the company during fixed-price contracts or when contract reset periods delay passing through higher costs.

Geopolitical uncertainties—including tariffs, trade restrictions, or diplomatic tensions—increase exposure to supply chain interruptions or unfavorable market access conditions across APWC’s diverse regional operations [S1].

Inflationary pressures extend beyond raw materials to labor and overhead costs which have risen over recent periods impacting overall cost structure [S1]. Currency exchange rate fluctuations create financial reporting complexity and operational risks despite active hedging policies [S1].

Limited disclosure on competitive differentiation restricts visibility into potential moats or strategic uniqueness leaving APWC vulnerable if competitors advance superior technologies or gain pricing advantages.

Key Upcoming Milestones and Market Signals

Investors should track subsequent interim filings after April 29, 2026 for insights into quarterly performance shifts post-peak copper prices reported early in 2026 (~$13,000 per ton in February) [S1]. This will clarify if margin pressure abates as input cost inflation moderates.

Management commentary around pricing strategy adjustments or new contract terms may signal improved pass-through effectiveness reducing earnings volatility.

Any announcement concerning capital expenditure plans aimed at capacity expansion or technological upgrades would be notable for long-term growth prospects.

Market signs of stabilized geopolitical conditions affecting supply chains would mitigate downside risks presently highlighted by regulatory filings.

Financial Overview Supporting Operating Trends

While detailed current liquidity data from recent filings is limited, historical balance sheet snapshots show comfortable cash balances relative to current liabilities suggesting stable short-term financial footing at end-2012 [F1]. No explicit updates on debt levels or leverage arisen from latest SEC periodic filings suggest no immediate refinancing risk or covenant pressure apparent through early 2026 disclosures [S2][S3][F1].

Profitability metrics reflect operational stresses primarily arising from external raw material cost shocks rather than internal solvency constraints. Finance costs slightly declined possibly reflecting improved debt conditions though finance income saw minor reductions year-on-year consistent with interest rate environments [S1].

Financial results thereby corroborate operating narratives underscoring manageable liquidity paired with earnings impacted by sector-specific cost cycles rather than fundamental financial distress.

This analysis synthesizes Asia Pacific Wire & Cable Corporation Limited’s recent SEC-reported operating performance alongside its structural industry position within the global wire manufacturing sector. The company exhibits top-line growth underpinned by geographic demand variances but contends with margin volatility manifested through copper commodity price dynamics—a consistent theme across this capital-intensive manufacturing space. Near-term outcomes rest upon balancing customer pricing responsiveness against input inflation while leveraging steady production capacity amidst geopolitically influenced market complexities.

This memorandum is provided solely for informational purposes without any recommendation regarding securities transactions.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments