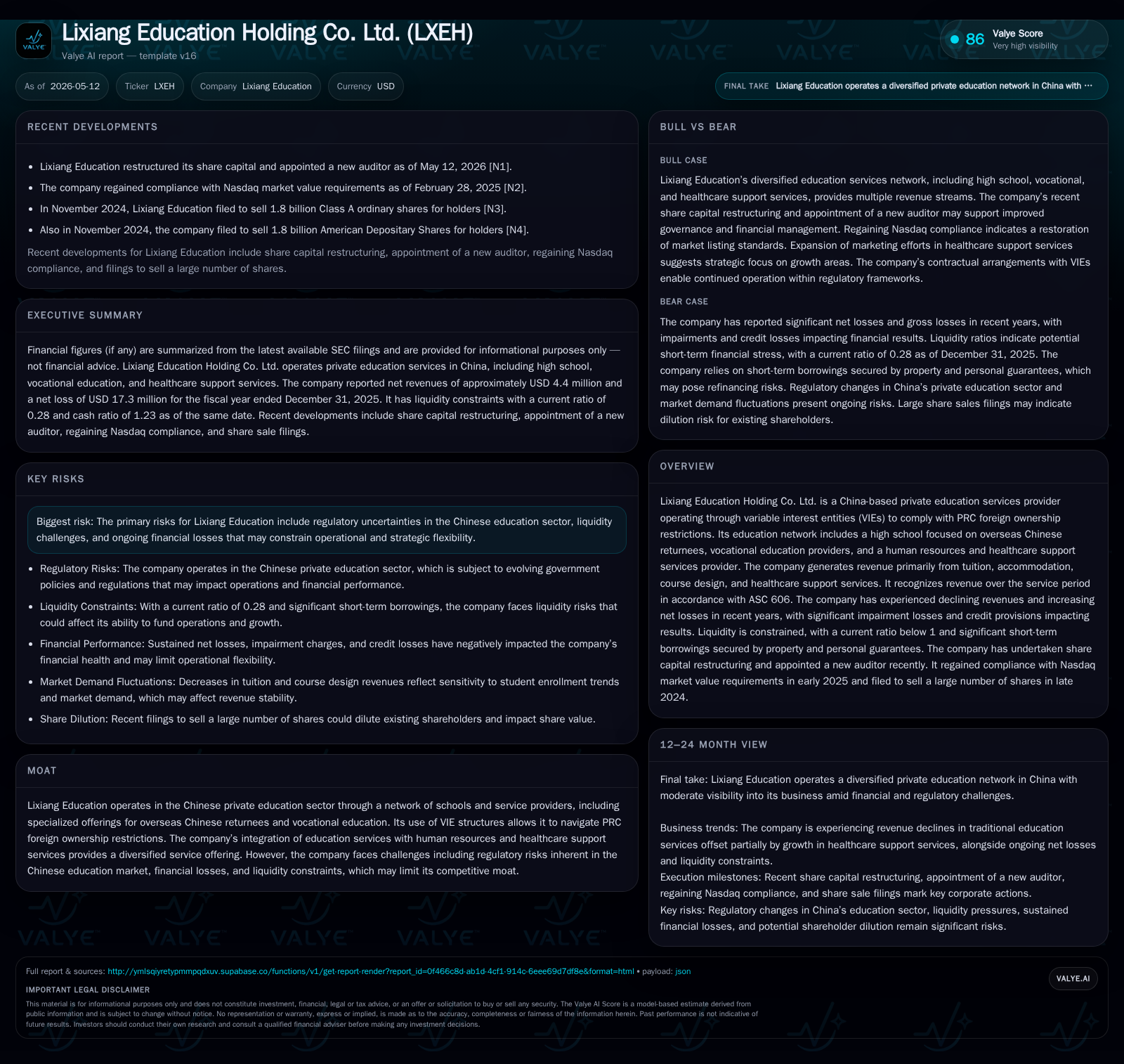

Lixiang Education Faces Intensified Financial Pressure Amid Declining Revenues and Liquidity Constraints

Recent quarterly disclosures highlight continued revenue declines, widening losses, and pressing liquidity challenges for Lixiang Education.

Lixiang Education Holding Co. Ltd., a China-based private education provider focused on overseas Chinese returnees and vocational training, reported further revenue declines and increased net losses in its latest quarter. The company’s current ratio remains severely depressed at 0.28, evidencing acute liquidity stress, while operating losses widen primarily due to rising costs and limited pricing flexibility amid regulatory constraints. Its business model combines high school education, vocational services, and healthcare support under a complex VIE structure that navigates PRC foreign ownership restrictions but also exposes it to regulatory uncertainties. Growth is constrained by shrinking student enrollments and cost pressures, while efforts to diversify into healthcare support have yet to offset core operational weaknesses. Monitoring capital raises, debt refinancing, and enrollment trends will be critical going forward.

Recent Operating Update

Lixiang Education Holding Co. Ltd.'s latest interim filings dated April 2026 reaffirm the company’s challenging near-term operating environment [S2][S3]. Although specific operating metrics were scant in these latest reports beyond procedural disclosures related to an ADS ratio change announcement, the annual filing on May 12, 2026 [S1] provides critical context illustrating ongoing revenue contractions coupled with mounting losses.

Net revenues declined by approximately 6% from RMB32.8 million in 2024 to RMB30.8 million (~$4.4 million USD) in 2025 [S10]. This drop was largely driven by reduced tuition and accommodation fees due to a graduating class outnumbering new enrollments at its vocational institutions plus diminished demand for course design services. Only healthcare support services bucked this trend with an uplift of RMB1.8 million over the period.

Costs surged disproportionately; cost of revenues jumped 19.3% due mainly to newly launched healthcare support services representing increased operational complexity alongside rising site rental expenses [S10]. Consequently Lixiang posted a gross loss margin of -38.7%, a steep deterioration versus prior years.

General administrative expenses edged slightly higher despite cost controls while marketing spend markedly increased reflecting efforts to grow healthcare services [S20]. Operating losses widened 40% year-over-year to RMB36.4 million (~$5.2 million USD), compounded by a rise in interest expense tied to prolonged borrowings [S10]. Net loss expanded drastically by nearly four-fold to RMB121 million (approx $17.3 million) [S20], underscoring intensifying financial strain.

Liquidity remains severely constrained: the company's current ratio stands at a precarious 0.28 as of December 2025 — current liabilities exceeding current assets roughly fourfold — raising concerns about near-term cash solvency without additional funding [F1]. The firm carries significant short-term secured borrowings (~RMB84 million or $12 million USD) backed by its own properties plus personal guarantees from related parties [S4][S6]. Despite ongoing deficits threatening operations over the next twelve months without further capital inflows or cost restructuring plans [S4], management is reportedly exploring multiple financing avenues including share issuance and cost efficiencies.

Business Model

Lixiang Education operates as a holding entity with no direct material operations; it conducts all substantive educational activities through wholly foreign-owned subsidiaries (WFOEs) and variable interest entities (VIEs) within mainland China [S1]. This layered structure complies with PRC regulations restricting foreign ownership in private education providers.

Its educational portfolio focuses primarily on two segments:

- High School Education: Delivered via Lishui International School targeting overseas Chinese returnees returning from abroad — a niche demographic requiring specialized curriculum aligned with international standards and reintegration support.

- Vocational Education: Provided through Langfang School and Hainan Jiangcai offering practical job-oriented programs designed to enhance employability in sectors such as technical trades.

Additionally, Hebei Chuangxiang serves as an ancillary human resources provider offering student internship placement alongside daily healthcare and elderly care services in collaboration with external partners [S1]. These complementary offerings aim to diversify revenue bases beyond classical tuition dependency.

Revenue is predominantly generated through upfront tuition payments often bundled with accommodation fees; these payments are recorded as contract liabilities initially then recognized evenly over the academic period according to ASC 606 [S21]. Additional income streams include bespoke course design/development projects—largely serving vocational partners—and healthcare service provision fees linked to senior care engagements.

Margins are pressured by significant fixed costs such as property leases (including dormitory facilities), staff salaries required for educational quality maintenance, and higher compliance-related expenditures necessitated under evolving regulation [S10][S19]. The company has made recent marketing investments principally aimed at enhancing awareness of its growing healthcare support segment though overall brand strength remains modest outside regional catchment areas.

Industry Structure and Competitive Position

China's private education sector is characterized by intense regulatory oversight that periodically reshapes competitive dynamics through restrictive licensing requirements, curricular examination mandates, limits on tuition pricing, and caps on enrollment quotas [S1]. The government's focus on standardizing educational quality while controlling access has created structural challenges for mid-sized regional players like Lixiang who do not possess scale-enabled cost advantages or dominant brand recognition.

Competition ranges from large national chains leveraging extensive networks across multiple provinces to boutique schools specializing in international curricula or niche vocational programs. Lixiang's differentiation derives chiefly from its tailored focus on overseas Chinese returnees—a demographic underserved relative to major urban centers—and its integration of human resources placement plus healthcare support services creating cross-selling opportunities albeit limited currently.

However, sustained financial underperformance undermines Lixiang’s ability to invest in pedagogical innovation or campus infrastructure enhancements that competitors may use to cement their market share. Moreover, reliance on VIE contractual structures exposes it indirectly but critically to policy risk connected with shifting government stances towards foreign participation in education sectors.

Growth Drivers

Near-term growth prospects hinge chiefly on three vectors:

- Healthcare Support Services Expansion: This recently scaled segment contributed RMB1.8 million incremental revenue in 2025 despite overall downturn elsewhere [S10], indicating latent demand for integrated elderly/healthcare service provision tied to vocational traineeships or community partnerships.

- Stabilizing Vocational Education Enrollment: Mitigating attrition caused by graduating cohorts outsizing new admissions at Langfang School through enhanced recruitment could reduce revenue erosion from core operations.

- Leveraging High School Curriculum for Overseas Chinese Returnees: Expanding grade levels (noted addition of second-year classes) can increase per-student lifetime value if retention improves substantially [S12].

Incremental marketing investments signal management's recognition of the need for focused demand generation initiatives particularly supporting newer healthcare lines which bear higher unit costs but potentially more scalable revenue streams if developed skillfully.

Risk Factors / Constraints

Lixiang’s principal risks include:

- Regulatory Uncertainty: Ongoing reforms targeting private education providers could restrict permissible fee structures or operational scopes fundamentally reshaping business viability.

- Liquidity Risk: Current assets cover less than one third of short-term liabilities creating acute refinancing risk particularly given dependence on secured loans backed by limited collateral [F1][S4].

- Operational Losses: Escalating net losses (> $17M USD in FY25) erode equity cushion impairing capacity for investment or absorbing shocks from adverse external events.[F1][S10][S20]

- Contractual Structure Dependence: Use of VIE structures circumvents ownership limits but subjects firm earnings rights and asset access contingent on counterparties’ contractual compliance which may invite enforcement risk.[S1]

- Market Demand Cyclicality: Reflective of broader demographic pressures reducing student cohorts combined with muted willingness/ability of families to pay premium tuition compressing volume-price drivers.

- Cost Inflation Pressure: Rising site rent obligations alongside increased staffing/marketing costs without commensurate revenue expansion depress margins further.[S10]

What To Watch Next

Investors and analysts should closely monitor:

- Announcements regarding capital raising activities or debt refinancing which will be pivotal given current working capital deficits[ S4[S6]].

- Enrollment statistics reported each semester at primary schools including any changes following regulatory pivot points affecting admission policies.[N1]

- Regulatory updates impacting allowable tuition fees or approval processes for expansions that could alter competitive dynamics.[S1]

- Quarterly operating metrics tracking progress in driving healthcare service revenue growth versus cost trajectory.[S20]

- Cash flow statements signaling sustainability improvements or deepening stress.[S5][F1]

- Management commentary around strategic pivots focusing on operational efficiency or asset monetization strategies.[N1]

Financial Profile Summary

Latest financial snapshot

| Metric | Value | Period |

|---|---|---|

| Cash & equivalents | $1827923 | |

| 2025-12-31 | ||

| Current assets | $5mm | |

| 2025-12-31 | ||

| Current liabilities | $18mm | |

| 2025-12-31 | ||

| Current ratio | 0.28x | |

| 2025-12-31 |

Source: SEC companyfacts cache [F1].

| Metric | Value | Period Ending |

|---|---|---|

| Revenue | $4.41M | |

| 2025-12-31 | ||

| Operating Income | -$5.20M | |

| 2025-12-31 | ||

| Net Income | -$17.43M | |

| 2025-12-31 | ||

| Cash & Equivalents | $1.83M | |

| 2025-12-31 | ||

| Current Assets | $4.89M | |

| 2025-12-31 | ||

| Current Liabilities | $17.77M | |

| 2025-12-31 | ||

| Current Ratio | 0.28x |

These figures reinforce the conclusion that Lixiang remains burdened by consistent negative cash flows exacerbated by thin liquidity buffers limiting maneuverability amid adverse market conditions.

Disclaimer: This analysis is based exclusively on public SEC filings and related information as of May 12, 2026. It does not constitute investment advice nor an endorsement of any securities mentioned herein.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments