Talphera Advances Nafamostat Therapy Development with Key Clinical and Capital Updates

The latest quarterly filing highlights Talphera’s clinical progress on its lead nafamostat candidate alongside capital position challenges and supply chain dependencies.

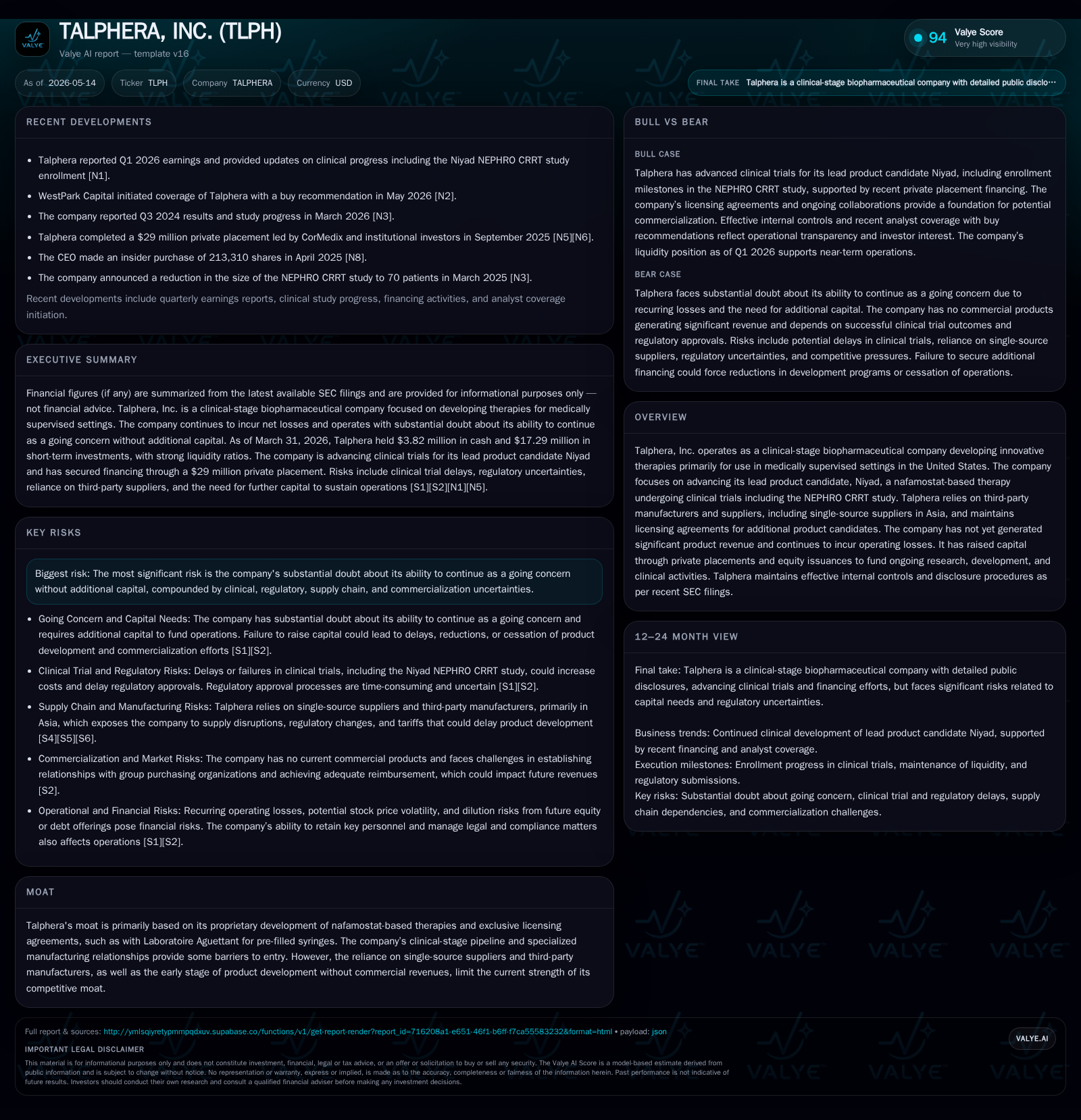

Talphera, Inc. remains a clinical-stage biopharmaceutical company focusing on developing nafamostat-based therapies, with its lead candidate Niyad advancing through clinical trials including the NEPHRO CRRT study. The company’s May 2026 10-Q confirms ongoing research activities and effective internal controls but reiterates significant financial constraints that cast doubt on its near-term going concern status. Talphera’s strategic moat derives from proprietary licensing agreements and specialized manufacturing partnerships, although reliance on single-source suppliers in Asia poses operational risks. Near-term growth hinges on key clinical milestones and potential regulatory filings while managing funding needs and supply chain uncertainties.

Latest Quarterly Operating Developments and Their Strategic Implications

Talphera’s May 2026 Form 10-Q filing substantiates continued efforts to advance its flagship nafamostat therapy candidate, Niyad, notably within its NEPHRO CRRT clinical trial program [S2]. The quarterly report affirms stable internal disclosure controls under management oversight with no material modifications since the prior period, suggesting steady operational governance despite the company’s developmental stage [S2]. Concurrently filed Form 8-K supplements these disclosures with a corporate update highlighting no significant deviations from prior clinical or financial plans [S3], with press release commentary confirming ongoing trial activity but underscoring capital challenges.

Notably, the filings reiterate Talphera’s reliance on third-party manufacturers for both active pharmaceutical ingredients (APIs) sourced from Japan and drug product formulation primarily outsourced to China [S2], spotlighting geographic concentration as an operational dependency. The management assessment of internal controls also provides assurance of procedural rigor amid the complex biopharma regulatory environment [S2]. However, consistent with earlier reports, the filings emphasize recurring operating losses without near-term commercial revenues, sustaining concerns over sustaining operations absent new capital infusion [S2].

Clinical-Stage Biopharmaceutical Model: Product Pipeline and Revenue Outlook

Talphera’s business model revolves around clinical-stage development of nafamostat-based therapeutics targeted for niche medically supervised inpatient applications across the U.S. healthcare system [S1]. Its lead product candidate Niyad is positioned primarily as an anticoagulant for continuous renal replacement therapy (CRRT), reflecting a highly specialized usage setting that demands rigorous clinical validation before market access. The company also holds licenses to ephedrine and phenylephrine pre-filled syringes via an exclusive commercialization agreement with Laboratoire Aguettant—a relationship that extends the IP estate but remains contingent upon successful U.S. FDA approval [S1][S27].

Despite this strategic breadth, Talphera has yet to generate meaningful product revenue, consistent with an investigational status typical of small biotechs intensely focused on phased clinical trials [F1][S1]. Revenue drivers will depend heavily on future regulatory milestones and subsequent commercialization capabilities either internally developed or through collaborations. Margins remain negative due to substantial research expenditures and manufacturing outsourcing costs that limit near-term operating profitability [F1]. The revenue mechanics are fundamentally driven by milestone-dependent licensing fees or future product sales to institutional healthcare providers post-approval.

Industry Landscape: Competitive Dynamics, Licensing, and Manufacturing Relationships

Operating in the competitive biotech sector targeting critical care therapeutics places Talphera within an intensive capital and regulatory cycle environment where early-stage clinical data shape valuation inflections and partnership prospects [S1][S6]. The company leverages exclusive licensing deals—for instance with Laboratoire Aguettant for US commercialization rights to pre-filled syringes—offering intellectual property leverage that can act as a moat against purely generic competition [S27].

However, Talphera’s dependency on single-source suppliers in Asia for APIs manufactured in Japan and final product formulation in China introduces notable supply chain risks especially amid rising geopolitical tensions and evolving international trade policies affecting tariffs and export controls [S2][S6][S16]. This constrains operational flexibility compared to vertically integrated competitors who control manufacturing internally. Additionally, the absence of internal manufacturing facilities makes Talphera vulnerable to vendor disruptions or price fluctuations inherent in contract manufacturing organizations (CMOs).

Capital intensity remains high industry-wide due to extensive regulatory compliance obligations—including Good Manufacturing Practices (GMP) enforcement—and costly Phase 3 clinical trials required for FDA approval. Thus, partnership strategies are essential for mitigating costs through shared development or licensing revenues [S1]. Yet commercial independence only materializes once substantive regulatory events occur.

Key Growth Drivers in Clinical Milestones and Commercial Readiness

The primary near-term growth trigger lies in obtaining positive clinical trial readouts from the NEPHRO CRRT study evaluating Niyad’s safety and efficacy as a regional anticoagulant in dialysis settings [S2][N1]. Successful demonstration of statistically significant endpoints would underpin potential FDA submissions initiating New Drug Application (NDA) review cycles—a pivotal gateway towards commercial launch authorization. Regulatory filings stimulated by compelling Phase 2/3 trial results can also increase licensing negotiation leverage or attract strategic alliances aimed at distribution scale-up.

Additionally, collaborations enhancing manufacturing scale or expanding product indications beyond CRRT represent supplementary value drivers. The exclusive agreement with Laboratoire Aguettant offers optionality to capitalize on commercial synergies if pre-filled syringes obtain approval thereby diversifying revenue streams [S27]. Robust patient enrollment rates or safety profile confirmations during ongoing trials will further validate technical feasibility sustaining investor confidence.

Risks Including Financing Needs, Supply Chain Constraints, and Regulatory Hurdles

Talphera’s most pressing risk stems from its precarious financial condition—latest disclosures state approximately $3.8 million cash on hand as of March 31, 2026 versus high burn rates inherent to late-stage biotech research programs [F1][S2]. The company explicitly warns of substantial doubt regarding going concern status absent timely capital raises. Given limited current liquidity juxtaposed against persistent operating losses exceeding $13 million annually last reported [F1], replenishing funding through equity issuances or partnerships is imperative though may be dilutive.

Supply chain concentration risk is pronounced due to reliance on single-source Asian suppliers whose operations could be disrupted by geopolitical tensions or tariff impositions consistent with recent U.S. trade policies impacting pharmaceutical ingredients [S2][S6][S19]. Additionally, prior FDA Warning Letters related experience adds regulatory scrutiny pressure increasing hurdles for approvals or marketing claims compliance—as reflected by ongoing securities litigation that was dismissed but underscores reputational sensitivity [S14][S15].

Legal risks also include potential exposure from patent infringement claims common in high-IP-value biotech arenas plus compliance risks associated with healthcare fraud statutes or improper promotion allegations under FDA regulations which have triggered enforcement actions industry-wide [S8][S22]. Any such adverse outcomes could divert management resources and inhibit commercialization efforts.

Milestones and Market Signals to Monitor in Upcoming Quarters

Investors should closely evaluate interim or final data releases from ongoing Niyad efficacy studies as these represent binary catalysts influencing valuation trajectories. Additionally, feedback or acceptance from FDA meetings regarding submission packages will offer early insight into regulatory receptivity shaping approval timelines.

Capital raising announcements—both equity issuances given share price pressure below Nasdaq minimum bid price threshold recently notified—and prospective collaboration deals expanding manufacturing capacity or co-commercialization would signal greater financial resilience.

Monitoring group purchasing organization (GPO) relationships post-approval will also provide visibility into real-world adoption chances within hospital procurement frameworks constrained by price sensitivity and supplier reliability concerns [S12]. Secondary market developments such as analyst ratings changes or shifts in trading volume may reflect evolving investor sentiment linked directly to these operational milestones.

Financial Snapshot: Liquidity, Capital Access, and Cash Runway

Latest financial snapshot

| Metric | Value | Period |

|---|---|---|

| Cash & equivalents | $4mm | |

| 2026-03-31 | ||

| Current assets | $21mm | |

| 2026-03-31 | ||

| Current liabilities | $4mm | |

| 2026-03-31 | ||

| Current ratio | 5.3x | |

| 2026-03-31 |

Source: SEC companyfacts cache [F1].

| Metric | Value (USD) |

|---|---|

| Cash & Equivalents | $3,823,000 |

| Current Assets | $21,336,000 |

| Current Liabilities | $4,025,000 |

| Current Ratio | 5.3 |

As of Q1 2026 end, Talphera maintains approximately $3.8 million in cash equivalents supporting working capital adequacy reflected by a strong current ratio of 5.3 derived from sizeable short-term assets relative to liabilities [F1]. Nonetheless, total debt figures dated back years earlier are not indicative of present leverage but net debt appears minimal [F1]. The principal financial challenge remains bridging substantial cash burn requirements associated with late-stage clinical trials before revenue realization becomes feasible.

While this snapshot illustrates an adequate immediate liquidity cushion for operational continuity in coming months, management's expressed intent to seek additional external financing underscores persistent inherent funding insecurity characteristic of early-stage biopharmaceutical innovation ventures dependent on episodic capital markets access.

This analysis is based solely on publicly available SEC filings up to May 13, 2026 and recent news transcripts without any forward-looking investment advice. It aims to provide a grounded understanding of Talphera's operational positioning in the evolving biopharmaceutical landscape focusing on nafamostat therapies.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments