Launchpad Cadenza Acquisition Sets Stage with Strengthened Governance and Solid Trust Liquidity

Latest quarterly disclosures reveal Launchpad Cadenza’s robust liquidity and governance enhancements positioning it for its upcoming business combination deadline.

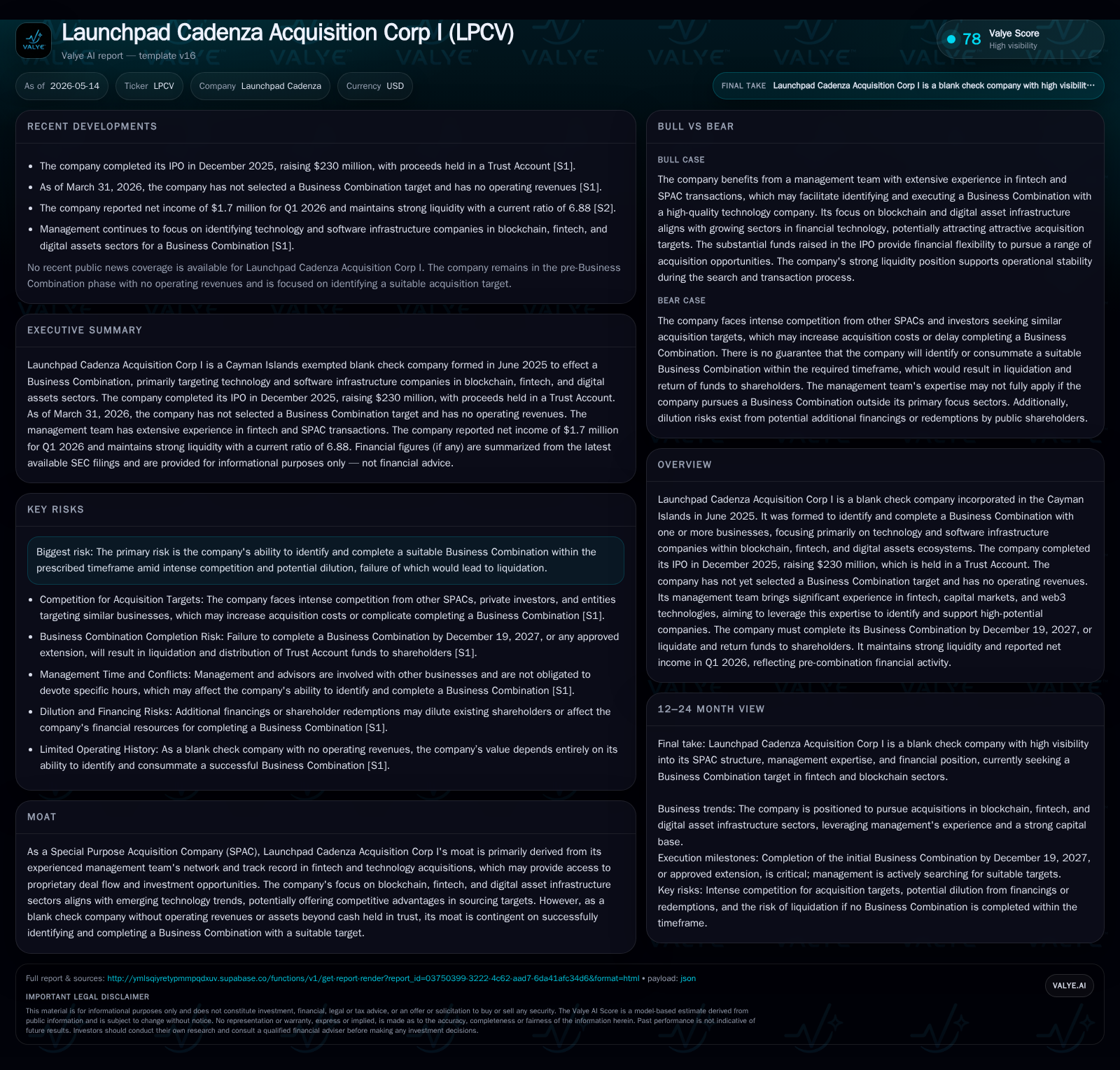

Launchpad Cadenza Acquisition Corp I, a Cayman-based blank check company focused on blockchain, fintech, and digital asset infrastructure targets, reported strong liquidity and a key governance shift in its most recent quarterly filing dated May 14, 2026. Despite lacking operating revenues as typical for SPACs pre-deal, the company posted net income reflecting minimal operating costs and maintains over $230 million in trust funds from its December 2025 IPO. The April 2026 appointment of Sheldon Sussman as audit committee chair signals an emphasis on governance rigor ahead of the business combination deadline by December 19, 2027. LPCV operates in a highly competitive SPAC ecosystem targeting tech-enabled financial services businesses with recurring revenue models and defensible technology positions. Critical growth vectors hinge on selecting a target with scalable software infrastructure in the emerging digital finance sector. Primary risks include intense deal competition, financing dilution, and deadline pressures. Key near-term milestones will be the announcement and shareholder approval of an initial business combination.

Latest Quarterly Developments and What They Signal

Launchpad Cadenza Acquisition Corp I’s (LPCV) latest quarterly report filed on May 14, 2026 [S2] provides valuable insight into the company’s current operational footing as it advances toward its Business Combination deadline set for December 19, 2027. A standout development is the board appointment of Sheldon Sussman as chair of the Audit Committee effective April 14, 2026 [S3]. Mr. Sussman brings deep expertise in asset-backed private credit origination and has a substantial track record of executing SPAC-related fintech investments. This leadership change reflects LPCV’s efforts to bolster governance controls crucial for vetting prospective targets and navigating regulatory complexities associated with SPAC mergers.

Financially, while LPCV remains pre-revenue—a norm for blank check vehicles without completed acquisitions—it reported net income by period end December 31, 2025 supported by limited operational expenditures [F1]. More importantly, the trust account established post-IPO currently secures roughly $230 million raised in December 2025 [S1], alongside working capital reflected through a strong current ratio of 6.88 at quarter-end March 31, 2026 [F1]. These liquidity reserves afford LPCV substantial maneuvering room to negotiate sizeable transactions or support follow-on funding needs without imminent capital constraints.

Company Structure, Business Model, and Sponsor Expertise

Launched as a Cayman Islands exempted company in June 2025 [S1], Launchpad Cadenza Acquisition Corp I operates as a Special Purpose Acquisition Company (SPAC) that raises capital through an initial public offering—$230 million in December 2025—to identify promising blockchain, fintech infrastructure, and digital asset ecosystem companies for acquisition. The company’s business model centers on deploying this pool of cash into one or more acquisitions (Business Combinations) that provide public listing benefits to private firms seeking capital market access but wish to avoid the protracted traditional IPO route [S1].

Until such transactional execution occurs, LPCV does not generate operating revenues but incurs minimal costs managing corporate affairs; these characteristics explain the modest net income disclosed despite no underlying operating activity [F1][S2]. The management team leverages significant sector expertise across fintech innovation and web3 technologies to source proprietary deal flow; this specialization serves as their moat in an otherwise commoditized blank-check market [S1][S6]. The sponsor's strategic focus includes targeting companies underpinning next-generation financial services such as digital custody solutions, on-chain analytics platforms, compliance tools utilizing identity technologies, tokenization frameworks, and institutional settlement infrastructures.

SPAC Industry Environment and Competitive Positioning

LPCV functions within an intensely competitive SPAC market with numerous contemporaries vying for quality fintech and blockchain sector acquisitions [S4]. The supply-demand imbalance for high-growth software infrastructure businesses has become pronounced as multiple well-capitalized blank check entities chase overlapping targets—often compelling target companies to demand premium valuation terms or improved deal structures that may inflate acquisition costs or delay announcements.

Launchpad Cadenza attempts differentiation by applying rigorous acquisition criteria emphasizing free cash flow sustainability, cash-flow positivity with consistent margin retention potential, recurring revenue dominance or platform scalability advantages, plus seasoned management teams capable of leading successful publicly listed companies [S4]. Strategic flexibility also permits transactions outside primary sectors where attractive value emerges but acknowledges potential trade-offs due to less domain relevance [S1].

Pricing power remains limited given prevalent competition; however, Launchpad’s strong management network and fintech domain credentials aim to alleviate some access challenges relative to generic SPAC players lacking specialized deal origination pipelines [S17].

Growth Opportunities Driven by Target Selection Focus

The path toward value creation for LPCV lies predominantly in consummating a Business Combination with an enterprise demonstrating compelling fundamentals within their core thematic sectors: blockchain infrastructure or fintech software platforms with broad addressable markets [S1][S6]. Ideally such targets exhibit recurring revenue streams underpinning predictable cash flows coupled with scalable economics driven by technology defensibility—for example custody platforms securing digital assets at institutional scale or compliance/identity systems facilitating regulatory adherence across geographies.

Being part of a public entity can unlock multiple benefits for these targets including efficient access to equity/debt markets for growth capital injections or acquisition rollup strategies that enable rapid market consolidation fueled by share currency availability—and enhanced employee retention via stock-based incentives [S4][S5]. Additionally, pioneering involvement in enabling decentralized finance ecosystems or digital asset settlement networks may position combined entities at the cutting edge of evolving financial technologies that enjoy favorable secular growth trends.

Risks and Challenges Ahead of Business Combination Deadline

A principal vulnerability facing Launchpad Cadenza is nestled within the tight timeline imposed by regulatory framework: failing to close a Business Combination before December 19, 2027 mandates liquidation and return of funds absent upside returns [S1][S2]. In an environment saturated with competing bidders pursuing similar fintech/blockchain targets—some backed by larger war chests or strategic buyers—there is notable risk around sourcing appropriate deals meeting LPCV’s criteria without unacceptable dilution.

Potential dilution arises if additional equity or convertible debt issuances become necessary due to higher-than-expected purchase price requirements or elevated shareholder redemptions exercising rights upon deal announcement [S9][S13]. Such dilution could materially erode Public Shareholder equity stakes if not managed prudently. Moreover, given the novelty of many targeted businesses’ control environments (especially startups or early-stage ventures), integration risks including Sarbanes-Oxley compliance ramp-up costs introduce execution uncertainty [S12]. Finally shareholder voting risks remain material—failure to secure approval would imperil completion prospects despite expended resources.

Key Milestones to Monitor in Near Term

Key indicators signaling progression toward value inflection will center on the timing of an announced Business Combination target along with associated shareholder proxy materials or tender offer documentation complying with SEC disclosure mandates including audited financial statements prepared under GAAP or IFRS standards if cross-border transactions apply [S12][S25]. Investors should track voting outcomes closely since approvals unlock subsequent liquidity events while also monitoring sponsor-related financing initiatives that may precede or coincide with deal closings.

Launchpad’s recent governance move in appointing Mr. Sussman as audit committee chair can be interpreted as preparatory groundwork enhancing fiduciary oversight capabilities ahead of such announcements [S3]. Progress updates on potential partnerships or definitive agreements will be pivotal in gauging transactional momentum.

Current Financial Position and Liquidity Insights

Latest financial snapshot

| Metric | Value | Period |

|---|---|---|

| Current assets | $1198787 | |

| 2026-03-31 | ||

| Current liabilities | $174152 | |

| 2026-03-31 | ||

| Current ratio | 6.88x | |

| 2026-03-31 |

Source: SEC companyfacts cache [F1].

From a financial perspective anchored by data reported at quarter-end March 31, 2026,[F1] illustrates LPCV's resilient balance sheet structure:

| Metric | Amount (USD) |

|---|---|

| Current Assets | 1,198,787 |

| Current Liabilities | 174,152 |

| Current Ratio | 6.88 |

| These figures underscore ample working capital well beyond immediate obligations reflecting conservative cost management characteristic of pre-combination SPACs. More critically,the $230 million raised through the IPO remains secured in the Trust Account dedicated exclusively toward funding the initial Business Combination transaction per regulatory requirements[S1]. |

Operationally insignificant expenses yield modest positive net income as accounted through late 2025[F1], reinforcing minimal burn risks absent deployment activities. Collectively,this financial setup affords Launchpad Cadenza sufficient runway to engage effectively in competitive bidding processes while maintaining market confidence through sound governance mechanisms.

This analysis leverages information from Launchpad Cadenza Acquisition Corp I's latest SEC filings up to May 14th, 2026 without conjecture beyond provided facts. Readers should note that all numeric figures are cited directly from official disclosures ensuring precise grounding.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments