Medicus Pharma’s Unfolding Quest: From Clinical Trials to Commercial Viability

Exploring Medicus Pharma's financial evolution and strategic challenges at a pivotal early clinical development juncture.

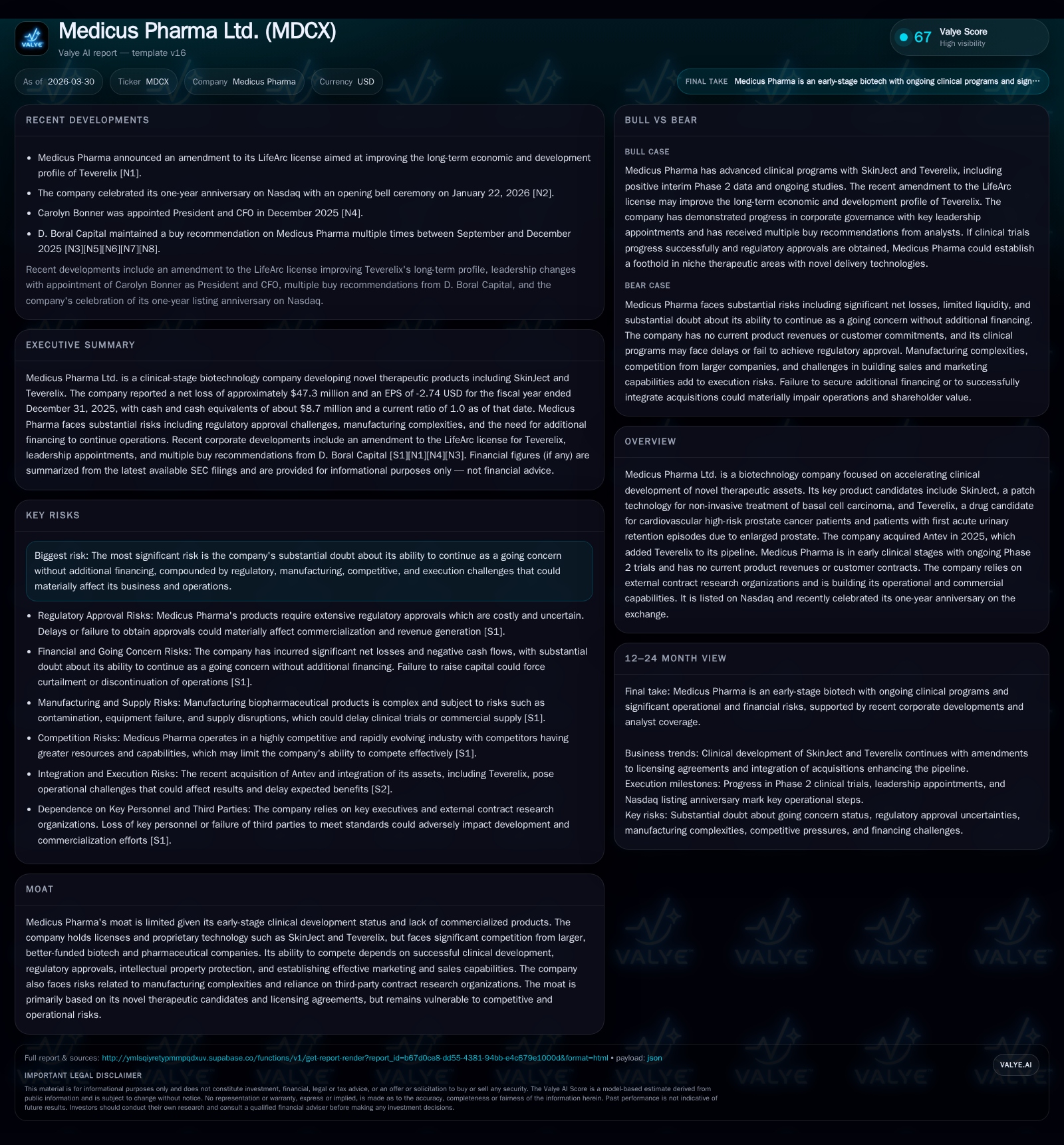

Medicus Pharma Ltd., a Nasdaq-listed biotechnology firm, remains in an early clinical phase with no current product revenues, focusing on advancing SkinJect and Teverelix through Phase 2 trials. The acquisition of Antev in 2025 expanded its pipeline but significantly increased operating losses and cash burn. Despite holding promising technology assets, the company faces substantial regulatory, integration, and commercial risks while managing its capital structure amid ongoing funding needs and uncertain profitability timelines.

Foundation of Innovation: Early Growth Drivers and Acquisition Integration

Medicus Pharma Ltd. operates as an early-stage biotechnology company focused on research and clinical development with no current revenues. In August 2025, Medicus acquired Antev, gaining the drug candidate Teverelix alongside its existing technology SkinJect [S2]. This acquisition expanded the company’s pipeline and increased its cost base.

Financially, operating income losses escalated sharply from approximately -$11.2 million in FY2024 to -$34.4 million in FY2025, representing a 207% year-over-year increase [F1]. This rise mainly reflects amplified spending on clinical trials, costs related to integrating Antev’s operations, and expanded R&D activities for both SkinJect — a transdermal patch targeting basal cell carcinoma — and Teverelix [S1][S2].

Management identifies significant integration challenges including aligning geographically dispersed teams, consolidating infrastructures, retaining key personnel, and harmonizing corporate cultures [S2]. These operational complexities increase execution risk during this critical growth phase.

Clinical Advancement: Progress on SkinJect and Teverelix Pipeline

SkinJect employs innovative transdermal patch technology aimed at non-invasive treatment of basal cell carcinoma. Early Phase 1 studies indicated favorable tolerability; however, progression into Phase 2 trials carries standard uncertainties related to efficacy, dosing, and safety [S1].

Teverelix is positioned for treating acute urinary retention episodes linked to benign prostatic hyperplasia and prostate cancer patients with cardiovascular risk factors. Following the Antev acquisition, Medicus initiated Phase 2b trials to validate therapeutic effects aligned with regulatory expectations [S1][S2]. Both candidates require approval from regulatory bodies such as the FDA—a process known for high attrition.

Market acceptance will depend not only on regulatory approval but also payer reimbursement decisions which can be variable for novel delivery systems like transdermal patches [S1].

Financial Strains Amid Scaling: Operating Performance and Cash Flow Analysis

Medicus exhibits characteristics typical of pre-revenue biotech firms investing heavily in clinical development. Net income declined from -$11.2 million in FY2024 to -$47.3 million in FY2025—a drop of approximately 324% year-over-year [F1]. Operating cash flow similarly deteriorated from -$10.2 million to -$22.8 million over the same period, reflecting accelerated cash burn due to late-stage trial expenses.

Liquidity remains constrained with cash & equivalents totaling $8.7 million as of December 31, 2025—sufficient only for near-term operational needs given current expenditure levels [F1]. The current ratio stands at approximately 1.0 (current assets roughly equal current liabilities), indicating tight working capital conditions that necessitate continued access to external financing imminently [F1].

The company’s auditor has expressed substantial doubt about Medicus’s ability to continue as a going concern without additional funding or revenue generation [S1].

Capital Allocation Dynamics: Funding Needs, Investor Considerations, and Return Metrics

Capital allocation is dominated by R&D expenditures with no dividends or share repurchases planned or issued—consistent with early-stage biotech norms [S1][F1]. Financing efforts have centered around equity sales under a Standby Equity Purchase Agreement (SEPA) executed in early 2025 with Yorkville Advisors providing committed purchasing capacity subject to drawdowns [S3].

Return metrics such as ROE are not informative at this stage due to negative retained earnings; net losses exceed shareholder equity resulting in distorted ratios that do not reflect performance returns [F1]. Investors are likely focused on efficient capital deployment toward milestone achievements validating asset potential while managing dilution risks inherent in repeated funding rounds.

Operational Risks and Regulatory Hurdles Facing Medicus Pharma

Medicus faces numerous operational risks detailed extensively in SEC filings:

- Clinical risk: Failure or delay in regulatory approval due to trial setbacks could materially impact value [S1,S4].

- Manufacturing complexity: Dependence on third-party contract research organizations raises supply chain and quality control risks [S5,S6].

- Regulatory compliance: Adherence to FDA requirements including post-approval monitoring imposes ongoing costs; violations could restrict commercialization .

- Intellectual property: Patent challenges or trade secret breaches may erode competitive advantages if unresolved unfavorably .

- Healthcare laws: Compliance with anti-kickback statutes, privacy regulations like GDPR/HIPAA across multiple jurisdictions adds legal complexity requiring vigilant controls .

- Product liability: Existing general liability insurance may be insufficient against large claims arising from late-stage clinical use or future marketed products .

Robust governance systems remain essential as Medicus scales operations.

Strategic Roadmap Ahead: Milestones to Monitor and Growth Prospects

While explicit forward-looking guidance is limited, investors should monitor:

- Completion and publication of Phase 2 data for SkinJect and Teverelix impacting regulatory filing timelines.

- Regulatory submissions across jurisdictions including U.S., Canada, Europe requiring strategic execution.

- Additional financing rounds likely given cash runway constraints relative to lengthy development cycles.

- Efforts toward operational scalability including potential direct sales capabilities or partnerships post-approval.

Growth prospects hinge on demonstrating therapeutic advantages relative to competing oncology and urology treatments plus payer acceptance influencing commercial scale.

Historical Operating & Financial Performance

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Net YoY |

|---|---|---|---|---|

| 2025 | -47 | -23 | -34 | -323.8% |

| 2024 | -11 | -10 | -11 |

Source: SEC companyfacts cache [F1]. Figures sourced from latest FY2025 end-of-year SEC filings reflecting intensifying loss profile consistent with ongoing clinical investment.

This review highlights Medicus Pharma’s challenging transition from early clinical research toward potential commercialization amid scientific uncertainty paired with pressing financial demands. Success will require disciplined execution of clinical milestones alongside securing necessary funding—a balance critical for emerging biotech firms at this stage.

Disclaimer: This report is based solely on publicly available filings as of March 30th, 2026. It does not constitute investment advice or recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments