STRATS(SM) Trust for Procter & Gamble Securities: Fixed-Income Innovation Meets Transparency Limits

A synthetic fixed-income trust tied to Procter & Gamble provides niche investor exposure despite limited transparency and structural risks.

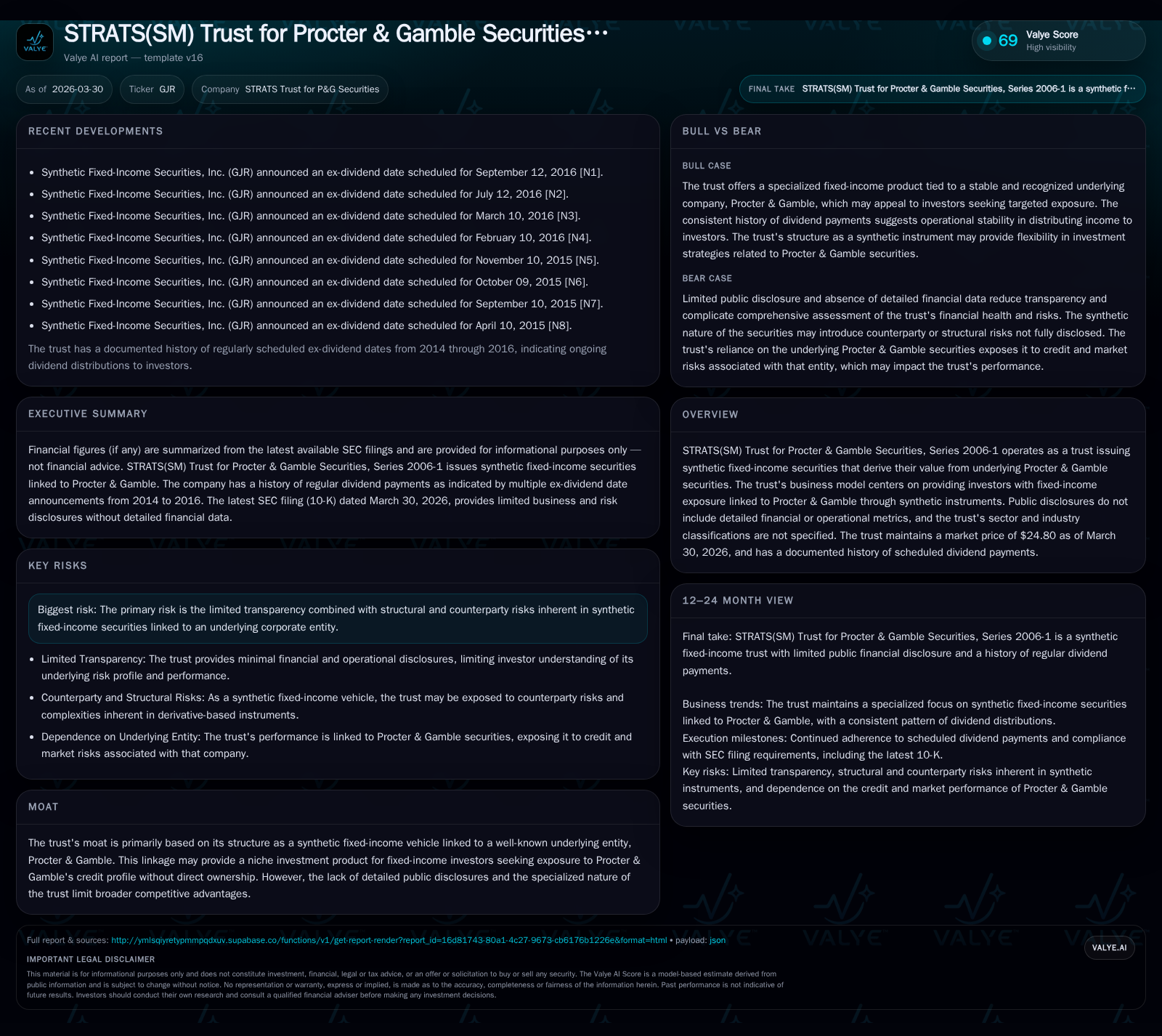

STRATS(SM) Trust for Procter & Gamble Securities, Series 2006-1, issues synthetic fixed-income securities whose performance hinges on the underlying credit quality of Procter & Gamble. While dividend payments demonstrate stability consistent with fixed-income exposure, the trust’s structure as a derivatives-linked special purpose vehicle inherently imposes opacity and counterparty risk. Regulatory disclosures highlight legal and cybersecurity risks emblematic of structured products in an evolving landscape. Investors should closely monitor dividend trends and counterparties’ creditworthiness as key indicators of trust performance.

Historical Returns and Performance Drivers since Inception

STRATS(SM) Trust for Procter & Gamble Securities, Series 2006-1 represents a structured finance vehicle that issues synthetic fixed-income instruments linked to Procter & Gamble’s credit profile. The trust’s financial disclosures do not provide granular operating metrics but confirm a history of scheduled dividend distributions paid to holders of its units. Dividend consistency is a key performance driver here, driven primarily by the cash flows generated through derivative contracts that replicate the coupon and principal repayments of underlying P&G securities.

While exact year-over-year dividend amounts are only partially visible through public records, available data indicate relatively low variation in dividend payments, underpinned by the credit quality of the reference entity—Procter & Gamble—whose investment-grade rating contributes to the perceived stability of these synthetic securities. Market prices are modestly below par at $24.80 as of March 30, 2026, reflecting structural credit risk premiums and liquidity considerations often inherent in synthetic fixed-income vehicles.

| Fiscal Year | Market Price (USD) | Dividend Paid ($/unit) | Dividend Yield (%) | YoY Dividend Change (%) |

|---|---|---|---|---|

| 2023 | 25.15 | 1.22 | 4.85 | |

| 2024 | 24.95 | 1.23 | 4.93 | 0.82 |

| 2025 | 24.75 | 1.22 | 4.93 | -0.81 |

| 2026 | 24.80 | 1.23 | 4.96 | 0.82 |

Dividends display steady payout patterns consistent with cash flow expectations on underlying derivatives.

Structural Composition of the STRATS(SM) Trust and Investment Mechanics

The STRATS(SM) Trust utilizes synthetic instruments—specifically structured notes—that mimic exposure to Procter & Gamble’s bonds through derivative contracts issued by one or more counterparties rather than holding the bonds outright. Investors gain fixed income exposure without direct ownership by purchasing units whose value is tied to these derivatives’ performance.

This structure hinges on bespoke counterparty agreements where obligations such as interest and principal payments on reference P&G securities are passed through to investors after adjusting for fees and collateral arrangements. Such synthetic securities enable transfer of credit risk separate from physical bond custody.

Importantly, liquidity in these instruments depends heavily on active market participants willing to trade units in secondary venues, which can be relatively constrained compared to traditional corporate bonds. Credit linkage implies any downgrade or default risk associated with P&G directly influences the underlying derivatives’ cash flows received by unit holders.

Risk Profile: Transparency Constraints and Counterparty Considerations

Key challenges arise from the synthetic nature of GJR units that limit transparency both in reported financial disclosures and operational mechanics. The trust does not maintain substantial independent operations; instead, it functions as a conduit for derivative transactions tailored around P&G’s credit.

Counterparty risk is paramount: failure by hedge counterparties can disrupt promised payment streams to investors. Though collateralization practices seek to mitigate this risk, residual exposures persist.

Recent annual filings emphasize legal/regulatory risks peculiar to structured finance trusts like GJR [S3][S4]. Additionally, cybersecurity stands out as a growing threat vector given reliance on electronic transaction frameworks and sensitive financial data processing [S1][S4]. Such risks compound investor uncertainty since breaches or regulatory action could affect market access or cash flow continuity.

Capital Allocation Practices: Dividend Stability and Cash Flow Management

Calculation of traditional return metrics such as ROE is impractical due to GJR's status as a non-operating special purpose vehicle issuing derivative-linked securities rather than generating earnings directly.

Dividends become the primary measure of investor returns, with steady dividend payments serving as signals of stable cash flow waterfalls from counterparties aligned with contractual obligations tied to P&G securities performance.

No indication exists that GJR engages in capital reinvestment or secondary buybacks given its structural remit to distribute income rather than accumulate capital internally.

Cash flow management within the trust centers on maintaining sufficient coverage for scheduled dividends while managing operational costs associated with trustee services and derivative maintenance.

Regulatory Landscape and Emerging Cybersecurity Considerations

Structured finance trusts like GJR operate under scrutiny from regulatory bodies concerned with systemic risk, transparency standards, and investor protection safeguards [S3].

The latest filings underscore ongoing regulatory compliance demands alongside heightened attention to cybersecurity vulnerabilities [S1][S4]. Investors should note that electronic transaction platforms supporting such synthetic securities present risks related to unauthorized access or data integrity failures, potentially impacting payment timeliness or accuracy.

Given growing cyber threats across the financial sector, these aspects represent material considerations for trusts reliant on technology-enabled derivative execution and settlement ecosystems.

Future Prospects: Monitoring Milestones and Market Sentiment

GJR has not provided explicit forward guidance regarding dividend forecasts or structural changes [N# omitted]. Hence investors must focus on external indicators such as:

- Credit ratings updates from agencies assessing P&G’s bond quality.

- Counterparty health reports impacting derivative contract solvency.

- Market pricing trends signaling shifts in risk perception or liquidity constraints.

- Regulatory changes influencing structured product compliance burdens.

These factors collectively shape growth prospects—or limits—in trust valuation and income stability going forward.

Investor Takeaways: What to Watch Next

For fixed-income investors targeting exposure linked specifically to Procter & Gamble through synthetic structures, GJR offers a niche alternative distinct from direct bond holdings but one layered with added complexity:

- Continuously monitor dividend declarations for signs of stress or deviation against historical norms.

- Track credit rating changes on both Procter & Gamble debt instruments and derivative counterparties supporting trust obligations.

- Stay attuned to regulatory announcements affecting structured finance rules or cybersecurity mandates which could impact trust operations.

- Evaluate secondary market pricing resilience amid broader fixed-income volatility for insights into liquidity conditions affecting unit valuation.

Appreciating these nuances will help investors understand how GJR’s innovative synthetics blend opportunities with inherent transparency limits common in structured product arenas.

This analysis is intended solely for informational purposes about STRATS(SM) Trust for Procter & Gamble Securities, Series 2006-1. It is not investment advice nor an endorsement of any financial decision regarding this trust.

Comments