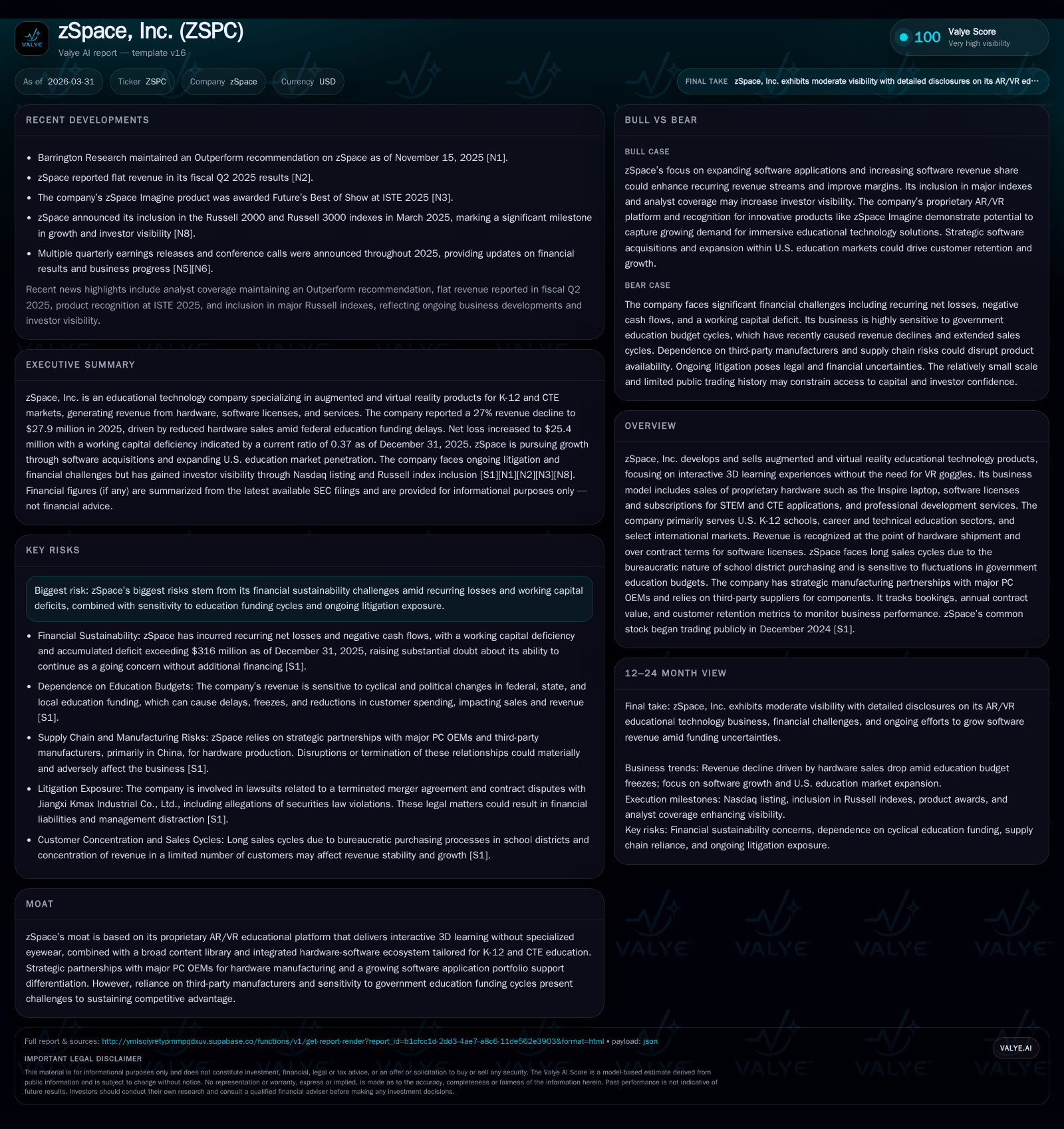

zSpace's Struggle to Scale: AR Education Hardware Meets Funding and Legal Hurdles

zSpace faces revenue contraction primarily driven by hardware sales decline, seeks software subscription growth amid capital strains and legal challenges.

Despite pioneering an augmented reality platform that delivers immersive STEM and CTE learning without VR goggles, zSpace, Inc. has encountered significant headwinds reflected in a steep revenue drop and persistent operating losses through 2025. Hardware sales have contracted sharply due to prolonged K-12 sales cycles and budget sensitivities, while software subscriptions show promise but have yet to offset these declines. The company's fragile liquidity position is compounded by substantial debt, ongoing litigation, and reliance on third-party manufacturing, all of which cloud near-term operational stability.

From Growth to Contraction: Revenue Dynamics and Product Mix Shifts

zSpace’s historical path illustrates a challenging transition marked by declining top-line figures amid evolving product mix pressures. For the fiscal year ended December 31, 2025, total revenues contracted substantially to $27.86 million from $38.10 million in 2024, a decrease of roughly 26.9% [F1]. This abrupt fall predominantly stems from hardware revenues shrinking from $21.99 million in 2024 to $14.21 million in 2025 — a near 35% decline [S5]. The flagship Inspire laptops, manufactured under strategic OEM partnerships predominantly located in China, represent the core hardware offering where volume moderation was notable.

The long sales cycles endemic to the U.S. K-12 public school segment, which consumes a large portion of zSpace’s product portfolio, exacerbate such declines. District purchasing often hinges on government budget allocations that remain susceptible to macroeconomic shifts—thereby injecting timing uncertainty into order flows. Unlike hardware that recognizes revenue upon shipment, software licenses generate ratable revenue over contract terms reflecting annual or multi-year licenses — complicating immediate revenue recognition and magnifying short-term top-line impacts when hardware demand wanes [S6].

Software revenues also declined year-over-year from $12.86 million to $10.56 million [S5], albeit with improved margin profiles given less dependency on third-party licensing costs [S13]. Services revenues — encompassing professional development offerings invoiced separately from hardware/software sales — remained stable but modest at around $3 million annually.

Historical performance (annual)

| FY |

|---|

| 2025 |

Source: SEC companyfacts cache [F1].

This contraction highlights the fragility inherent in a largely hardware-dependent business model servicing the cautious public education sector.

Software and Subscriptions: The Growth Engine or Pipe Dream?

zSpace has articulated a strategic pivot toward expanding its software subscription base — presenting it as an engine for sustained growth due to durable contract structures typical of user-based licensing models [S6]. Software applications license intellectual property enabling interactive STEM education and reside primarily within the proprietary Inspire ecosystem.

Revenue recognition for software occurs ratably over contractual periods as license keys activate access; this pattern differs materially from point-in-time recognition associated with hardware shipments [S6]. Subscriptions may vary between device-based models allowing unlimited users per device or user-count-limited contracts renewed annually or multi-year terms.

While gross margins on software reached approximately 71% in 2025 compared to hardware’s lower mid-thirties territory (34%) reflecting component costs and outsourced manufacturing expenses [S13], the raw decline in absolute software revenue hinders immediate offsetting impact against diminishing hardware sales.

Additionally, customer renewal rates bear critical influence on recurring software revenue growth: while management measures this metric internally as a gauge for penetration and adoption momentum [S16], explicit quantitative disclosure is absent making sustained growth speculative until more transparent guidance is provided.

Moreover, services revenue—and costs—increased modestly reflecting incremental warranty contracts and professional development engagements but represent only a fraction of total revenues limiting leverage impact [S13].

What to Watch: Upcoming Milestones and Market Signals

As of the latest disclosures ending March 31, 2026, zSpace provides limited explicit forward guidance beyond acknowledging material booking cancellations ('debooks') experienced post-2024 that impacted previous commitment levels [S16]. These cancellations — totaling $1.7 million in 2024 alone — mainly reflected customer fiscal constraints linked to pandemic-era budget tightening, underscoring continued exposure to education sector cyclicality.

Key operational indicators poised for scrutiny include:

- Changes in order backlog depth especially from core U.S.-based K-12 districts.

- Renewal rates for software subscriptions indicating adoption retention and potential expansion.

- International bookings proportion (~15%) as diversification beyond domestic markets could mitigate regional budget risk [S16].

- Any initiation or resolution of current litigation cases given their potential impact on corporate focus and partner confidence.

Without formal quantitative outlooks or detailed backlog disclosures currently available, these proxies will serve as early market signals influencing assessments around recovery prospects.

Capital Fitness: Navigating Liquidity, Debt, and Allocation Choices

Financially, zSpace confronts a precarious liquidity situation heading into fiscal year-end 2025 with combined cash and equivalents totaling approximately $1.02 million juxtaposed against current liabilities nearing $17.31 million—a current ratio of about 0.37 evidencing severe short-term coverage constraints [F1]. The company reported net cash used in operating activities of approximately $18 million for FY2025 versus nearly $8.9 million the prior year demonstrating worsening cash burn trends [S7][S25].

To sustain operations amid negative cash flows extending since inception, zSpace has raised liquidity primarily via debt instruments including convertible notes aggregating upwards of $41 million collectively through staged financings from institutional investors starting in early 2024 continuing through early 2026 [S7][S8][S20][S27]. Debt maturities have been amended with payment moratoriums through late calendar year 2026 deferring interest payments but compounding principal balances owed creating heavier future servicing obligations [S11][S20].

Equity issuances occurred during December 2024’s IPO raising net proceeds of roughly $7.5 million plus follow-on equity line draws contributing incremental funding infusions [S7][S25]. Despite capital raises no dividends or share repurchases have been declared or executed as management prioritizes conservation of cash towards operational liquidity maintenance [S15][S23].

Balance sheet leverage combined with tightening working capital cycles—driven by accounts receivable concentrations (notably one customer representing over 11% of receivables at end-2025) and inventory purchase obligations exceeding $10 million expected within one year—raise pronounced solvency risks unless operating performance stabilizes or additional financing is secured promptly [S5][S26].

Operational Challenges Behind Sales Cycles and Manufacturing Dependencies

The sales funnel into public schools is characteristically elongated requiring extensive tenure navigating bureaucratic procurement practices spanning several months to even years per district contract—frequently influenced by fiscal year government appropriations restricting discretionary technology spend windows. These intrinsic delays disrupt conventional demand forecasting models leaving the company vulnerable to timing gaps between shipment cycles impacting quarterly revenue consistency.

On the supply side, all Inspire laptops are manufactured under OEM agreements primarily based in China relying on third-party suppliers of components where industry-wide semiconductor shortages and commodity price swings have induced volatility in bill-of-materials costs affecting gross margins [S6][S10]. Freight logistics outsourcing has mitigated some cost elements but reduced direct distribution control introduces exposure during global disruptions such as those witnessed during COVID-19 pandemic periods further emphasizing supply chain fragility.

Maintaining product lifecycle economics for educational devices designed with specialized augmented reality capabilities intensifies operational overhead requiring continuous R&D investments alongside managing obsolete inventory write-downs historically amassing hundreds of thousands annually [S13], pressuring margin optimization efforts.

Legal Headwinds and Their Impact on Corporate Strategy

zSpace currently confronts multiple legal disputes creating material execution risks beyond mere financial burdening:

- A breach of contract suit filed February 9, 2026 by Jiangxi Kmax Industrial Co., Ltd alleges unpaid invoices totaling approximately $558K related to a Software Resale License Agreement dating back several years; zSpace has acknowledged a payable reserve of roughly $600K while asserting counterclaims including IP infringement defenses; responses pending as April deadlines approach [S1][S23].

- Subsequent securities law-related allegations surfaced March 11, 2026 from the same entity naming certain officers; claims reference investment disputes linked to pre-IPO private placements seeking rescission remedies and damages which zSpace contests vigorously in court proceedings scheduled for trial January 20, 2027 after termination of a prior merger deal with EdtechX SPAC partners also triggered litigation claims earlier [S1].

Such ongoing contentious matters divert senior leadership attention from commercial execution while potentially heightening reputational risks among OEM partners and institutional customers sensitive to governance issues.

Valye’s Take: Risks, Opportunities, and Strategic Imperatives

zSpace’s technological uniqueness anchored around AR educational delivery sans goggles — combined with a growing software portfolio curated specifically for STEM/CTE applications — underpin competitive positioning augmented by critical OEM manufacturing agreements ensuring product availability at scale.

However, financial sustainability concerns dominate the near-term narrative marked by steep top-line contraction fueled largely by adverse K-12 spending patterns and extended vendor payment obligations resulting in working capital deficits evidenced through sub-one current ratio metrics.[F1] Negative operating income exceeding $22 million alongside sizable net losses surpassing $25 million highlight profitability lagging fundamental support amid capital-intensive R&D plus selling/general/administrative cost structures rising moderately year-over-year.[F1][S14]

Successful scaling will hinge heavily on accelerating transition toward ratable software subscription revenues that deliver steadier top-line visibility alongside improved margin profiles mitigating inherent volatility embedded within episodic hardware shipments. Equally critical will be strengthening balance sheet resilience through proactive refinancing strategies potentially involving negotiated covenant modifications or fresh equity infusions mitigating looming repayment pressures post-interest moratorium expirations.

Investors monitoring zSpace should prioritize shipping velocity metrics aligned with contract renewals—a proxy for customer stickiness—alongside incremental clarity surrounding resolution pathways across active litigations constraining corporate focus. Furthermore, vigilance over international market penetration outcomes may offer diversified growth avenues somewhat less tethered to U.S.-centric public education funding challenges.

Navigating this complex matrix without overstating either imminent turnaround prospects nor default risk will require continual reassessment grounded strictly on disclosed operating trends without extrapolative projections.

This analysis is based solely on disclosed financial results, risk factors, operational commentary contained within SEC filings dated through March 31, 2026 consistent with publicly available information as cited.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments