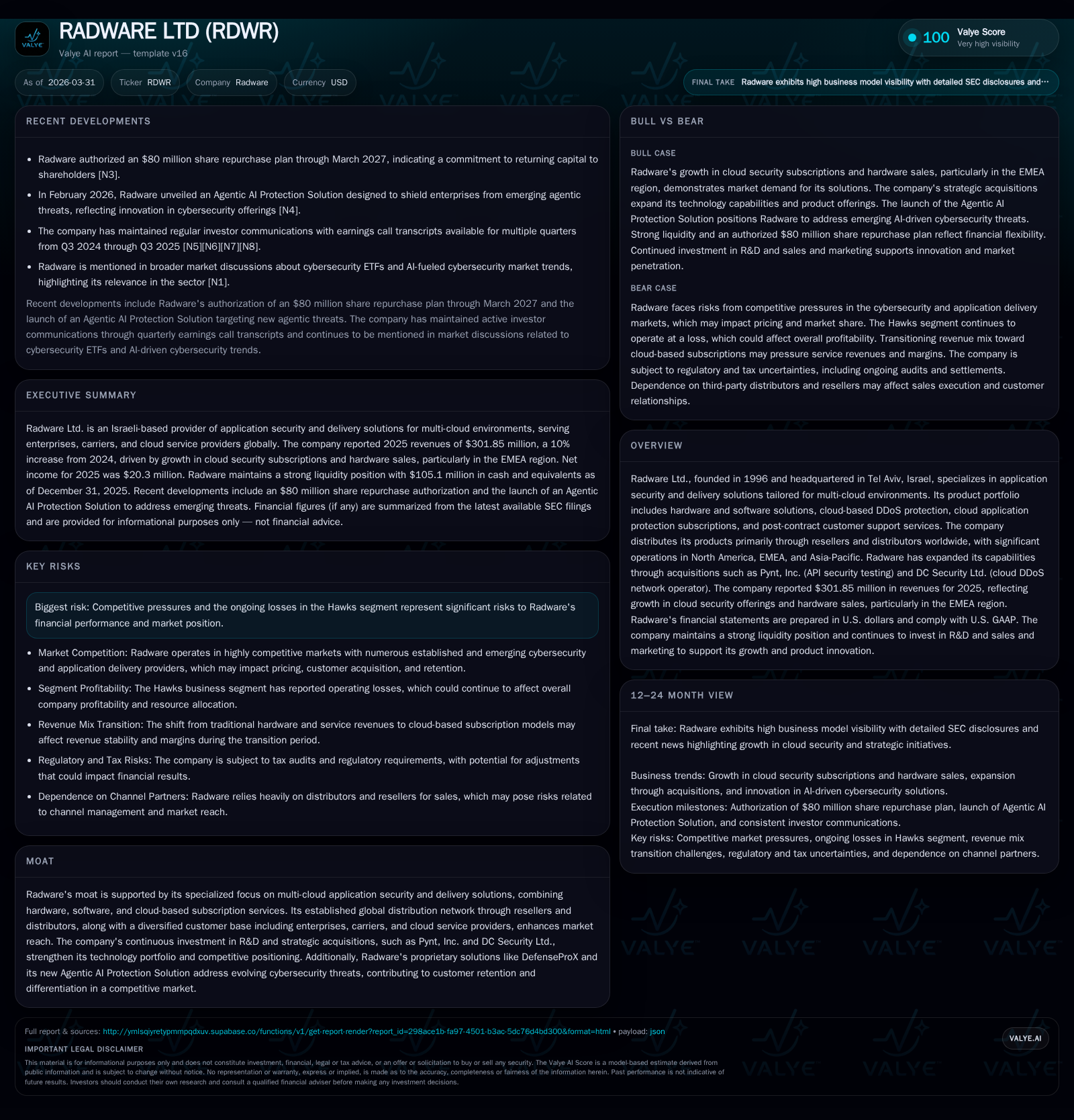

Radware Ltd: Rebounding Profitability and Strengthened Cloud Security Position

Radware's transition to operating profitability in 2025 is driven by growth in multi-cloud security offerings and strategic acquisitions, offsetting segments with ongoing losses.

Radware Ltd. has returned to operating profitability in 2025 after successive losses, leveraging a near 10% revenue increase underscored by its shifting product and subscription mix. Its global distribution network supports robust growth in North America and EMEA, assisted by key acquisitions like Pynt, Inc. for API security and DC Security Ltd. for cloud-based DDoS protection. While capital deployment remains balanced between R&D and shareholder returns, challenges persist due to losses in the Hawks segment and the competitive cybersecurity landscape.

Financial Recovery Signals Amid Revenue Growth and Operating Turnaround

After several years marked by negative operating results — notably a heavy $31.7 million loss in 2023 — Radware achieved a significant turnaround with an $11.4 million operating profit in fiscal year 2025 [F1]. This reversal correlates with incremental top-line growth: revenues increased almost 10% year-over-year to $301.85 million by end-2025, up from $274.88 million in 2024 [F1]. Net income similarly swung from a prior loss to positive territory at $20.26 million last year.

This rebound reflects improved gross margins supported primarily by an expanding share of product revenues relative to services — product gross margin enhancements suggest effective operating leverage as scale improves [S1][S4]. Notably, the cost of products as a percentage of product revenue declined from 27.1% in 2024 to approximately 25.9% in 2025 before amortization adjustments [S14]. Operating expenses moderately increased by around 3%, yet this was enough below revenue growth to drive margin expansion [S8].

Operating cash flow showed a contraction versus the prior year decline (30% decline YoY), dipping from $71.6 million to about $50.1 million [F1]. However, substantial reduction in capital expenditures resulted in sustained strong free cash flow generation ($41.5 million), supporting ongoing investments without pressuring liquidity [F1][S21].

Historical performance (annual)

| FY | Rev ($mm) | Net ($mm) | CFO ($mm) | OpInc ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 302 | 20 | 50 | 11 | +9.8% | +235.5% |

| 2024 | 275 | 6 | 72 | -4 | +5.2% | +128.0% |

| 2023 | 261 | -22 | -3 | -32 | -11.0% | -12906.0% |

| 2022 | 293 | 0 | 32 | -3 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Buybacks ($mm) | FCF ($mm) | ROE% |

|---|---|---|---|

| 2025 | 10 | 42 | 5.8 |

| 2024 | 1 | 66 | 1.9 |

| 2023 | 63 | -9 | -7.6 |

| 2022 | 59 | 23 | -0.0 |

Source: SEC companyfacts cache [F1].

*n.m.: Not meaningful due to change from negative to positive values.

Product and Service Mix Evolution Driving Revenue Expansion

Products combined with cloud subscription revenues made up roughly two-thirds (63%) of total sales last fiscal year — up sharply from an already growing base of around 57% in the previous year [S4][S18]. This mix tilt reflects customer preference for bundled offerings blending physical hardware, software licenses, and increasingly critical cloud-delivered subscription services.

Radware applies ASC606 compliant accounting principles whereby physical goods’ revenues are recognized at point of shipment or delivery when control transfers; subscription revenues are recognized ratably over contract periods consonant with SaaS norms [S4][S6]. Post-contract customer support (PCS)—covering technical help desks and unit repair or replacement—also benefits from ratable revenue recognition enhancing revenue visibility over one-to-three-year periods.

This recurring revenue model through subscriptions and PCS promotes predictable cash flow streams less volatile than traditional license sales alone [S4]. Moreover, increased focus on cloud security subscriptions solidifies customer retention via ongoing contractual commitments.

The shift towards such ratable revenue mechanisms embodies industry trends towards 'as-a-service' models that mitigate billing cyclicality while enhancing lifetime value metrics—a sector nuance Radware appears successfully adapting into its core business.

Regional Dynamics Fueling Growth: Spotlight on EMEA and Americas Markets

Geographically, Radware’s diversified footprint demonstrated resilience during fiscal year ended December 31, 2025 [S3][S18]. Revenues from North America—including notably the United States—grew by about +6% year-over-year to roughly $124.53 million (41% of total revenue), while EMEA surged +18% to approximately $111.25 million (37% share) [S3]. Asia-Pacific contributed steadily at about $66 million with a +5% increase.

This growth pattern underscores effectiveness of Radware’s channel sales strategy that leverages its global reseller-distributor network for widespread market penetration [S6]. The U.S market alone accounted for nearly one-third (31%) of overall sales while retaining consistent importance across reporting years.

Among growth drivers were expanding demand for cloud security subscriptions paired with steady hardware product uptake—particularly within DDoS protection devices underpinned by specialist scrubbing centers—highlighting regional pricing power variations based on infrastructure maturity levels [S18].

Such regional insights suggest differentiated market dynamics favorable to Radware’s multi-pronged delivery platform integrating physical devices with scalable cloud defenses.

Innovations and Acquisitions Strengthening Cloud Security Portfolio

Radware’s recent acquisition activity reflects deliberate capacity-building aligned with evolving enterprise cybersecurity needs [S1][N1][S2]. In January 2026, it acquired Pynt, Inc., an API security testing firm whose capabilities complement Radware’s cloud application protection suites through proactive vulnerability identification—a burgeoning priority given growing API exploitation risks.

Meanwhile, the February 2022 acquisition of DC Security Ltd., formerly named SecurityDAM Ltd., integrated vertically by internalizing cloud DDoS scrubbing center operations previously outsourced via related-party contracts [S1][S23]. These data centers cleanse traffic before reaching clients’ networks thus essential for robust denial-of-service mitigation.

Complemented by proprietary products like DefenseProX—which provides real-time adaptive mitigation—and the newly launched Agentic AI Protection Solution incorporating artificial intelligence threat heuristics, Radware crafts a comprehensive multi-cloud security fabric resistant to contemporary attack vectors.

These integrations not only broaden functional scope but also enhance cross-product synergies enabling streamlined deployment across hybrid environments—a decisive advantage amid intensifying cyber threats demanding automated defensive architectures frequently referenced as 'scrubbing center services' within sector parlance.

Challenges from Hawks Segment and Competitive Market Pressures

Despite broad progress within its core business segment, Radware acknowledges continuing losses emanating from its Hawks segment—a smaller operative unit likely tied to experimental or niche product lines [F1][S17][S25]. Operating losses shrank slightly but persisted into recent years underscoring an area where operational discipline or strategic pivoting may be required.

Competitive headwinds remain acute as numerous cybersecurity vendors jockey for platform dominance amidst technological convergence and price pressures exacerbated by commoditization trends in basic DDoS defenses and firewall functionalities.

Although no explicit remedial measures were disclosed beyond ongoing expense optimization efforts observed from changes in share-based compensation and personnel cost dynamics [S9][S20], balancing innovation investments against Hawks’ financial drag will be critical.

The segment profitability challenge illustrates the broader market pressure scenario requiring focused execution amid rapid technological evolution alongside macroeconomic uncertainty affecting IT budgets worldwide.

Capital Deployment Review: R&D Investment, Buybacks, and Cash Flow Health

Capital allocation policies emphasize continued innovation while maintaining shareholder value initiatives [F1][S21][S5][S6]. Research & Development spending edged upward to nearly $79 million in fiscal year 2025—a modest increase reflecting expanded headcount costs partly offsetting lower share-based comp grants [S7][S9]. This dedication affirms commitment to evolving proprietary technological moats essential for differentiation.

Capital expenditures surged circa +61.7% year-over-year to approximately $8.54 million as investments targeted infrastructure upgrades aligned with new cloud service expansions [F1]. Concurrently, Radware advanced buyback programs significantly netting $10.49 million spent during fiscal 2025 compared with under $1 million the prior year signaling confidence bolstered by improved free cash flows estimated around $41.55 million after subtracting capex from operating cash flow [F1].

With liquidity buffers sustained at over $105 million in cash equivalents plus favorable current ratios near ~1.63 supported by current assets exceeding liabilities comfortably allowed operational flexibility without external financing reliance [F1][S15].

Return on equity reached roughly a mid-single digit ~5.8%, indicative of emerging earnings traction though reflecting room for optimization relative to peer cybersecurity firms known for high reinvestment cycles balanced with shareholder returns [F1].

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments