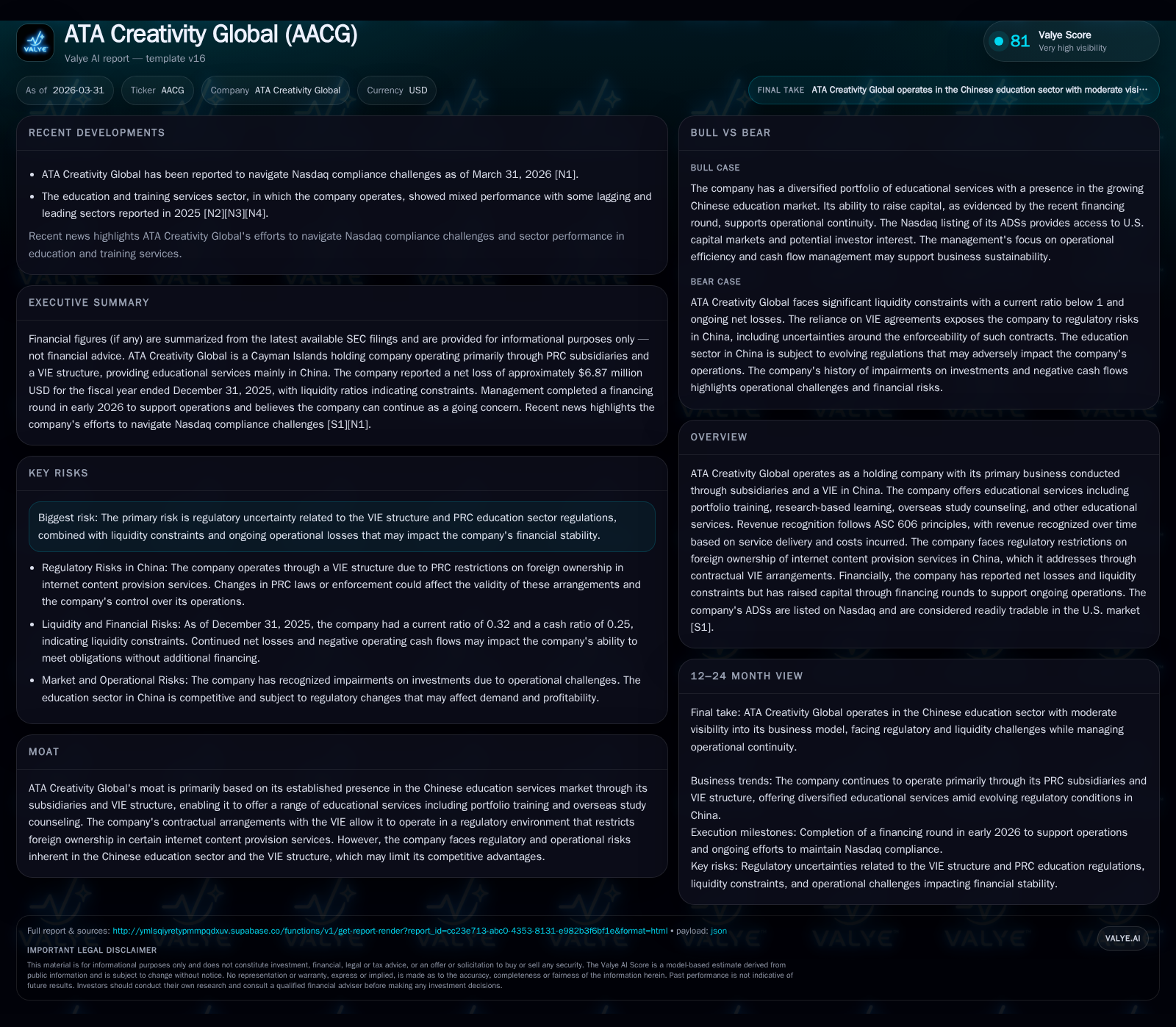

ATA Creativity Global’s Financial Struggles and Strategic Streamlining in China’s Education Market

A close examination of ATA Creativity Global reveals tensions between financial losses, regulatory challenges, and strategic refocusing in China’s creative arts education sector.

ATA Creativity Global (AACG) has encountered escalating net losses alongside modest revenue growth, largely driven by its portfolio training services in the Chinese art education market. Its reliance on a VIE structure introduces regulatory vulnerabilities amid evolving PRC education policies and foreign ownership restrictions. The company strategically exited its junior art education segment in late 2024 to concentrate on higher-margin international art education services. Liquidity remains strained, despite a recent $8.85 million financing round in early 2026, as operating cash flows have deteriorated sharply. Shareholder returns remain elusive due to persistent deficits and limited capital allocation options given regulatory constraints.

Historical Revenue and Operating Performance Trends

ATA Creativity Global's revenue showed restrained expansion from RMB268.1 million (~$38.3M) reported in both fiscal years 2024 and 2025, marking a ~16.4% year-over-year increase versus prior years measured against USD metrics from [F1]. Despite this top-line stability and mild growth, profitability deteriorated markedly: operating income plummeted from a loss of approximately $5.9 million in 2024 to nearly $9.2 million deficit in 2025—an over 55% worsening yearly decline; net losses escalated similarly from about $4.9 million to $6.9 million in the same interval [F1][S1]. Such trends underline sustained operational challenges compounded by tightening margins.

Operating cash flow suffered a pronounced reversal with a negative $2.3 million recorded for 2025 compared to smaller outflows or positive inflows previously; simultaneously, capital expenditures shrank dramatically by over 90%, reflecting curtailed reinvestment ability amid financial pressures [F1][S9]. These adverse trends emphasize liquidity stresses critical to sustaining ongoing activities.

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|---|

| 2025 | -7 | -2 | -9 | 0 | -38.9% |

| 2024 | -5 | 0 | -6 | 3 | -4.3% |

| 2023 | -5 | 1 | -6 | 0 | +31.7% |

| 2022 | -7 | -2 | -8 | 0 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2025 | -2 | -149.9 |

| 2024 | -3 | -45.3 |

| 2023 | 1 | -29.8 |

| 2022 | -2 | -33.5 |

Source: SEC companyfacts cache [F1].

Financial data extracted from AACG consolidated statements per [F1], capturing continuing operations.

Primary Revenue Drivers: Portfolio Training and Education Services

AACG segments its revenue primarily into portfolio training services, research-based learning services, overseas study counseling services, and other educational formats [S1]. Of these, portfolio training dominates (>70%), generating fees mainly through time-based or project-based credit hour programs targeting high school and undergraduate students preparing creative portfolios requisite for overseas art study admission [S1]. Pricing clarity derives from enrolled credit hours or projects completed under ASC 606 revenue recognition principles.

Following the October 2024 disposition of the more commoditized junior art education segment—which was lower margin—the company narrowed focus on international arts-related educational offerings with stronger brand recognition and presumably superior unit economics. This realignment was motivated by the need to stabilize margins while navigating complex market conditions exacerbated by regulation and capital limitations [S1]. Overseas study counseling and research-based learning services contributed smaller but gradually increasing proportions of overall revenue mix through increased student uptake.

Regulatory Environment and Structural Risks in China

AACG’s operations are conducted via subsidiaries and a variable interest entity (VIE) structure domiciled in China due to PRC government restrictions forbidding foreign ownership in internet content provision services critical to its business model [S1]. Such arrangements create operational complexity as they depend heavily on contractual agreements whose enforceability is inherently uncertain under evolving PRC laws.

Intercompany licensing fees transferred from VIE entities to the offshore holding company are subject to PRC VAT obligations along with business taxes that elevate effective cost bases and generate tax liabilities directly impacting profitability [S1][S4][S5]. Additionally, foreign exchange controls limit repatriation of cash held inside mainland China leading to further cash flow management constraints [S6]. Risk disclosures caution that any shifts undermining VIE contractual validity could jeopardize control over key subsidiaries or their earnings.

Recent Strategic Shift: Divestiture of Junior Art Education Business

The disposal of all junior art education businesses in late 2024 represents a decisive pivot amidst intensifying regulatory pressure targeting China’s after-school tutoring sector. This business unit historically operated under the "other educational services" category but faced margin compression relative to AACG’s core portfolio training offerings focused on higher-value international art educational pathways [S1].

This strategic pruning reflects an effort to consolidate operational resources toward segments offering clearer competitive moats via brand strength and differentiated service content amid tighter government scrutiny on foreign influence in education provision.

Liquidity Status and Capital Raising Efforts

Liquidity indicators paint a constrained picture; at December 31, 2025 AACG reported cash & equivalents totaling approximately $12.19 million against current liabilities exceeding $49 million leading to a current ratio of just ~0.32—signaling potential short-term liquidity stress points [F1][S6]. Negative cash flows from operations at about $2.3 million during fiscal year-end add urgency.

To counterbalance liquidity deficits stemming from prolonged operational losses and cash burn, AACG completed an $8.85 million registered direct offering placement in January 2026 aimed at bolstering working capital allowing continuity while executing cost rationalization initiatives across sales/marketing and administrative functions targeting elimination of redundancies [S4].

Management affirms its expectation of adequate resource availability for foreseeable future operations contingent upon successful execution of business plans alongside potential additional financings if necessary—denoting fragile but viable financial footing reflecting "going concern" judgments [S4].

Profitability Challenges: Operating Losses and Cash Flow Dynamics

Persistent operating losses exceeding $9 million in FY25 underscore fundamental profitability challenges exacerbated by pricing pressures amid increased competition within creative arts international education segments [F1][S7]. Cost drivers include teaching payrolls with performance-linked bonuses, rental expenses for classroom infrastructure and technology development expenditures though CapEx was very limited recently indicating tight reinvestment constraints.

Declining gross margins largely reflect varying unit economics influenced by credit hour volumes delivered under portfolio training plus costs related to ancillary research-based services affecting overall cost absorption. Operating expense controls remain crucial as share-based compensations contribute substantially to general & administrative expenses constraining earnings further [S7].

Capital Allocation and Shareholder Returns Overview

No dividends or share repurchase programs have been declared or executed since at least calendar years ending prior to FY25 per SEC filings confirming capital retention within the business necessary for working capital amidst losses rather than shareholder distributions [F1][S8][S11].

AACG's return on equity stood near -150% reflecting negative earnings versus reduced book equity base wiping out investor value generation prospects under current loss-making trajectory [F1]. PRC statutory reserve mandates require allocations from after-tax profits restricting available distributable earnings thereby adding layers of complexity on external dividend payments even if profits eventually emerge.

Outlook: Opportunities and Constraints Ahead

Looking forward demands balancing rising tuition demand fueled by China's expanding middle class increasingly seeking specialized international arts education pathways against tightening national policy frameworks restricting foreign-controlled entities via VIE constructs which introduce structural risks potentially impacting scalability [N1][S1][S2].

Growth levers reside largely in expanding portfolio training volumes aligned with premium curriculum offerings endorsed by overseas institutions enhancing market positioning plus exploiting hybrid delivery modes integrating online/in-person programs fostering cost efficiency gains.

However caution persists as geopolitical frictions between US-China combined with evolving educational regulations could impose unexpected hurdles requiring adaptability from corporate governance through operational contingencies.

Key Indicators for Investors to Monitor

Investors should observe quarterly updates on liquidity including cash balances against current liabilities revealing runway under ongoing losses; regulatory clarifications or legal precedents surrounding VIE contract enforceability shaping control confidence; shifts in revenue composition signaling sustained growth pockets beyond legacy juniors segment; marketing spend efficiency metrics determining customer acquisition economics; alongside progress on Nasdaq compliance following notices highlighting governance standards linked directly to valuation perceptions among US investor community [N1][S3][S9].

This analysis compiles publicly filed financial results combined with detailed MD&A disclosures providing a factual assessment without making investment recommendations or forecasts beyond documented evidence as stipulated under compliance guidelines.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments