MIND CTI LTD's Multi-Module Billing Platform: Balancing Growth and Competition

Analysis of MIND CTI’s financial trajectory, technology strengths, and market positioning amid competitive pressures in telecom software.

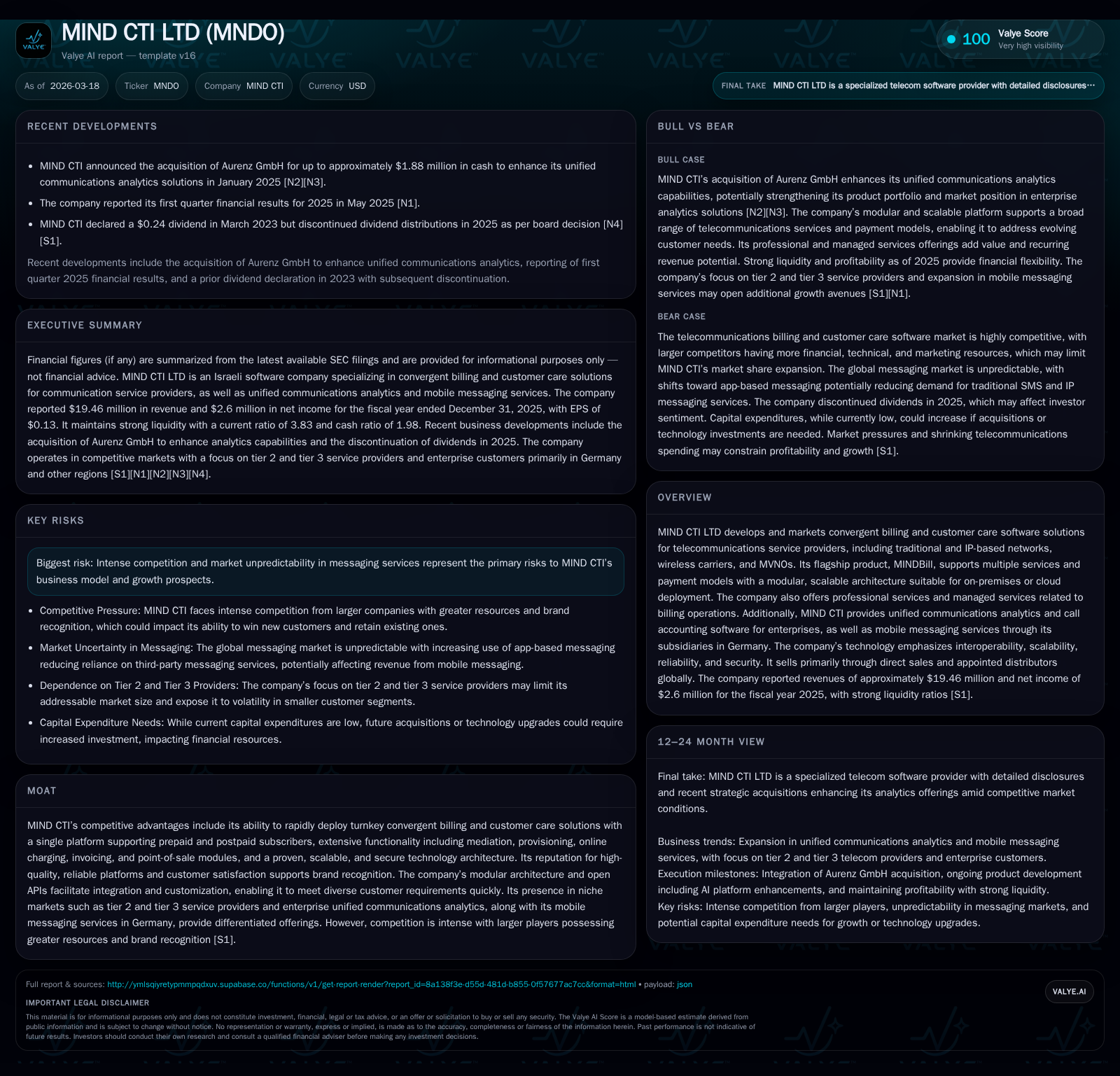

MIND CTI LTD operates as a specialized provider of convergent billing and customer care software tailored for tier 2 and tier 3 telecommunications operators globally. The company’s flagship MINDBill platform, supported by modular architecture and open APIs, enables integration with diverse telecom networks and supports prepaid/postpaid subscriber management. Financially, MNDO experienced a revenue decline of approximately 9.3% in 2025 accompanied by a sharper contraction in earnings, signaling margin pressure despite stable operating cash flow. Growth opportunities hinge on expanding service offerings, including mobile messaging and AI-driven tools, while competition from larger rivals and market volatility pose key risks. The company has discontinued dividends but maintains robust liquidity and operational cash generation.

Foundation of Growth: Historical Revenue and Profit Dynamics

MIND CTI LTD’s financial performance over the recent four fiscal years reflects underlying challenges in maintaining growth momentum amid a competitive telecom software landscape. According to the latest filings [F1], annual revenues fell from about $21.45 million in 2024 to $19.46 million in 2025, marking a notable -9.3% decline year-over-year. Meanwhile, operating income contracted more sharply by approximately 52.3%, declining from $4.38 million to just over $2.09 million in the same period.

Net income followed a similar pattern with a -43.8% drop to $2.60 million in FY2025 compared to FY2024's $4.63 million result. Despite this substantial earnings compression, the company maintained relatively steady operating cash flow generation around $3.99 million, mildly down (-3.1%) versus prior year.

Capital expenditures remained minimal at $27 thousand for the year but showed an increase relative to prior periods, primarily directed towards upgrades of hosted messaging platforms and essential equipment for engineering teams as disclosed [S16].

Historical performance (annual)

| FY | Rev ($mm) | Net ($mm) | CFO ($mm) | OpInc ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 19 | 3 | 4 | 2 | -9.3% | -43.8% |

| 2024 | 21 | 5 | 4 | 4 | -0.8% | -10.4% |

| 2023 | 22 | 5 | 4 | 5 | +0.3% | -2.3% |

| 2022 | 22 | 5 | 5 | 6 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($mm) | FCF ($mm) | ROE% |

|---|---|---|---|

| 2025 | 5 | 4 | 11.3 |

| 2024 | 5 | 4 | 19.1 |

| 2023 | 5 | 4 | 21.1 |

| 2022 | 5 | 4 | 22.2 |

Source: SEC companyfacts cache [F1].

This data illustrates that while the top line remained relatively flat between FY22-24 before declining notably in FY25, profitability indicators weakened considerably starting in FY24—pointing to margin pressures potentially linked to competitive pricing or increased operating costs.

Technology Edge: Scalable, Modular Architecture with Open APIs

MNDO’s technology stack centers on an open architecture designed around industry-standard APIs facilitating extensive interoperability with legacy telecom equipment as well as modern network infrastructures [S3]. Its MINDBill platform is purpose-built as a multi-layered object-oriented system supporting real-time distributed processing conducive to scalability, high availability, and security.

Key features include:

- Mediation capabilities for real-time event collection from voice, data, content services.

- Flexible online charging systems (OCS) enabling complex tariff plans sensitive to usage patterns such as time-of-day or call origin/destination.

- Integrated Point-of-Sale (POS) functionality extending billing into retail store environments with support for credit card processing and external tax engines.

- Workflow automation infrastructure allowing operators to customize business processes such as subscriber onboarding, order management, collections, and trouble ticket handling with speed.

The product supports multiple payment models—prepaid, postpaid, pay-in-advance—and offers multi-currency and multi-service billing consolidations within a single convergent platform [S12][S14]. Such architecture facilitates carrier-grade reliability critical in mission-critical applications involving high transaction volumes.

MNDO complements these core products with cloud-based messaging platforms operated via their German subsidiaries targeting enterprise customers needing API-driven mobile messaging integrations for CRM or marketing automation purposes [S3].

Market Focus: Serving Tier 2 and Tier 3 Providers Plus Enterprise Messaging

MIND CTI distinctly targets niche telecom sectors—specifically tier 2 and tier 3 service providers such as Mobile Virtual Network Operators (MVNOs), Wireless Internet Service Providers (WISPs), LTE/5G carriers who require adaptable billing systems without the complexity or cost structure imposed by large vendors [S6].

Their customer portfolio spans globally across traditional telcos evolving into quad-play operators (e.g., Moldtelecom), triple-play internet providers (e.g., Hrvatski Telekom), cable firms incorporating voice (EastLink), plus MVNEs like Pelephone Communications Ltd [S7]. This diversified footprint grants MNDO exposure across geographies: Europe (59%), Americas (34%), Asia Pacific & Africa (~2%) [S7].

On the enterprise side, the phonoEX ONE call accounting system aids multinational corporations by providing comprehensive telecom expense management coupled with quality of service monitoring tools tailored for multi-site global operations [S10][S18].

The acquisition of Message Mobile GmbH has established a foothold in the German messaging market serving over 100 enterprises with direct communication solutions ranging from OTPs to marketing SMS while also supporting wholesale message termination services negotiated via volume contracts—however this segment remains volatile due to app-based alternatives reducing SMS reliance [S11][S8].

Competitive Terrain: Strengths, Rival Resources, and Pricing Pressures

Competition within convergent billing software is intense with MNDO facing large multinational firms possessing substantially greater financial muscle and brand recognition combined with more extensive marketing capabilities [S4]. Furthermore, some competitors operate on leaner cost bases enabling aggressive pricing tactics that challenge MNDO’s market share.

However, MIND CTI leverages several distinct strengths:

- Rapid turnkey deployment capability allowing clients prompt go-live versus longer lead times typical elsewhere.

- Single unified database supporting both prepaid/postpaid subscribers minimizing backend complexity.

- Modular product design facilitating easy customization adapting swiftly to unique operator requirements.

- Proven technology base refined over years trusted by numerous operators worldwide.

These afford MNDO positioning as an agile alternative focused on specialized mid-tier operators reluctant or unable to migrate to heavyweight vendor suites immediately but seeking robust feature sets including mediation, provisioning, interconnect billing provisions and roaming management modules embedded within MINDBill [S4][S9].

On messaging fronts in Germany, competition involves international players like Sinch AB alongside numerous smaller local providers where MNDO competes mainly through tailored services combined with technological flexibility rather than broad-scale commoditized offerings [S8].

Future Growth Drivers: Expanding Services and Self-Onboarding Capabilities

Future expansion vectors include broadening the range of technological delivery models along with increasing new customer acquisition velocity by enabling self-registration processes facilitated through recently introduced e-commerce portals and mobile app-based self-care interfaces embedded into their billing system ecosystem [S3][S10].

Additionally, ongoing investment in artificial intelligence is evident through development of chatbots capable of responding autonomously to customer inquiries related to account status or assisting CSRs thus enhancing operational efficiency while enriching customer service quality [S10].

Though no formal management forecasts or revenue guidance are provided publicly [N2][S2], these initiatives hint at strategic emphasis on digitization trends catering both to existing client upsells as well as new operator onboarding optimized for scale without commensurate increases in headcount.

Financial Forecast Perspective: Monitoring Revenue, Profitability, and Efficiency Signals

Given absent explicit forward-looking guidance from management within recent disclosures [N2][S2], monitoring should prioritize:

- Revenue trend reversals signaling demand stabilization or recovery after recent contractions;

- Operating income margins revealing expense management effectiveness amid rising competitive intensity;

- Operating cash flow trends offering insight into quality of earnings relative to accrual accounting fluctuations;

- Capital expenditure patterns potentially indicating readiness for technological upgrades or acquisition moves.

Investors may also watch gross profit contributions from emerging product verticals such as mobile messaging services whose unpredictable nature can exert disproportionate effects on overall profitability dynamics.

Capital Deployment Review: Dividend Cessation, Cashflows, and Shareholder Returns

Historically MNDO paid dividends corresponding approximately to EBITDA plus financial income less income taxes following a board-approved policy until fiscal year-end 2025 when distributions ceased per board decision despite continued positive cash flows [F1][S15]. Specifically dividend payouts dropped from roughly $4.87 million in FY2024 to $4.50 million in FY2025 reflecting strategic capital preservation perhaps aimed at bolstering liquidity buffers or reinvestment flexibility.[F1]

With robust operational cash flow around $4 million annually exceeding minimal capex spending (~$27K in FY25), free cash flow availability remains healthy at near $4 million levels providing scope for selective investments or debt servicing if applicable.[F1]

Equity stood at approximately $23 million at year-end FY25 complemented by a strong current ratio approaching 3.83x denoting solid working capital adequacy underpinning operational resilience.[F1]

Approximate ROE based on net income over equity was about 11.3% suggesting efficient albeit declining return generation under current market conditions.[F1]

Risk Assessment: Cybersecurity Vigilance and Market Volatility Challenges

Given the mission-critical nature of billing software handling sensitive customer data along with cloud-based service components particularly within messaging services susceptible to heightened attack surfaces, MNDO maintains layered cybersecurity governance frameworks overseen by its audit committee comprising independent directors tasked explicitly with monitoring IT risk profiles including business continuity safeguards [S1][S23].

The company's VP of IT is seasoned with over nearly three decades at MNDO managing privacy programs complemented by company-wide employee awareness initiatives including phishing simulations designed to preempt social engineering vulnerabilities.[S23]

While no material cybersecurity incidents have occurred so far per disclosures up through FY25 year-end reporting periods [S24], emerging threats leveraging artificial intelligence represent continuous challenges requiring sustained vigilance given potential impacts on service availability or data integrity threatened by sophisticated exploits.

Market-wise messaging segments face unpredictability due to shifts toward app-based communications reducing traditional SMS volumes placing pressure on wholesale margins while intensifying competitive battles among aggregators further pressuring pricing structures challenging sustained growth without technological innovation or client retention enhancements.

This analysis synthesizes information available through official SEC filings as well as internal company disclosures without offering investment advice or forecasts beyond reported data points.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments