Netcapital Inc. Faces Steep Revenue Declines and Liquidity Pressures in Transitioning Financial Services

Netcapital’s sharp revenue drop, regulatory scrutiny, and customer concentration threaten growth as it pivots to broker-dealer services and blockchain technology.

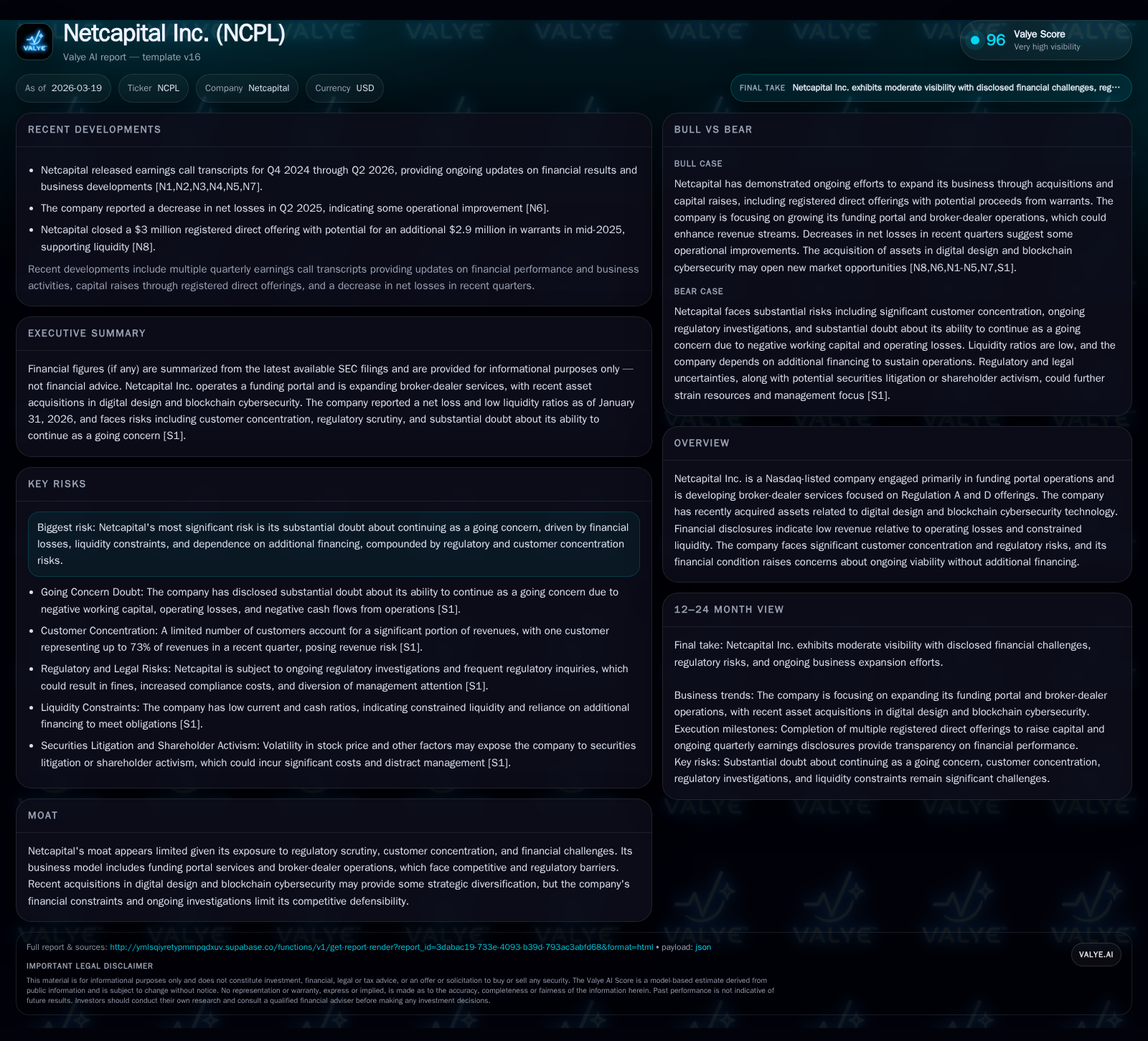

Netcapital Inc. has experienced a pronounced collapse in revenue over the past two years, driven by shifts in its funding portal business and intensifying regulatory costs. Operating losses have deepened significantly, while liquidity constraints and doubtful going concern status spotlight the firm’s financial fragility. The company is attempting a strategic pivot towards broker-dealer services targeting Regulation A and D offerings alongside acquisitions in blockchain cybersecurity, yet faces concentrated client risk and ongoing SEC investigations. Critical upcoming regulatory milestones and liquidity improvements will determine whether this transition stabilizes or further pressures capital preservation.

Collapse in Revenue: Historical Trajectory and Key Drivers

Netcapital's financials have deteriorated sharply over recent fiscal years as its traditional funding portal operations have faced significant headwinds. Revenue fell precipitously from $8.5 million at fiscal year ending April 30, 2023 (FY2023) to just $869 thousand by FY2025, reflecting an 82.4% decline [F1]. This collapse aligns with structural shifts within the niche market of Regulation A & D offering funding portals where increased competition and rising regulatory costs have squeezed margins.

Operating income paints an equally stark picture: the company moved from a positive operating income of $2.27 million in FY2023 to a deeply negative figure of -$8.32 million in FY2025, suggesting escalating operating costs not matched by sales growth or new revenue streams [F1]. The widening gap underscores both higher compliance burdens intrinsic to SEC-regulated portals plus internal challenges managing costs effectively.

Compounding these issues, Netcapital swung from recorded net profits of over $3 million in FY2022–23 to a cumulative net loss exceeding $28 million in FY2025 alone — a near tenfold deterioration signaling intensified write-downs or extraordinary expenses alongside operational losses [F1]. The operating cash flow remained consistently negative across the period, peaking at -$5.3 million in FY2025 which indicates persistent cash burn despite strategic pivots [F1].

Historical performance (annual)

| FY | Rev ($mm) | Net ($mm) | CFO ($mm) | OpInc ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 1 | -28 | -5 | -8 | -82.4% | -985.7% |

| 2024 | 5 | -3 | -5 | -3 | -41.7% | -188.2% |

| 2023 | 8 | 3 | -5 | 2 | +55.0% | -15.7% |

| 2022 | 5 | 4 | -3 | -1 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Buybacks ($) | ROE% |

|---|---|---|

| 2025 | 366377 | -189.9 |

| 2024 | 183189 | -6.9 |

| 2023 | 195252 | 8.2 |

| 2022 | 13.9 |

Source: SEC companyfacts cache [F1].

Note: YoY changes for operating income and net income reflect swings into losses; operating cash flows remain persistently negative indicating ongoing liquidity strain.

Mounting Regulatory Headwinds and Customer Concentration Risks

Netcapital operates within a heavily regulated environment characterized by intense oversight from the Securities and Exchange Commission (SEC), Financial Industry Regulatory Authority (FINRA), and Nasdaq Stock Market membership requirements . Heightened regulatory scrutiny has increased legal exposure substantially with the company currently subject to an ongoing SEC investigation that threatens reputation and management bandwidth according to recent filings [S2], [S15]. This investigation entails substantial anticipated legal costs.

The company’s broker-dealer licensing efforts require rigorous compliance audits which divert scarce operational resources towards risk mitigation rather than revenue-generating activities. Regular inquiries cover anti-money laundering procedures, registration compliance and disclosure mandates reflective of a FINRA regulatory audit environment [S6], emphasizing structural hurdles within this niche.

Another critical vulnerability is extreme customer concentration risk: for Q3 2025 the largest single customer represented roughly 73% of revenues—a substantial exposure that jeopardizes revenue stability should this client’s demand decline or contract terms shift unfavorably [S6], [S7]. Earlier quarters also showed similarly concentrated profiles with three clients accounting for over half of all revenues combined.

This concentration compounds risks posed by ongoing litigation potential stemming from federal investigations plus the inherent volatility tied to exposures within innovative but less liquid equity securities held long term by the company’s advisory segments [S8].

Emerging Strategic Focus: Broker-Dealer Services and Blockchain Cybersecurity Acquisitions

In response to revenue declines and pressure on its traditional funding portal model centered on Reg A & D offerings facilitation through crowdfunding platforms like netcapital.com [S13], Netcapital has broadened its strategic focus towards services more directly aligned with broker-dealer operations. This leverages existing regulatory know-how while aiming for higher-margin opportunities via licensed intermediations.

Recent asset acquisitions underpin this pivot: notably an acquisition on January 2nd, 2026 included Iverson Design LLC’s digital design studio assets — encompassing AI-driven graphic design capabilities — intended to enhance integrated product offerings around branding and marketing for growing issuer clients [S23]. Furthermore on December 3rd, 2025 Netcapital purchased Rivetz Corp.’s “Rivetz Network,” which combines hardware-based cybersecurity with blockchain technology aimed at mobile computing environments [S25], broadening exposure into next-generation tech sectors.

These moves reflect an effort to diversify beyond traditional funding portals by embedding cybersecurity innovation and enhanced service lines adjacent to their brokerage platform development initiatives targeted initially at exemption-based fundraising structures under Reg A & D rules ,[S21],[S25]. However competitive barriers remain high given entrenched incumbents controlling access to scale required for profitable brokerage business models.

Liquidity Crunch: Cash Position, Debt, and Going Concern Implications

Liquidity concerns are paramount for Netcapital as evidenced by current assets totaling approximately $1 million against current liabilities near $4 million as of January 31st, 2026 — yielding a distressingly low current ratio of roughly 0.26 consistent with shortage of readily available working capital necessary for ongoing operations [F1].

Repeated disclosures emphasize management’s recognition that historical cash flow deficits coupled with sustained operational losses raise “substantial doubt” regarding their ability to continue as a going concern absent successful refinancing or capital raises through private placements or debt markets [S9], [S11], [S12], [S13], [S16], [S17].

Operating cash flow deficits hovered above $4 million annually converting into cumulative negative free cash flow aggravating balance sheet stress not offset by asset sales or meaningful internal cash generation given losses worsened significantly post-FY2023 [F1]. Managerial disclaimers caution on failure probability if additional external funding falls short requiring drastic reductions or even cessation of operations.

Moreover insolvency risk is exacerbated by volatile valuation of equity securities held in private companies where impairment charges above $2 million were recorded due to lack of liquid markets curtailing balance sheet reliability over near term periods [S18].

Capital Allocation Review: Diminishing Returns, Buybacks, and Dividend Absence

The firm prioritizes capital preservation amid financial distress having ceased dividend payments entirely; there is no indication dividends have been paid historically reflecting retained losses eroding shareholder returns [F1], [S27]. Small share buyback programs occurred over FY2023-24 but the scale—sub few hundred thousand dollars—is negligible relative to market capitalization or cash burn illustrating absence of any meaningful capital return strategy during crisis period.

Return on equity calculations depict deeply negative metrics approximating -189% for FY2025 given soaring net losses against shrinking equity base (from over $37.9M in FY2024 down substantially) signaling persistent destruction of shareholder value rather than creation [F1]. Long-term negative ROE well below typical cost-of-equity thresholds underscores inefficiency driven by both unprofitable core operations and impairments on illiquid private holdings.

Negative operating cash flows reinforce poor capital efficiency raising questions about sustainability without immediate structural improvements or external recapitalization.[F1]

Outlook Considerations: Milestones to Watch Amid Ongoing Investigation and Market Pressures

With no explicit forward guidance observed in filings—the company faces uncertainty contingent on several key developments:

- Resolution timeline and outcome details regarding ongoing SEC investigation which could dictate management focus allocation and reputational damage severity affecting client retention or new business wins ([S2],[S14]).

- Ability to diversify away from highly concentrated customers possibly via expanded broker-dealer client acquisition targeting Reg A/D offerings fostering more stable recurring fee revenues (,[S13]).

- Execution success on integrating newly acquired digital design assets plus blockchain cybersecurity technology from Rivetz aimed at augmenting product portfolio breadth (,[S25]).

- Capital access events such as private placements or public offerings that can relieve acute liquidity challenges before Nasdaq delisting deadlines set at August 3rd, 2026 require attention due to imminent trading suspension risks tied to sub-$1 stock price violations ([S27]).

- Any operational restructuring outcomes designed to reduce cost bases while maintaining compliance obligations amid increased FINRA audits will demonstrate managerial agility under pressure.

In sum though ambitious strategic pivots offer avenues toward stabilization or eventual growth expansion their success is conditioned critically on overcoming steep regulatory hurdles alongside resolving acute balance sheet fragilities within short-term horizons.

This analysis synthesizes publicly filed regulatory disclosures up through March 19th, 2026 without offering investment advice but aims to provide a clear-eyed view of Netcapital Inc.’s precarious financial position alongside its emerging repositioning efforts within evolving financial services niches.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments