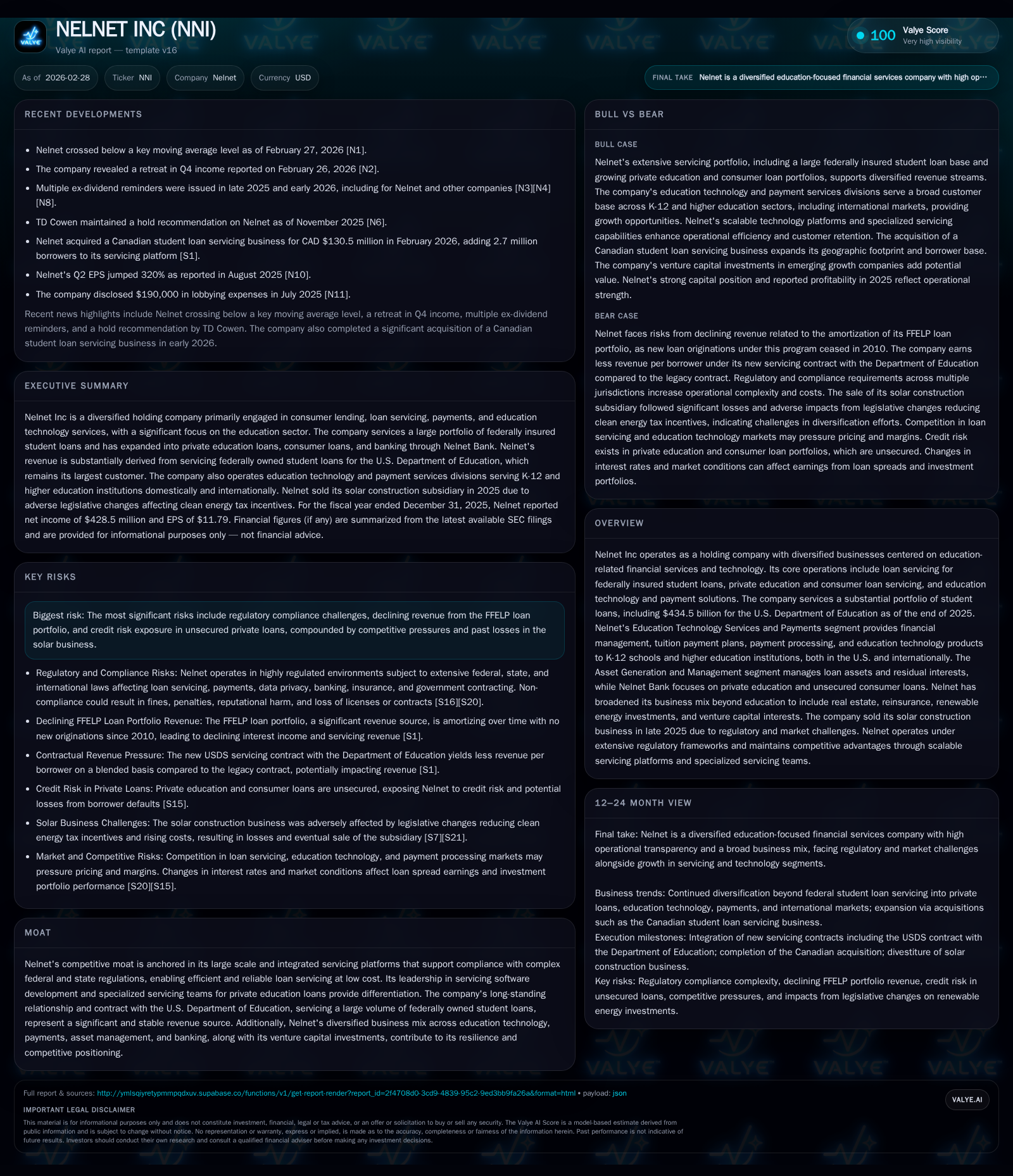

Nelnet's Shift from Loan Servicing to Diversified Education Financial Solutions

Nelnet Inc is transforming its business model from a focus on federal student loan servicing to a broader portfolio encompassing education technology, payments, and banking.

Originally centered on servicing federally insured student loans, Nelnet has faced natural revenue compression due to the decline of its FFELP portfolio. In response, the company has strategically diversified into private lending, education technology platforms, and payment services, including an expanding international footprint. While net income surged strongly in 2025, driven partly by operational efficiencies and non-core gains, cash flow trends signal increased reinvestment and capex outlays. Regulatory complexities and credit risks in unsecured loans pose notable challenges. Continued contract renewals with the U.S. Department of Education and growth in non-loan financial solutions will be critical milestones to watch.

Historical Revenue and Income Drivers Reflecting FFELP Legacy

Nelnet's origins lie firmly rooted in servicing federally insured student loans established under the Federal Family Education Loan Program (FFELP). Despite the program's discontinuation of new originations as of July 2010 per the Health Care and Education Reconciliation Act of 2010 [S1], Nelnet has continued to generate significant income from its residual FFELP loan portfolio. As of December 31, 2025, this portfolio stood at approximately $7.6 billion [S1][S9]. Although substantial, it is markedly lower than previous years due to ongoing paydowns.

Interest income arising from this shrinking FFELP portfolio historically contributed a large portion of Nelnet’s revenue stream; however, the gradual attrition has inevitably compressed these returns. The company's overall loan servicing operations remain large-scale yet face secular headwinds tied directly to this legacy asset decline [S18].

Concurrent with managing legacy FFELP loans, Nelnet services a much larger block — around $434.5 billion in federally owned student loans — on behalf of the U.S. Department of Education as part of its Unified Servicing and Data Solution (USDS) contract initiated in April 2024 [S15]. This government contract contributes about 21% of total revenue and underpins roughly two-thirds of the Loan Servicing and Systems segment revenue [S15]. While USDS contract fees are typically lower per borrower than prior contracts, they replace revenues lost from legacy servicing agreements.

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|

| 2025 | 428 | 423 | 26 | +132.8% |

| 2024 | 184 | 663 | 21 | +101.1% |

| 2023 | 92 | 433 | 74 | -77.5% |

| 2022 | 407 | 684 | 59 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Buybacks ($mm) | FCF ($mm) | ROE% |

|---|---|---|---|

| 2025 | 69 | 397 | 11.6 |

| 2024 | 83 | 642 | 5.5 |

| 2023 | 28 | 359 | 2.8 |

| 2022 | 98 | 625 | 12.7 |

Source: SEC companyfacts cache [F1].

Note: Dividends last paid were in 2018; recent years show no dividend distributions.

Shifting Business Mix: Diversification Beyond Traditional Loan Servicing

Getting ahead of inevitable declines in FFELP interest income, Nelnet strategically broadened its business mix across several fronts [S1][S4]. A core pillar is Nelnet Bank (established in 2020), an FDIC-regulated Utah-chartered industrial bank focusing on private education loans and unsecured consumer credit which complemented traditional federal portfolio exposure [S9][S10]. As of December 31, 2025, Nelnet Bank held approximately $958 million in loans alongside a growing deposit base totaling $1.76 billion [S14][S10]. This segment targets refinancing options tailored to emerging private credit borrowers nationwide across all states plus D.C.

Another diversification vector is the company's Education Technology Services and Payments (ETSP) segment operating under Nelnet Business Services branding [S4][S13]. This includes multiple divisions:

- FACTS: a dominant provider for K-12 tuition management engaging approximately 12,000 private schools domestically.

- Nelnet Campus Commerce: delivering integrated payment solutions for over 1,200 higher education campuses serving upwards of eight million students.

- Nelnet Payment Services: providing PCI-compliant transaction processing covering mobile wallets, in-person terminals, online portals earning recurring fees from credit card and ACH channels.

- Nelnet International: focused mainly on Australia/New Zealand/Asia-Pacific regions targeting ~600 schools across ~70 countries generating steady revenue streams [$9 million annually] internationally [S4].

This integrated service fabric supports resilience against single-segment downturns by leveraging scalable platforms rooted both domestically and abroad.

Net Income Surge vs Cash Flow Moderation: Dissecting 2025 Financials

Nelnet exhibited impressive net income growth jumping approximately 133% year-over-year to $428 million for calendar year 2025 [F1]. This leap reflects enhanced operational efficiencies within core servicing contracts but also includes significant non-recurring items such as gains related to ALLO divestment activities reported in news [N2][S25].

Conversely, operating cash flow contracted sharply by over one-third to about $423 million largely reflecting working capital shifts and timing differences on receivables/payables linked to growing payment services volumes [F1]. Capital expenditure climbed strongly (+25%) reaching roughly $26 million as Nelnet invested further into technology infrastructure enhancements supporting its diversified digital payment platforms [F1][S21].

Despite weaker cash flow momentum relative to earnings growth, free cash flow remains solid near $397 million given controlled capex spend [F1]. Buybacks resumed moderately with share repurchases totaling nearly $69 million during the year continuing a pattern evident since at least early 2020s while dividends have remained suspended post-2018 [F1][N3]. As a result leverage ratios stayed conservative with book equity rising to about $3.7 billion underpinning an ROE near 11.6%, underscoring capital efficiency despite changing business dynamics.

Innovation in Education Technology and Payment Services Segments

The ETSP segment exemplifies Nelnet’s pivot towards service-based technology innovation intertwined with financial transactions management [S4][S13]. Nelnet Payment Services recorded ~$64 million revenue in 2025 up from ~$59 million prior year driven by enhanced adoption of PCI-compliant mobile payments and expanded processing volumes [S4]. Key offerings include robust payment gateway integration spanning credit/debit card acceptance through secure hosted services coupled with ACH automation—crucial for educational institutions aiming to streamline tuition collections.

Further technological capabilities extend into integrated campus commerce including storefront e-commerce platforms allowing departments across universities to monetize merchandise seamlessly along with campus cashiering solutions managing everything from meal plan payments to parking fees with unified back-end reconciliation workflows [S27][S28].

Online billing & refunds provide full regulatory compliance especially accounting for federal refund mandates essential for higher education financial offices [S27]. In K–12 markets via FACTS brand products such as advanced accounting systems combined with financial aid management tools support sophisticated grant assessments while subscription-based SaaS products deliver curriculum management with video AI-powered teacher evaluation software enabling evidence-driven instructional coaching—the latter reinforcing customer stickiness through differentiated tech capabilities rarely matched by peers [S11][S13].

Internationally through Nelnet International’s platforms catering primarily Australia/New Zealand/Asia-Pacific markets revenue contribution stabilized around $9 million annually as scale develops providing footholds for further global expansion opportunities [S4].

Regulatory Landscape and Its Impact on Business Operations

Operating extensively across loan servicing, payments technology, banking, insurance reinsurance subsidiaries and even past renewable energy ventures subjects Nelnet to a wide gamut of regulatory regimes nationally and abroad [S8][S16][S17].

Loan servicing operations must continually comply with evolving federal regulations under Title IV HEA provisions enforced by the Department plus oversight by Consumer Financial Protection Bureau (CFPB), state licensing regimes—with many states imposing unique requirements raising compliance complexity—and multi-jurisdictional data privacy/security laws including FERPA/GLBA or Canada’s provincial statutes following recent acquisition of student loan servicer NDS Canada managing millions of Canadian borrowers [S1][S8][N2].

Payment services require adherence to PCI DSS standards ensuring transaction security while contractual obligations incorporate adherence to ACH network rules—noncompliance carries reputational risk alongside potential fines or litigation exposures arising from breaches or privacy incidents [S8].

Complicating matters further are recent legislative changes linked to solar tax credits following enactment of "One Big Beautiful Bill" which curtailed clean energy incentives forcing exit from solar construction subsidiary NRE after sustained losses mostly attributable to margin compression exacerbated by tariff costs impacting supply chains designated "foreign entity of concern"—raising costs and curtailing project viability abruptly [S2][S21].

Overall rising regulatory scrutiny pressures operating leverage while elevating cost structures mandating continuous investment into compliance infrastructures remotely connected but relevant toward overall strategic risk management.

Capital Allocation: Shareholder Returns, Buybacks, and Investment Trends

Nelnet has prioritized disciplined capital allocation balancing buybacks, modest capex investment in its growth-oriented technology initiatives while suspending dividends since late last decade reflecting strategic reinvestment priorities amidst portfolio transitions [F1][N3]. Buyback activity averaged between $28 million (2023) up toward nearly $83 million (2024), settling at just under $70 million repurchased during fiscal 2025 signaling steady shareholder return appetite within manageable capital budgets [F1].

Simultaneously the Company manages an extensive venture capital portfolio valued around $327 million carrying amount that includes stakes in over a hundred early-stage enterprises globally but notably Hudl Inc., a leading sports performance analytics SaaS firm with large international adoption reflective of expertise transcendence beyond pure finance [S6].

Real estate holdings consist primarily of commercial properties valued near or above $230 million acquired through partnerships leveraging specialist operators allowing balance sheet diversification without overly concentrated risk exposure typical among sector peers reliant solely on financial assets originations/servicing businesses [S5][F1].

The company’s debt posture remains conservative with limited outstanding debt facilitating flexibility amid economic cycles alongside liquidity buffers evidenced by ~$296 million cash/equivalents held at fiscal year-end providing runway for opportunistic deployment into technology or loan acquisitions supporting diversification ambitions.

Future Outlook: Risks, Growth Prospects, and Strategic Milestones

Looking ahead Nelnet faces dual forces shaping performance potential: accelerated attrition pressures within its diminishing FFELP loan book erode legacy interest income bases long-term even as servicing contracts for federally owned loans continue providing essential revenue stabilization subject to multi-year USDS agreements culminating no earlier than April 2028 plus extensions available thus warranting monitoring renewal terms closely given their materiality (>21% total revenues) [N1][N2][S15].[N2] indicates Q4 income retreat aligning with portfolio paydowns.

Growth prospects depend heavily on scaling private education loan portfolios managed through AGM/Nelnet Bank offering higher yield albeit higher credit risk segments requiring prudential underwriting calibration especially amid macroeconomic headwinds potentially raising defaults or charge-offs on unsecured consumer lines requiring vigilant asset quality controls supported by proprietary servicing platforms incorporating specialized teams familiar with these niches absent federal guarantees unlike FFELP exposures [S19][S7].[N1]

Concurrently expansion within education technology services including vendor-funded SaaS subscriptions alongside increasing penetration in international markets suggests recurring revenue thickening beyond transactional volume-dependent feeder lines highlighting platform stickiness critical versus fragmented competitors primarily offering commoditized payment acceptance solutions lacking integrated academic management features or deep sector domain exclusivity seen at FACTS or Campus Commerce units.[S13]

Risks remain pronounced around intensifying regulatory compliance cost burdens spanning disparate jurisdictions’ privacy statutes compounded by fragile consumer protection laws dynamically evolving potentially impacting product design especially tuition finance segments where recent federal/state scrutiny heightens transparency/disclosure demands.[S8] Solar investment divestiture underscores vulnerability when external policy influence materializes unexpectedly indicating prudence warranted when evaluating future non-core business lines adjacent but not intrinsic to core expertise.[S2][S21] Monitoring contract renewal outcomes coupled with private loan portfolio seasoning will offer key signals shaping trajectory over next two-to-three years.

This analysis synthesizes factual information drawn exclusively from referenced SEC filings ([F1], [S#]) and verified news sources ([N#]). It purposefully avoids speculative forecasting or investment recommendation language consistent with Valye News internal research standards regarding coverage objects within student lending & education finance sectors.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments