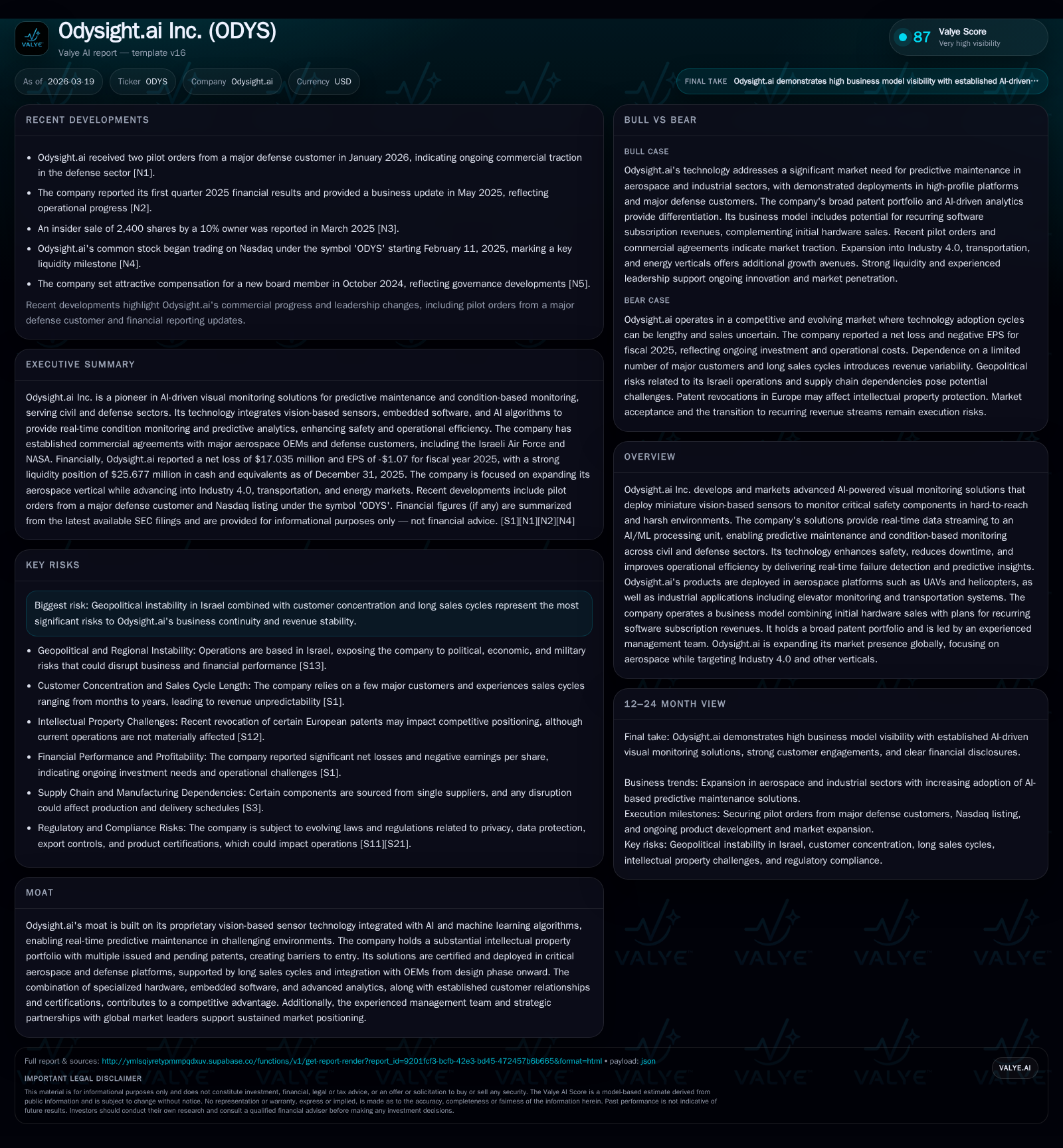

Odysight.ai’s Scaling Challenge: From Proof-of-Concept to Sustainable Revenue Amid Operational Losses

Odysight.ai pioneers AI-powered vision-based predictive maintenance technology with aerospace foothold, facing growth and profitability hurdles.

Odysight.ai Inc. leverages miniature vision sensors combined with AI/ML algorithms to address predictive maintenance in inaccessible, high-risk environments, mainly in aerospace and industrial sectors. The company has secured key defense and aerospace customers and progressed from trials to commercial rollouts but remains unprofitable with widening operating losses and negative operating cash flow as of 2025 [F1][S1][S4]. Growth is driven by expanding aerospace contracts and emerging Industry 4.0 applications, while long sales cycles, geopolitical risks, and tariff-induced supply chain pressures cloud near-term revenue visibility [S1][S21][S4]. Continued R&D investment aims to sustain technological leadership; capital allocation focuses on growth without dividends or buybacks [F1][S25].

Company Overview

Odysight.ai Inc. develops advanced visual monitoring solutions using miniature camera-based sensors integrated with proprietary AI and machine learning analytics for real-time condition-based monitoring (CBM) and predictive maintenance (PdM). Their technology captures detailed visual data from hard-to-reach or harsh environments—such as aircraft components, industrial machinery belts, or transportation systems—and processes this information locally for early anomaly detection before failures occur [S1][S23].

Originating from medical device applications under FDA clearance, Odysight.ai has pivoted toward aerospace and defense markets where its vision-based monitoring offers advantages over traditional vibration or acoustic sensors that often detect faults too late [S1][S16][S23]. Deployments include monitoring critical fasteners on AH-64 Apache helicopters following structural safety concerns, UAVs, other helicopter models like the SH-60 Seahawk, industrial elevator belts, mine trucks, and railway infrastructure [S4][S11][S23].

Historical Financial Performance

Despite technical validation and marquee clients—including the Israeli Ministry of Defense, NASA collaborations, global defense contractors, Israel Railways Ltd., among others—revenue generation remains limited. As of Q3 2022, total revenues were approximately $222 thousand USD [F1]. Operating losses have deepened significantly from -$9.44 million in FY2022 to -$18.14 million in FY2025, nearly doubling over three years. Net income losses followed a similar trend.

Operating cash flow reflects heavy investment in R&D and scaling activities, declining from -$6.09 million in FY2022 to -$13.70 million in FY2025. Capital expenditures remain low relative to overall spending ($56K in FY2025), indicating focus on technology development rather than fixed asset expansion.

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($) | Net YoY |

|---|---|---|---|---|---|

| 2025 | -17 | -14 | -18 | 56000 | -44.8% |

| 2024 | -12 | -8 | -13 | 53000 | -24.6% |

| 2023 | -9 | -10 | -11 | 113000 | +0.2% |

| 2022 | -9 | -6 | -9 | 118000 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2025 | -14 | -67.0 |

| 2024 | -8 | -64.5 |

| 2023 | -10 | -53.0 |

| 2022 | -6 | -80.3 |

Source: SEC companyfacts cache [F1].

The equity base has grown over time through capital raises supporting growth but without profitability.

Growth Prospects

Key growth drivers include:

Aerospace Expansion: Increased penetration into aerospace OEMs supported by compliance with strict certification standards such as FAA regulations and CE certification for European markets. Installed systems span multiple rotorcraft platforms globally [S13][S9].

Industry 4.0 Applications: Expansion beyond aerospace into elevators, railways, mining machinery aligns with Industry 4.0 trends seeking real-time smart monitoring solutions; addressing costly unplanned downtime estimated at $1.4 trillion annually among top global companies [S6][S11].

Recurring Revenue Transition: Currently dependent on hardware kit sales combining sensors and embedded AI processing units bundled with initial algorithm sets; the company plans to develop multi-year software subscription services post-warranty offering enhanced analytics such as fleet management and algorithm upgrades for sustainable revenue streams [S25][S21].

Challenges include long procurement cycles spanning months to years due to complex OEM integrations; customer concentration risk with three major accounts; geopolitical tensions centered on Israel headquarters posing operational risks; evolving tariff regimes increasing component costs potentially compressing margins or affecting customer demand sensitivity [S4][S1][S17].

Forecasts & Milestones

Management has not provided explicit forward-looking revenue guidance but highlights milestones like successful pilot program completions moving into initial commercial deliveries particularly within industrial markets beyond defense/aerospace core segments [S11]. Important future indicators include:

- Growth in purchase order volumes converting into recognized revenues.

- Progression from hardware-only sales toward meaningful software subscription adoption.

- Expansion of strategic OEM partnerships facilitating early design integration.

- Improvement of gross margins through manufacturing scale efficiencies.

Capital Allocation & Returns

No dividends or share repurchases have been declared historically or indicated given the company's ongoing net losses [F1]. Cash and equivalents totaled approximately $25.7 million at year-end 2025 providing operational runway absent new financing.

Return metrics reflect early-stage investment dynamics: approximate return on equity based on net loss relative to shareholder equity is negative ~67% for FY2025 consistent with technology commercialization phases prioritizing growth over profitability [F1].

Competitive Position & Intellectual Property

Odysight.ai’s competitive edge derives from its integrated vision-based sensing technology combined with advanced AI/ML analytics capable of detecting subtle anomalies ahead of failure—a domain traditionally dominated by less granular vibration or acoustic sensing methods prone to delayed fault detection [S7][S16].

Its intellectual property portfolio includes issued patents across multiple jurisdictions alongside numerous pending applications; however European patent revocations occurred recently though these are not expected to materially impact ongoing operations [S8][S19].

Partnerships with prominent aerospace OEMs such as Elbit Systems and Israel Aerospace Industries provide vital market access leveraging established distribution networks while early design-phase integration strengthens customer lock-in reducing churn risk once embedded solutions deploy broadly [S4][S13].

Risk Factors Summary

Principal risks include:

- Geopolitical instability related to Israeli headquarters operations impacting continuity.

- Customer concentration risk coupled with protracted sales cycles introduce forecasting uncertainties.

- Tariff-induced supply chain cost pressures potentially eroding margins or deterring price-sensitive customers.

- Intellectual property challenges including ongoing patent litigation may constrain product development timelines.

- Regulatory compliance complexity across multiple jurisdictions could delay market entry or increase costs.

- Sustained negative financial performance heightens dependence on external capital if operational efficiencies are not realized.

- Competitive threats from alternative sensing technologies could erode technological advantages.

Conclusion

Odysight.ai occupies a specialized niche intersecting computer vision technology with AI-driven predictive analytics targeting safety-critical infrastructures primarily within aerospace while expanding into Industry 4.0 verticals. Despite technical validation supported by marquee customers and an extensive IP portfolio combined with partnership-driven commercial traction beyond pilot phases remains financially nascent.

Operating losses have deepened amid scaling efforts without reported sustainable revenue ramp or subscription monetization underscoring the challenge of transitioning innovation maturity into scalable profitable operations amidst geopolitical tensions and tariff uncertainties.

Close monitoring of order conversion rates alongside progress on recurring software services adoption plus managing production cost pressures will be essential for Odysight.ai’s evolution toward financial sustainability while protecting its innovation moat against intensifying competition remains imperative.

This report synthesizes publicly available documents filed by Odysight.ai Inc., including SEC filings as of March 19, 2026 , without offering investment advice.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments