Orion Bliss Corp.'s Growth Ambitions Confront Liquidity Constraints and Market Realities

The latest quarterly report reveals mounting liquidity pressures juxtaposed with Orion Bliss’s aspirations to expand its natural hair care product footprint beyond e-commerce.

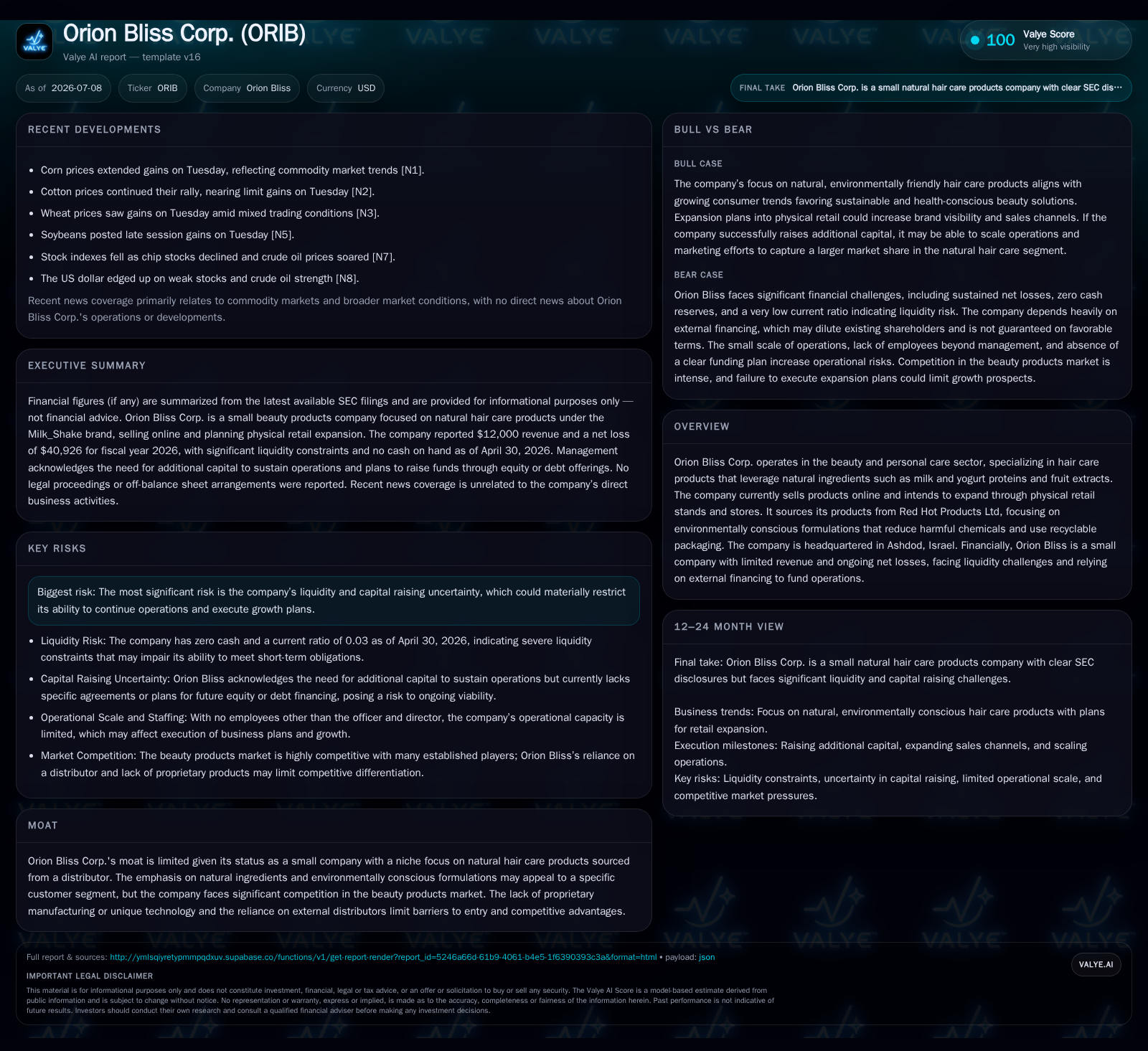

Orion Bliss Corp. remains a small player in the beauty sector focused on natural ingredient hair care products sourced from a third-party distributor, currently dependent on a solely online sales channel. The February 2026 quarter disclosed zero revenue growth with ongoing net losses, underscoring severe liquidity issues highlighted by a near-zero current ratio and no cash on hand as of April 2026. While the company aims to grow through retail stands and stores, this expansion is presently stalled by financial constraints and an absence of proprietary manufacturing capabilities, capping margin potential. Near-term viability hinges critically on successful capital raises amid a competitive market landscape dominated by larger, vertically integrated incumbents.

Latest Quarter Reveals Critical Liquidity Pressures That Stall Growth Ambitions

As of April 30, 2026, Orion Bliss reported zero cash and equivalents alongside current assets of just $5,041 against current liabilities exceeding $181,800—delivering an alarmingly low current ratio of roughly 0.03 [F1]. Total debt stood at about $45,500 with no off-balance sheet obligations flagged [F1][S2]. This indicates a critical dependency on equity or debt raises to extend the company's runway beyond the coming quarter unless operating cash flows improve sharply.

Such acute financial constraints impose immediate existential pressure on Orion Bliss’s ability to execute its broader strategic plans centered on growth through product line expansion and channel diversification.

"Natural" Product Promises Amid Limited Margin and Scale Realities

Orion Bliss’s product portfolio focuses exclusively on "Milk-Shake" branded hair care items sourced from Red Hot Products Ltd., featuring natural ingredients such as milk proteins, yogurt extracts, and fruit components aimed at enhancing hair health while embracing sustainability principles — including reductions in sulfates, parabens, sodium chloride, and use of recyclable packaging materials [S1]. This clean beauty positioning aligns with consumer trends favoring ingredient transparency and reduced environmental impact.

However, reliance on third-party sourced formulations restricts Orion Bliss’s capacity to innovate proprietary products or protect unique formulations via intellectual property rights. Consequently, margin expansion opportunities are limited; while natural ingredient narratives can support premium pricing within niche segments, absence of brand scale or novel R&D narrows pricing power relative to established incumbents who combine own manufacturing with large-scale marketing reach. Lack of patent protection or exclusive technology likewise exposes the firm to easy replication by competitors.

Therefore, though product differentiation has appeal for select eco-conscious consumers seeking vibrant haircare outcomes without harmful additives, gross margin improvement depends heavily on scaling brand equity and improving distribution breadth rather than formulation innovation alone.

Sourcing Strategy Dependency: Red Hot Products Ltd Enables but Caps Control

Orion Bliss operates in the beauty value chain as a brand development and marketer relying entirely on Red Hot Products Ltd. for manufacturing and distribution sourcing [S1]. This upstream dependency caps operational control across key levers such as inventory management flexibility, supply chain resilience, and responsiveness to changing consumer preferences or formulation tweaks.

In an industry where speed-to-market for new product launches often defines competitive success alongside deep supply-chain integration, the outsourcing model here undercuts agility. While utilizing a reputable distributor reduces initial capital investment requirements, the tradeoff is diminished bargaining leverage over cost inputs and limited capacity to optimize gross margins through direct production efficiencies or proprietary packaging innovation.

This structural reliance highlights that any meaningful margin gains would necessitate cultivating closer collaboration with suppliers or evolving toward partial self-manufacturing capabilities.

E-Commerce Origins with Tangled Path Toward Physical Retail Footprint Expansion

To date Orion Bliss’s sales predominantly flow through online channels consistent with many contemporary small beauty startups emphasizing direct-to-consumer engagement via digital platforms [S1]. The company publicly articulates ambitions to develop physical retail stands and eventually stores complementing e-commerce efforts—a common growth vector intended to increase brand visibility and diversify revenue streams.

However, expanding into brick-and-mortar environments demands considerable investments in inventory buildup at retail points, management bandwidth for operational complexity, and often higher fixed costs that challenge smaller companies without deep pockets. The lack of immediate capital availability undermines these expansion plans.[S2] Equally important are shifts in channel mix impacts: physical retail typically entails different customer acquisition cost profiles, inventory turnover rhythms, and pressure on gross margins due to wholesale discounting practices relative to direct online sales.

Such multichannel transitions require careful execution supported by sufficient funding—a condition currently unmet—making them formidable hurdles at present.

Competitive Terrain: Niche Sustainability Versus Global Brand Scale and Pricing Power

Orion Bliss competes within the intensely crowded personal care space marked by dominance from global brand leaders like L'Oréal and Estée Lauder who enjoy expansive scale-driven advantages including broad distribution networks, significant marketing budgets, and powerful brand equity translating into enduring pricing power. These incumbents capitalize on proprietary research pipelines coupled with diverse product portfolios spanning multiple price tiers.

Conversely, niche players focusing on natural ingredients sustainability appeal represent smaller slices of the market characterized by higher customer scrutiny around ingredient provenance but often suffer from limited recognition outside their loyalists. Without committed substantial marketing investments capable of driving efficient customer acquisition at scale—which Orion Bliss currently lacks—the ability to break through competitive noise remains marginal.[S1][S2]

This scenario creates pressures on customer acquisition costs and constrains top-line momentum unless differentiation becomes materially stronger or distribution expands meaningfully.

Key Growth Opportunities Hinge on Multi-Channel Execution and Marketing Efficiency Gains

Achieving sustainable growth will depend critically on Orion Bliss executing its channel diversification plans effectively while optimizing marketing spend. Increased retail distribution could raise average order values by exposing products to impulse buyers unacquainted previously through online platforms. However, success here requires prudent inventory management balancing turnover against stocking risks common in perishable personal care items.

Simultaneously improving customer acquisition cost performance through sharper branding using social media influencers or targeted digital campaigns could unlock volume growth necessary for incremental economies of scale.[S1][S2] New product introductions within Milk_Shake’s range—if backed by credible trial success rates—may also fuel repeat purchase cycles essential for long-term brand loyalty. Efficiently orchestrating these levers amidst tight funding will be pivotal given ongoing operating losses.

'Capital Raise Imperative': Funding Needs Define Near-Term Survival and Strategy Risks

Management reiterates repeatedly that without additional capital infusions via equity or debt issuances sustained operations remain untenable beyond short-term horizons [S2]. No formal lines of credit exist; past financing has relied on private placements plus director loans carrying inherent uncertainty regarding availability or terms. Increased operating expenses linked to inventory acquisition, development (typical startup expenditure), and amplified marketing efforts underscore escalating cash burn. Absence of committed funding arrangements injects risk not only into operational continuity but also strategic flexibility limiting ability to seize market opportunities or counter competitive threats proactively. Further issuances risk shareholder dilution while funding uncertainties increase execution risk profiles notably.[S2]

What To Watch: Milestones in Retail Opening and Financing That Will Validate Execution Capacity

Key near-term events will provide clarity regarding Orion Bliss’s trajectory: whether concrete retail stand openings materialize signaling channel expansion real progress; equity or debt capital raises occur easing liquidity pressures; disclosures around marketing campaign effectiveness reflected through upticks in sales volumes or lower acquisition costs will offer early evidence of scalable customer engagement [S1][S2]. Without signals confirming successful navigation of these milestones, running concerns around survival will persist underscoring urgency for delivering operational inflection points aligned with financial stabilization.

Financial Profile Discussion: How Balance Sheet Constraints Shape Orion Bliss’s Strategic Choices

Orion Bliss's financial position at April 30, 2026 depicts critical imbalance between liquidity resources and obligations: zero reported cash reserves complicate ongoing operational funding under rapidly approaching maturities [F1]. Total debt stands at approximately $45,500 comprising notes payable plus director loans—amounts small in absolute terms but material relative to company scale given minimal assets available for offsetting liabilities. Current liabilities dominate working capital calculations resulting in a severely deficient current ratio (~0.03) that flags acute solvency stress absent prompt corrective capital inflows [F1]. These conditions rationalize management’s explicit warnings about imminent financing needs documented extensively throughout recent quarters underscoring persistent going concern uncertainty [S2]. Such tight balance-sheet constraints impose hard limits on strategic initiatives requiring upfront investment including but not limited to physical retail expansion, increased inventory procurement, or amplified digital advertising spend—all essential growth enablers presently curtailed by funding limitations.

Financial position in context

As of 2026-04-30, companyfacts shows 0 USD in cash and equivalents and $45500 of total debt [F1]. The same snapshot implies net debt of roughly $45500, keeping balance-sheet context relevant but secondary to the operating story [F1]. Current assets of $5041 and current liabilities of $181848 imply a current ratio near 0.03x for 2026-04-30 [F1].

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments