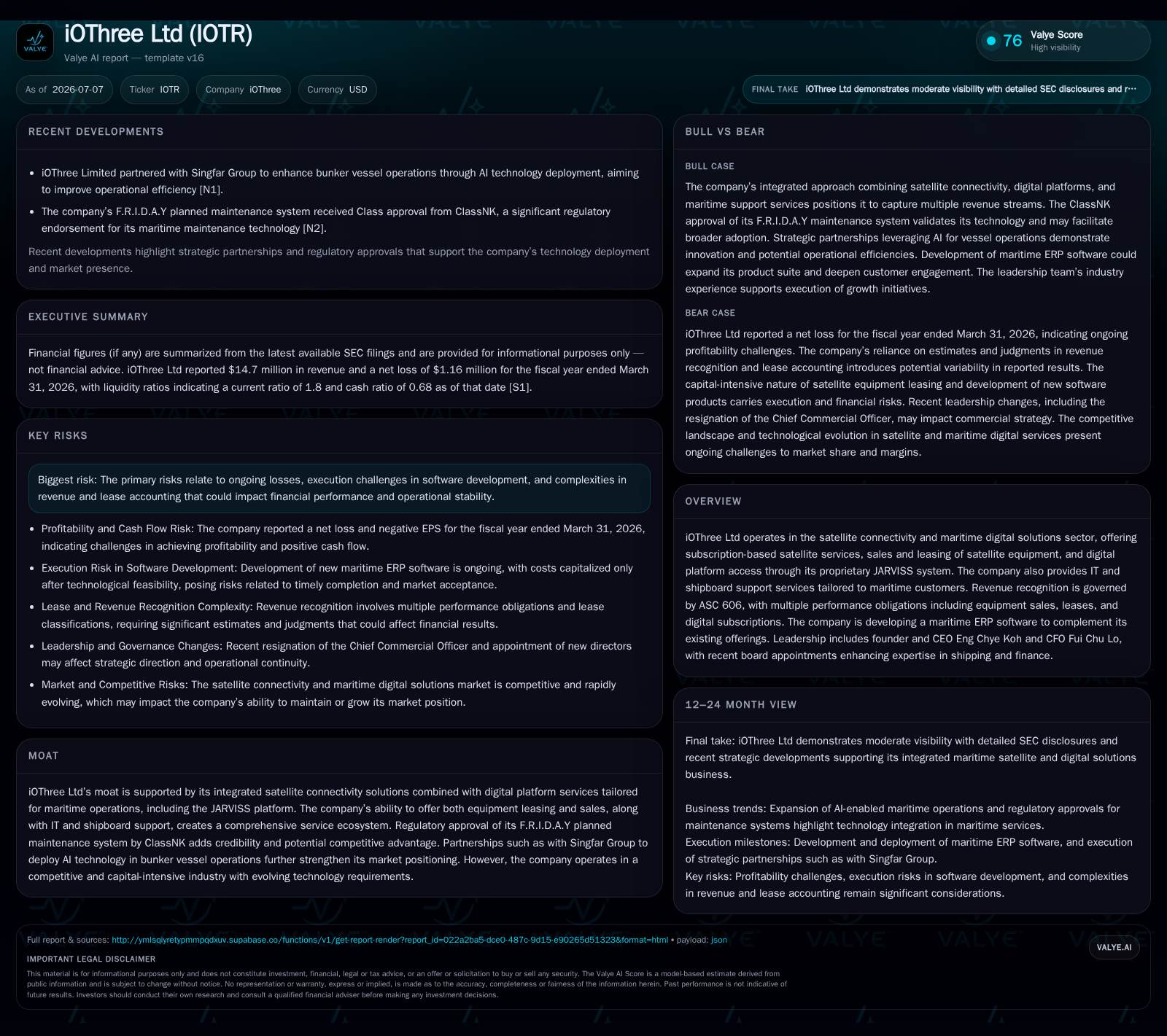

iOThree Ltd Expands Maritime Digital Solutions Amid Rising Losses and Geographic Growth Plans

iOThree Ltd navigates growth in maritime satellite connectivity and digital platforms while managing escalating operating losses.

iOThree Ltd operates an integrated maritime connectivity and digitalization business focused on satellite services, equipment leasing/sales, and proprietary digital platforms including JARVISS. Recent filings reveal a strategic push for geographic expansion into Asia and the Middle East accompanied by significant growth in digital solutions revenue. Despite revenue rising 40% year-over-year to $14.7 million, iOThree faces steepening net losses driven by increased administrative costs and expansion investments. The company’s subscription-based satellite offerings combined with digital IT and operational technology support position it uniquely within the maritime value chain. Execution risks notably center on software development complexity and managing multi-obligation ASC 606 revenue recognition amid capital-intensive equipment leasing. Financially, liquidity remains adequate with a strong current ratio and low net debt, but sustained negative operating cash flow underscores the challenge of scaling profitably in this specialized market segment.

Recent Operating Update

In its latest quarterly filing dated January 26, 2026, iOThree Ltd announced significant board changes that enhance its maritime operational and financial expertise. The appointment of Mr. Yangan Ou as director and Mr. Yufei Li as independent director brings seasoned leadership with deep experience in bulk carrier operations, shipping finance, and audit advisory, aligning with iOThree’s strategic focus on expanding into offshore maritime markets across Asia and the Middle East [S2]. The orderly resignation of the Chief Commercial Officer without operational disagreements further reflects stable governance transitions.

The company’s annual report filed July 7, 2026, outlines aggressive growth initiatives targeting new Asian countries and Middle Eastern markets to diversify revenue streams beyond its core Singapore base [S1]. This geographic expansion encompasses scaling satellite equipment sales and leasing alongside digital solution offerings, including IT support and proprietary platforms. These efforts require upfront investments in personnel, marketing, office infrastructure, and distribution networks to support broader market penetration

Business Model Overview

iOThree operates two primary segments: satellite connectivity solutions and digitalization/other solutions. The satellite connectivity segment combines subscription-based satellite services with sales and leasing of shipboard network equipment, enabling shipboard network management and fleet connectivity [S1]. The digitalization segment includes proprietary software platforms such as JARVISS—"Just A Really Very Intelligent System"—which integrates IoT and vessel management applications, as well as IT and operational technology (OT) support services and the emerging maritime ERP system FRIDAY

This integrated business model spans multiple layers of the maritime connectivity value chain, from physical network access provided via leased or sold hardware to high-value software-enabled asset and operational management. Revenue is generated through recurring subscription fees for satellite connectivity, equipment sales and leasing income, and software licensing or service fees for digital platforms.

Revenue recognition follows ASC 606 guidelines, requiring the separation of multiple performance obligations within bundled contracts that include lease components (equipment) and non-lease components (digital subscriptions and services) [S1]. Judgments on standalone selling prices materially affect the timing and amount of revenue recognized, reflecting the complexity of maritime contracts that bundle hardware and software services

Subscription revenues provide a more predictable recurring income stream compared to equipment sales or leasing, which involve upfront capital expenditures and depreciation schedules impacting gross margin management.

Industry Structure and Competitive Positioning

Operating within the maritime satellite connectivity and digital solutions sector, iOThree interfaces with upstream satellite network operators such as Inmarsat and Iridium, which provide the backbone satellite infrastructure. Downstream, it competes with ship integrators and equipment providers like KVH Industries and Cobham SATCOM, which supply terminal equipment and integration services. Digital platform competitors include Marlink and Speedcast, known for bundling connectivity with advanced fleet management tools.

iOThree differentiates itself through its JARVISS ecosystem, designed specifically for optimized vessel IoT integration and operational technology support onboard ships. Its FRIDAY maritime ERP system holds ClassNK certification, a notable regulatory endorsement that signals compliance quality and reliability in maritime software solutions. Additionally, partnerships deploying AI-enabled bunker vessel operations exemplify the company’s niche technological differentiation, contrasting with peers focused primarily on connectivity or hardware alone.

This integrated solution approach creates customer stickiness by bundling subscriptions, equipment leases, and IT services, increasing switching costs for shipping operators who face compliance and operational risks.

Growth Drivers

iOThree’s FY2026 revenue growth was predominantly driven by its digitalization segment, which more than doubled to approximately $8 million, representing a $4.2 million increase year-over-year [S11,S24]. This surge reflects increased sales of IT equipment and expanded service contracts, consistent with maritime operators’ investments in digital transformation initiatives driven by regulatory mandates such as IMO safety and environmental rules, operational efficiency needs via IoT integration, and a shift toward SaaS-based asset optimization platforms

Satellite connectivity subscription revenues grew approximately 16%, demonstrating resilience in recurring income despite a 30% decline in one-time equipment sales and leasing, possibly due to market saturation or competitive pricing pressures [S24]. Gross margins improved to 21.4%, supported by economies of scale in the digital segment, which increased its margin from roughly 4.3% to 17.4%, while satellite connectivity margins remained stable near mid-20% levels [S9, S22].

The company plans to establish new offices across Asia-Pacific and the Middle East to capture growing regional trade flows. These expansions require substantial upfront capital expenditures and recruitment-driven overheads, indicating potential margin dilution during the rollout phase [S1]. Recent board appointments with shipping logistics and finance expertise aim to mitigate execution risks associated with this growth strategy.

Risks and Constraints

iOThree operates in a capital-intensive industry with several notable risks:

- Continuous R&D investments are necessary to keep pace with rapid satellite technology evolution.

- Complex revenue recognition under ASC 606 requires careful allocation between lease and non-lease components in bundled contracts.

- Regulatory exposure is significant, with dependencies on class certifications such as ClassNK; delays or failures could stall product launches.

- Customer concentration risk exists, with over 23% of receivables aged under 90 days tied to a few large customers, though credit risk remains contained [S20].

- Competitive pressures from global satellite operators advancing integrated bundled offers.

- Execution risk in developing and deploying new software platforms like the FRIDAY maritime ERP system.

- Geographic expansion risks including compliance with foreign laws, local competition, and infrastructure setup costs.

Financially, the company’s net loss widened substantially to approximately $1.16 million for FY2026 from $0.23 million the prior year, driven by increased administrative costs and expansion investments. Operating cash flow turned negative at $2.24 million, reflecting the investment cycle rather than sustainable profitability [F1]. Scaling equipment leasing while improving average revenue per user (ARPU) on subscriptions will be critical for future financial health.

What to Watch Next

Key operational and financial milestones to monitor include:

- Progress in deploying the FRIDAY maritime ERP system, which could enhance platform stickiness and customer retention.

- Successful establishment and operationalization of new offices across Asia and the Middle East, evidencing credible geographic diversification.

- Trends in active satellite connectivity subscription counts and churn rates as indicators of commercial traction.

- Gross margin improvements driven by volume leverage, especially within digitalization services.

- Management’s ability to control general and administrative expenses amid scaling, particularly after IPO-related cost surges.

- Regulatory approvals and classification society endorsements that facilitate broader adoption of digital applications.

- Maintenance of lease receivable repayments and credit quality given customer concentration.

Financial Profile Discussion

iOThree reported revenues of $14.7 million for FY2026, marking a 40.4% increase over the prior year, primarily fueled by the digitalization segment’s doubling of sales [F1]. Gross profit rose to approximately $3.15 million, a 68% increase, lifting gross margin from about 17.8% in FY2025 to 21.4%. This improvement was driven by economies of scale in digital services, which increased their margin from roughly 4.3% to 17.4%, while satellite connectivity margins remained stable near mid-20% levels [S9, S22].

Capital expenditures remained moderate at approximately $0.58 million, focused on equipment acquisition to support service delivery [F1, S15]. Cash and equivalents stood at about $2.12 million at fiscal year-end, against modest total debt of approximately $0.27 million, resulting in a net cash position of roughly $1.85 million. The current ratio of 1.8 indicates adequate short-term liquidity and a working capital surplus to support ongoing operational investments

This analysis integrates iOThree Ltd’s latest financial disclosures with maritime satellite connectivity and digital solutions sector context. The company’s integrated business model, spanning hardware leasing and sales alongside proprietary software ecosystems like JARVISS, positions it uniquely amid peers focused on either connectivity or standalone software solutions. While top-line momentum reflects favorable demand tied to maritime digital transformation and regulatory tailwinds, profitability challenges driven by rising corporate overheads and global expansion efforts underscore execution risks. Monitoring recurring revenue trends, contract mix evolution under ASC 606, and software deployment milestones will be critical to assessing iOThree’s ability to build a sustainable competitive moat in a capital-intensive, rapidly evolving industry segment.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments