Butler National’s Aerospace Product Efficiency and Gaming Operations Underpin Modest Revenue Growth

Aerospace segment gains offset gaming revenue softness amid leadership transition and stable financial footing.

In its latest quarterly update ending January 31, 2026, Butler National Corporation reported a modest 1% overall revenue growth driven by aerospace product advances despite a 5% decline in professional services revenue. Operational efficiency gains reduced aerospace product costs by 12%, significantly boosting segment operating income. The company is navigating a CEO transition with Christopher Reedy’s retirement effective mid-2026, while maintaining strong liquidity metrics. Butler National’s dual-segment exposure to aerospace fabrication and gaming services introduces unique operational dynamics, with aerospace benefiting from backlog growth and subcomponent fabrication expansion, whereas gaming revenues face regional economic headwinds. Cybersecurity oversight remains a board-level priority amidst these developments.

Recent Operating Update

Butler National Corporation’s third-quarter fiscal 2026 results (for the period ended January 31, 2026) reveal a nuanced operating environment balancing growth in aerospace fabrication against softness in professional services revenues tied to gaming [S2]. Total revenue increased modestly by 1% to $20.1 million compared with the prior-year quarter. This aggregate masks a divergence where Aerospace Products revenue grew by 7% to $11.3 million while Professional Services declined 5% to $8.8 million [S17]. The aerospace segment benefits from increased production efficiencies and order flow improvements across special mission electronics and avionics upgrades [S9], supporting stronger operating margins.

Operational cost management played a material role: cost of goods sold within Aerospace Products decreased by 12%, representing a reduction from approximately 71% to about 58% of segment revenue [S8][S17]. These efficiencies derive from expanded internal sub-component fabrication capabilities—partially enabled by a recent adjacent facility purchase in Newton, Kansas—to address capacity constraints noted previously [S8][S9]. By contrast, Professional Services costs rose marginally in absolute terms but declined proportionally reflecting the revenue drop; this segment’s margin contraction reflects increased labor costs amid declining casino patronage and state-mandated higher revenue sharing [S17][S27].

Management also contended with discrete disruptions such as the June 16, 2025 airplane crash into the New Century hangar that temporarily impacted aircraft modifications operations; the facility has since been fully restored [S9]. Adding complexity, CEO Christopher J. Reedy retired effective June 15, 2026 and transitioned into an advisory role on the board until July 1, 2027—signaling a planned leadership succession that emphasizes operational stability during this period of incremental growth [S3].

Business Model Specifics

Butler National operates through two primary segments: Aerospace Products and Professional Services [S18]. The Aerospace Products division engages in engineering design, manufacturing, installation, and aftersales support including avionics upgrades, aircraft modifications, and special mission electronics for military vehicles and commercial aircraft. Its customers comprise commercial aviation operators, defense contractors, government agencies, and allied commercial entities involved in aviation lifecycle enhancement.

Revenue recognition primarily follows the percent completion method tailored for long-cycle aerospace modification contracts varying from one to twelve months—mirroring industry standards for custom engineering projects demanding significant judgment on labor cost estimations and contract progress milestones [S29]. Fixed-price contracts dominate this mix but introduce risk exposure that management monitors closely through backlog evaluation and quarterly profit estimate adjustments.

Professional Services encompasses management of the Boot Hill Casino & Resort in Dodge City, Kansas under state lottery authority oversight. This business line derives income mainly via casino gaming (slots and tables), sports wagering through DraftKings platform integration initiated post-legalization in September 2022, along with ancillary dining and entertainment operations [S18]. Revenue here is subject to regulatory compliance requirements unique to gambling operations including mandated state revenue sharing increases effective December 2024 impacting net income [S27].

This dual-sector model exposes Butler National to dissimilar demand drivers: aerospace relies on capital-intensive fabrication capacity expansion coupled with regulatory retrofits while professional services hinge on consumer discretionary spending influenced by local economic conditions such as employment trends in agricultural processing sectors nearby its casino location [S27]

Industry Structure and Competitive Position

In aerospace manufacturing and modification services—which includes peers like AAR Corp or specialized avionics integrators—operational metrics such as backlog volume, contract mix quality, capacity utilization rates, labor efficiency gains, and fixed-price risk management define competitiveness. Butler National’s strategic investments in expanding sub-component fabrication align with sector thrusts toward vertical integration for margin improvement.

The broader industrial hardware perspective highlights stringent regulatory oversight on product safety standards alongside cybersecurity imperatives given defense contractor involvement [S1]. The Board mandates full oversight on cybersecurity risks reflecting its consequences beyond IT into operational continuity and compliance especially relevant for its Boot Hill gaming subsidiary regulated by the Kansas Racing and Gaming Commission [S1]. In this respect, Butler National’s governance framework appears robust relative to sector norms.

Competitive challenges include customer concentration risks inherent in government contracting sectors paired with cyclicality in commercial aviation spend. Additionally, professional services face regional economic headwinds tightening consumer spend which could persist if industrial employment declines continue impacting discretionary entertainment budgets near their casino premises.

Growth Drivers

Incremental growth prospects lie predominantly within Aerospace Products where continued expansion of fabrication capacity coupled with productive backlog conversion signals durability. The June facility acquisition aims directly at bottleneck alleviation observed when parts demand exceeded prior shop capacities [S8][S9]. New certifications or Supplemental Type Certificates (STCs) under development will further broaden retrofit offerings—critical given ongoing demand for regulatory-driven aircraft modifications globally.

Professional Services’ sports wagering segment shows promise with increasing revenue share via DraftKings platform integration, suggesting digital channel expansion traction despite overall traditional casino volume softness [S11][S27]. Regulatory shifts toward legalized sports wagering underpin this potential.

Moreover, capital expenditure plans prioritizing STCs ($5 million), combined equipment investment ($4.5 million), and building enhancements ($3 million) for FY2026 align resources with anticipated scaling needs across both segments [S20]. Maintaining robust liquidity cushions supports these initiatives while positioning for opportunistic investments or absorbing shocks.

Risks and Constraints

Primary risks encompass cybersecurity threats given data sensitivity in avionics projects plus gambling operation compliance vulnerability; both require ongoing board-level vigilance due to potential reputational and regulatory sanctions impacts [S1]. The company also navigates the challenge of managing fixed-price contract exposures which can compress margins if cost overruns materialize unexpectedly across complex aerospace modifications [S29].

Capacity constraints remain relevant despite recent expansions as ramping skilled labor hiring lags industry-wide shortages constraining production elasticity [S9][S12]. Economic cycles influence aerospace demand; defense spending volatility or commercial aviation downturns could dampen order flows while local economic weakness pressures gaming revenues particularly around their Kansas-based Boot Hill Casino operations where patron visits have fallen due to external employment conditions [S27]. Lastly, high inflationary pressures on materials and labor costs may not be fully transferrable through pricing causing margin pressures short term [S15].

What To Watch Next

Key milestones include monitoring backlog trends particularly in special missions electronics which recently grew due to pre-assembled components readiness facilitating quicker order fulfillment [S9]. Capacity utilization reports following the new facility integration will clarify whether bottlenecks materially abate.

On governance front, observing outcomes related to CEO transition execution through July 2027 will elucidate succession impact on operational strategy integrity [S3]. Updates on capital allocation effectiveness via upcoming quarterly disclosures around STC rollout progress can serve as leading growth indicators.

Gaming segment performance must be tracked closely for stabilization or recovery signals amid ongoing local economic uncertainty; payor behavior changes or additional state regulatory adjustments beyond the already increased revenue share will further influence results.

Lastly, any disclosures around cybersecurity incident occurrences or enhancements will be pertinent indicators of risk management maturity within high-compliance industrial hardware plus regulated gaming environments.

Financial Profile Discussion

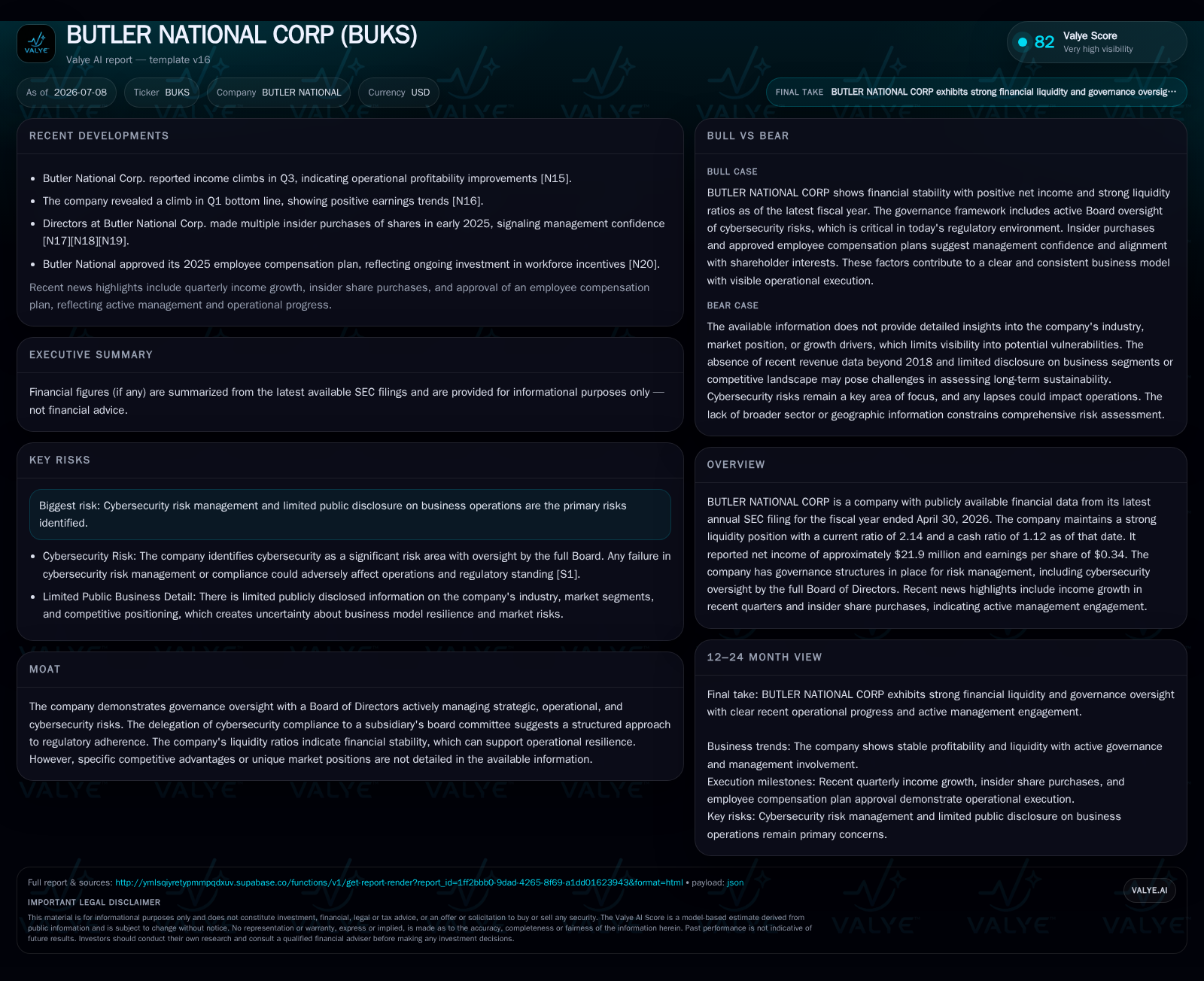

Butler National maintains a healthy financial position anchored by strong liquidity metrics as of April 30, 2026: current assets stood at $67.3 million versus current liabilities of $31.4 million yielding a current ratio of approximately 2.14—a comfortably liquid stance that supports ongoing operations without stress signaling prudent working capital management [F1]. Cash & equivalents at nearly $35.1 million surpass total outstanding debt of roughly $29.6 million resulting in a net cash position of about $5.6 million enhancing financial flexibility [F1].

The company shows moderate leverage calibrated thoughtfully balancing debt service obligations against cash flow generation capacity emphasizing conservative capital structure suited for cyclical industry sectors vulnerable to external shocks characteristic of both aerospace manufacturing cycles and regulated gaming environments.

This analysis integrates verified SEC filings through Q3 FY2026 complemented by contextual industry insights pertinent to Butler National’s dual-segment operations without extrapolating beyond disclosed facts or projecting future guidance absent explicit statements from management [F1]. It applies sector-relevant KPIs such as backlog compositional dynamics, cost efficiencies, contract risk exposure assessments alongside governance factors including cybersecurity oversight practices vital for stakeholder risk understanding.

Financial position in context

As of 2026-04-30, companyfacts shows $35mm in cash and equivalents and $30mm of total debt [F1]. The same snapshot implies net debt of roughly $-6mm, keeping balance-sheet context relevant but secondary to the operating story [F1]. Current assets of $67mm and current liabilities of $31mm imply a current ratio near 2.14x for 2026-04-30 [F1].

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments