Ohio Valley Banc Corp Navigates Elevated Credit Costs and Leadership Change in Q1 2026

Modest earnings decline and commercial loan impairments highlight operating pressures as Ohio Valley Banc Corp adjusts executive leadership.

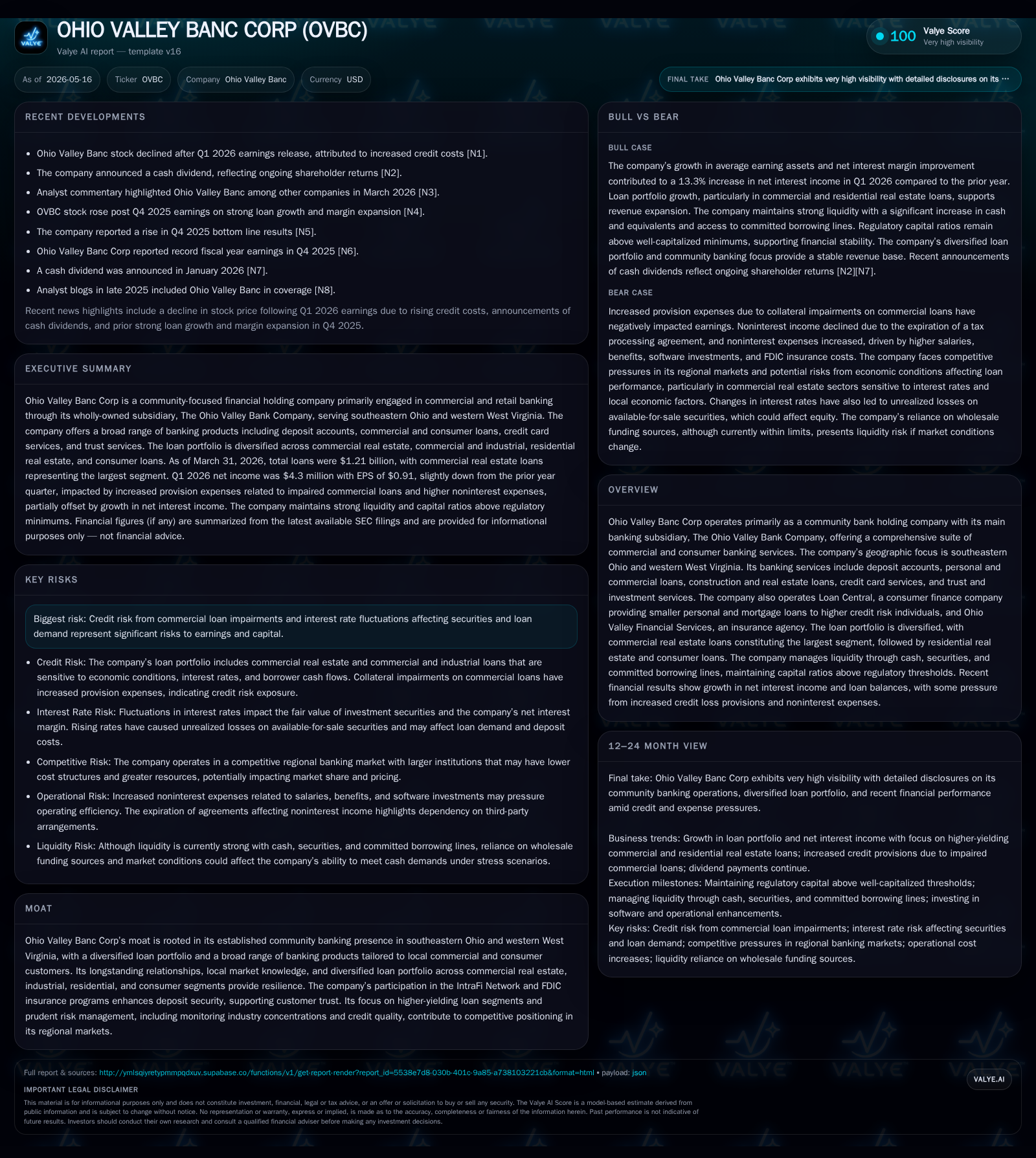

In its latest quarterly filing for Q1 2026, Ohio Valley Banc Corp reported a slight decrease in net income driven largely by increased credit costs linked to collateral impairments in commercial loans. Noninterest income declined, while operating expenses rose, reflecting pressures on profitability. Concurrently, the company announced a significant leadership transition with the appointment of Ryan J. Jones as President, succeeding Larry E. Miller II, aiming to steer strategic growth in its southeastern Ohio and western West Virginia footprint. Ohio Valley Banc Corp maintains a diversified loan portfolio across commercial real estate, residential real estate, and consumer segments, leveraging long-standing community ties and a wide range of banking products tailored to its regional customers.

Recent Operating Update: Q1 2026 Earnings Reflect Rising Credit Costs and Leadership Transition

Ohio Valley Banc Corp’s first quarter results filed on May 15, 2026 ([S2]) indicate a small year-over-year dip in net income to $4.3 million, or $0.91 earnings per share, compared to $0.94 per share in Q1 2025. Return measures also softened, with return on assets declining by 12 basis points to 1.08% and return on equity dropping by 165 basis points to 10.17%. The primary headwind cited was an elevated provision expense increase of approximately $1.2 million tied to collateral impairments on two commercial loan accounts, underscoring sector-specific credit risks within their lending portfolio.

Noninterest income contracted by $358 thousand mainly due to reduced electronic refund check handling and deposit fee revenue—reflecting subtle shifts in customer transactional behavior or competitive pressure on fee structures. Meanwhile, higher staffing costs, technology expenses, or other operational factors pushed noninterest expenses up by around $483 thousand.

An event filing on the same date ([S3]) highlighted a key leadership development wherein Ryan J. Jones was named President of both Ohio Valley Banc Corp and The Ohio Valley Bank Company, filling a vacancy left by Larry E. Miller II who remains CEO. This directorial succession reflects governance adaptation with potential implications for strategic execution going forward.

Business Model: Community-Focused Banking with Diversified Financial Services

Ohio Valley Banc operates principally as a community bank holding company focused geographically on southeastern Ohio alongside adjacent western West Virginia markets ([S1], Valye Report). Its core banking subsidiary offers comprehensive commercial and consumer services — including deposit accounts (checking savings/time), personal/commercial loans, construction financing, real estate loans across various categories, credit card services, IRA products, safe deposit facilities, wire transfers, and tax-related short-term loans co-originated with Loan Central.

Loan Central extends access to smaller-scale personal loans and mortgages targeting borrowers considered higher credit risks than typical bank clientele — an important complementary business aimed at broadening reach within the retail consumer segment while managing risk through focused underwriting standards separated from core banking.

The company’s operational model also includes Ohio Valley Financial Services Agency providing insurance products designed to generate fee income streams beyond traditional interest margins. These multiple revenue layers enhance the overall business resilience.

The loan book is notably diversified: commercial real estate loans comprise the largest portion followed by residential real estate loans; the consumer portfolio includes home equity lines of credit and automobile loans among others ([S1]). This spread mitigates concentration risk but requires vigilant performance monitoring especially in commercial credits sensitive to local economic cycles.

Industry Structure and Competitive Position

Operating as a regional community bank amidst numerous peers servicing similar demographic footprints implies inherently intense competition for deposits and quality loan opportunities. However, Ohio Valley Banc’s longstanding presence enhances its moat via strong local brand recognition and relationship banking strengths supported by deep knowledge of its regional economy.

Its participation in programs like the IntraFi Network furthers depositor confidence by augmenting FDIC insurance coverage across high deposit balances — critical given competitive pressures on pricing and customer retention strategies. The company's balanced product offering across retail banking, lending sectors, trust services, and ancillary insurance products situates it well within the local ecosystem.

Nonetheless, challenges arise from larger national or regional banks capable of leveraging scale advantages or technology investments that may appeal increasingly to younger demographics or digitally oriented consumers—areas where smaller banks often face infrastructural constraints.

Growth Drivers

Key growth avenues are multifaceted:

- Commercial Lending Expansion: Leveraging localized industry relationships enables originations particularly within the commercial real estate segment where knowledge of property markets is advantageous.

- Consumer Loan Penetration: Through Loan Central’s focus on higher-risk personal lending segments including tax advance products linked closely with seasonal demand patterns.

- Fee Income Diversification: Enhancing trust services and insurance offerings broadens fee-generating capabilities independent of interest rate fluctuations.

- Deposit Base Stability: Maintained via trusted brand reputation allied with expanded insurance network participation fostering customer retention even during economic volatility.

These drivers align structurally with observed market trends favoring relationship-driven banking and moderately sized institutions catering effectively to underserved niches while maintaining lean cost structures relative to large-scale competitors.

Risks and Constraints

Credit risk continues as a prominent concern highlighted explicitly by recent increases in provisions ([S2]). Impairment in commercial loans signals vulnerability to localized economic downturns or misalignment with borrower profiles—demanding continuing emphasis on conservative underwriting practices.

Interest rate environment fluctuations pose dual pressures: rising rates can erode fixed-rate loan demand but improve net interest margins; conversely low or falling rates pressure yields but stimulate borrowing volumes. Balancing this dynamic influences future earnings stability.

Regulatory compliance costs represent ongoing overhead burdens particularly for smaller banks striving to meet evolving mandates without scale economies available to national institutions ([S1]). Capacity constraints limiting geographic expansion challenge faster growth ambitions given entrenched competition.

Technology adoption challenges also exist; updating digital platforms is critical for customer engagement yet costly relative to institution size—a perennial tension impacting long-term competitiveness.

What To Watch Next

Following completion of Q1 results and leadership changes ([S2], [S3]), investor attention should focus on:

- Progress on credit remediation efforts concerning impaired commercial relationships.

- Trends in noninterest income rebounding or stabilizing as fee-based revenue sources adapt post-pandemic behavioral shifts.

- Execution under newly appointed President Ryan J. Jones encompassing strategy refinement or expansion plans.

- Quarterly updates on loan portfolio composition shifts or new product initiatives launched via Loan Central or Insurance divisions.

- Deposit growth trajectory sustaining funding stability amid competition.

- Any incremental disclosures regarding regulatory developments affecting operational flexibility or capital allocation decisions.

Financial Profile: Stable Liquidity With Net Cash Positive Balance Sheet

Latest financial snapshot

| Metric | Value | Period |

|---|---|---|

| Cash & equivalents | $125mm | |

| 2026-03-31 | ||

| Total debt | $24mm | |

| 2026-03-31 | ||

| Net debt | $-102mm | |

| 2026-03-31 |

Source: SEC companyfacts cache [F1].

Ohio Valley Banc maintained strong liquidity at the end of March 2026 with cash and cash equivalents totaling approximately $125 million against total debt near $23.7 million—resulting in net cash position around negative $101.6 million (net debt defined as total debt less cash) ([F1]). This conservatively leveraged posture provides ample buffer for absorbing credit volatility or funding organic expansion without immediate external financing needs.

Conclusion

Ohio Valley Banc Corp’s latest quarter embodies typical challenges facing small regional banks balancing credit risk management amid local economic cycles alongside sustaining diversified revenue streams across consumer lending, commercial banking, insurance agency operations, and trust services. Leadership renewal concurrent with continuing vigilance over impaired credits highlights management’s dual focus on stability preservation while positioning for measured growth within familiar geographic confines. The company’s durable ties within southeastern Ohio/western West Virginia markets combined with participation in broader deposit insurance frameworks underpin its competitive moat despite incremental financial pressures noted this quarter.

This analysis is based solely on publicly filed documents including the most recent quarterly (10-Q), annual (10-K), event (8-K) filings along with validated company facts as of May 16, 2026. It excludes any investment recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments