From Blank Check to Energy Player: Evaluating Pelican Acquisition Corp’s Path Through Business Combination

Pelican Acquisition Corp progressed from its 2025 IPO as a blank check company toward becoming Greenland Energy via a complex merger with energy targets, facing key execution and capital allocation challenges.

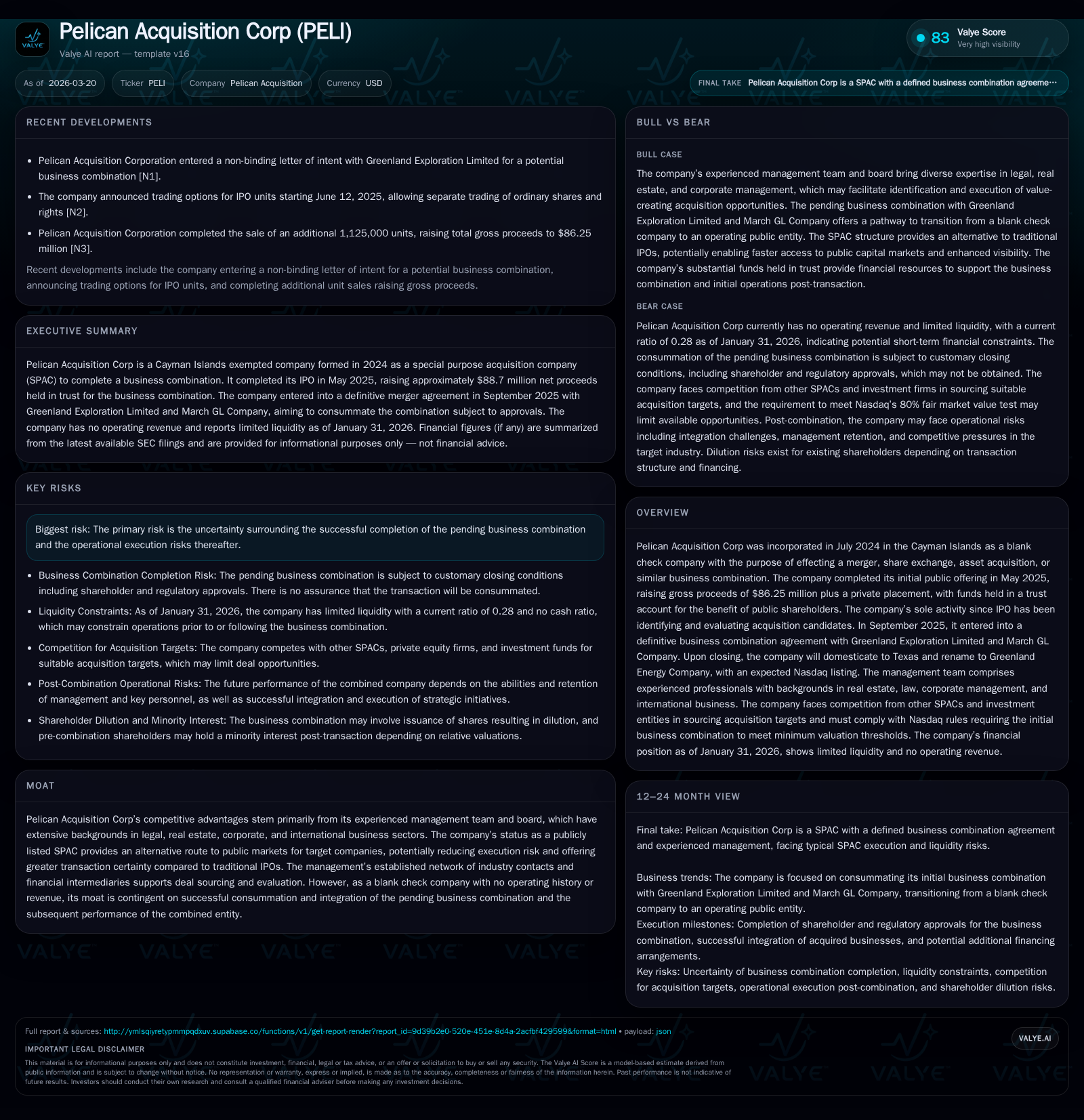

Founded in mid-2024 as a Cayman Islands-based SPAC, Pelican Acquisition Corp raised approximately $88.7 million in gross proceeds through its May 2025 IPO and private placement, held in trust pending business combination. The company is pursuing a transformational merger with Greenland Exploration Limited and March GL Company, which will domesticate the entity to Texas and rename it Greenland Energy Company. While Pelican has no operating history or revenue, its management team’s extensive experience and network underpin deal sourcing and evaluation capabilities. Execution risks remain elevated given SPAC structure and untested integration plans. Cash resources are primarily held in trust awaiting transaction closing, with founder shares providing nominal dilution. Future growth depends on scaling operations post-merger and accessing public capital markets.

IPO Launch and Initial Capital Structure Setup

Pelican Acquisition Corp commenced as a Cayman Islands exempted company in July 2024 specifically formed as a blank check company—or SPAC—to facilitate mergers or similar business combinations [S1]. The choice of the Cayman jurisdiction was motivated by tax neutrality benefits and administrative flexibility including ease of later redomiciliation [S1].

The Company successfully launched its initial public offering (IPO) on May 27, 2025, issuing 8,625,000 units priced at $10 each—this included an over-allotment exercise of 1,125,000 units—resulting in gross proceeds amounting to $86.25 million [S1][S4]. Each unit comprised one ordinary share plus one right which entitles the holder to fractional shares upon consummation of the initial business combination [S1]. Simultaneously, the Sponsor acquired 212,500 private units for $2.125 million under terms that restrict transferability [S1][S4].

Following deduction of underwriting discounts and offering expenses, the net proceeds totaling approximately $88.7 million were placed into a trust account intended to protect public investors until use towards consummating a qualifying business combination or returning capital upon liquidation [S4][S16]. This structure exemplifies common SPAC mechanics designed to enhance investor protections.

In August 2024 prior to the IPO, the Sponsor received 2,875,000 founder shares at an aggregate cost of just $25,000 — roughly $0.0087 per share — establishing a significant discount relative to the IPO unit price that dilutes post-merger economics for public shareholders if unmitigated [S1][S5].

Management Expertise and Strategic Deal Sourcing Capabilities

Leadership is concentrated within Robert L. Labbe who serves simultaneously as Chairman, CEO and CFO since inception; Labbe's extensive background over thirty years in real estate development finance and legal practice lends both industry insight and transactional acumen valuable in navigating complex acquisition deals [S7].

The board is comprised entirely of U.S. citizens including directors Daniel McCabe, Ping Zhang and Qi Gong who collectively augment governance with corporate management experience spanning international law and finance sectors [S7].

Management leverages an extensive network composed of private owners, private equity funds, family offices along with legal advisors and investment bankers across jurisdictions to identify acquisition opportunities aligned with targeted value creation parameters [S1][S6]. This breadth reduces deal sourcing risk inherent in SPAC models but cannot eliminate execution uncertainties inherent in definitive transaction agreements.

Financial Snapshot Prior to Business Combination

Operating solely as a blank check entity post-IPO involved zero revenue generation or substantive business activity beyond evaluating acquisition candidates; consequently Pelican’s financials reflect formation costs primarily driven by administrative overheads including advisory fees [F1][S7]. As reported for fiscal year ended January 31, 2026:

Historical performance (annual)

| FY |

|---|

| 2026 |

Source: SEC companyfacts cache [F1].

(Source: [F1])

Operating income sits near negative $1.1 million consistent with pre-revenue status; however net income registers positively at roughly $1.25 million indicating gains likely from non-operating items such as changes in fair value or interest income—typical for SPACs managing trust assets [F1]. The severely constrained current ratio (0.28) reflects limited available operating liquidity outside the trust account where most cash is sequestered until deal completion [F1]. The approximate return on equity measure is sharply negative at -308%, expected for an entity without ongoing profitable operations [F1].

Detailed Breakdown of the Greenland-March GL Business Combination

On September 9th, 2025 Pelican entered into a definitive Agreement and Plan of Merger with entities including Pelican Holdco Inc., Greenland Exploration Limited—an energy sector participant—and March GL Company—another complementary target firm—involving newly formed merger subsidiaries pooling these assets under one corporate roof post-closing [S1][S3][S19].

This transaction contemplates Pelican’s domestication relocation from Cayman Islands to Texas jurisdiction reflecting both tax optimization considerations historically favored by the Company’s incorporation decisions as well as strategic positioning linked to U.S.-centric operations of Greenland entities [S24][S1]. Post-merger branding will change the company name to Greenland Energy Company with anticipated Nasdaq listing continuation maintaining access to public equity markets aligned with institutional shareholder expectations [S3][S6].

The deal structure requires customary closing conditions such as shareholder approval—which typically involves redemption voting processes—and regulatory consents typical within energy sector consolidations though specifics remain undisclosed pending filing updates [S26][S17]. Cash financing arrangements rely heavily on existing trust account funds complemented potentially by additional equity or debt capital raises subject to market conditions proximate to closing date [S9][S29].

Anticipated Growth Trajectory and Market Position Post-Merger

Explicit forward-looking guidance was not made publicly available in current SEC filings; however management detailed qualitative criteria informing target selection that implicitly outline envisioned growth drivers including:

- Identification of targets demonstrating scalable revenue streams capable of producing sustainable free cash flow enabling reinvestment opportunities or deleveraging post-transaction;

- Ability for combined enterprise to benefit from enhanced visibility via public market listing potentially improving financing flexibility;

- Operational synergies derived from integrating complementary energy businesses providing scale economies or expanded market access [S6].

Given these parameters Pelican aims for non-dilutive growth fueled by organic expansion supplemented by opportunistic acquisitions enabled through its new public shell vehicle status—a common vector for post-SPAC success cases—but ultimately dependent on macro-economic energy market dynamics alongside competitively challenged industry factors common within exploration/drilling segments prevalent among Greenland Exploration’s profile.

Capital Allocation Approach, Liquidity Status, and Return Metrics

Pelican emphasizes retention of all available funds including future earnings after completing the initial business combination aimed at funding operational growth rather than paying dividends—in line with growth-stage priorities precluding cash distributions absent sustained profits or mature cash flows [S5][S6]. Founder shares representing approximately $25K aggregate cost acquired pre-IPO provide substantial theoretical dilution relative to public shares priced at $10 each; however sponsors have agreed to waive their redemption rights reducing direct share count pressure during redemption events but not eliminating overall ownership dilution risk following deal completion [S12][S13].

No share repurchase program exists reflecting limited capital utilization options during pre-operating phases while trust account cash continues securing public shareholder investments pending merger closure [F1][S14]. Cash flow projections remain undeclared due to nascent operations but expected evolution will involve converting trust assets plus any additional financing into productive capital expenditures defining future free cash flows.

Negative ROE approximates -308% highlighting early-stage losses relative to equity base earned during formation activities rather than operational profit generation—the standard pattern for SPACs transitioning into operating businesses only upon combination consummation [F1].

Regulatory and Operational Risks Surrounding Upcoming Transition

Main disclosed risks focus on:

- Completion uncertainty around the definitive business combination tied inherently to shareholder voting results plus customary regulatory approvals applicable principally within energy sector consolidations governed by federal/state agencies plus Nasdaq standards;

- Operational execution risks related to integration complexity across different corporate cultures or geographic footprints given new Texas domicile incorporating foreign-exempted Cayman entities;

- Lack of diversification post-merger concentrating revenues in limited number of energy-related products/services potentially subjecting company performance sensitivity to industry volatility or regulatory shifts affecting exploration/extraction activities;

- Potential management turnover ambiguity given no assurances provided regarding continuation/withdrawal of current leadership roles post-combination impacting ongoing value creation continuity;

- Absence of material litigation or known adverse legal proceedings currently offers moderate legal risk profile but cannot preclude latent contingent claims typical in carve-out mergers within commodity sectors requiring careful due diligence follow-up.

What Investors Should Monitor Ahead of Nasdaq Relisting

Investors focused on Pelican should track key milestones including:

- Outcomes from upcoming shareholder meetings voting on business combination approval which will set timing for transaction close or potential fallback scenarios;

- Satisfaction or waiver status concerning customary closing conditions especially regulatory clearances linked closely with domiciliary change oversight;

- Initial earnings announcements from Greenland Energy post-combination providing first operational transparency beyond pre-revenue reporting;

- Changes in liquidity profile representing movement of funds out of trust account into general corporate use impacting working capital adequacy;

- Governance transitions including board composition adjustments reflective of new entity identity under Texas law aimed at aligning strategic priorities with energy sector challenges.

Disclaimer: This analysis is based solely on publicly available regulatory filings as indicated by sources cited herein without making any predictions or recommendations related to security performance. No forward guidance beyond described facts should be construed as endorsement or financial advice.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments