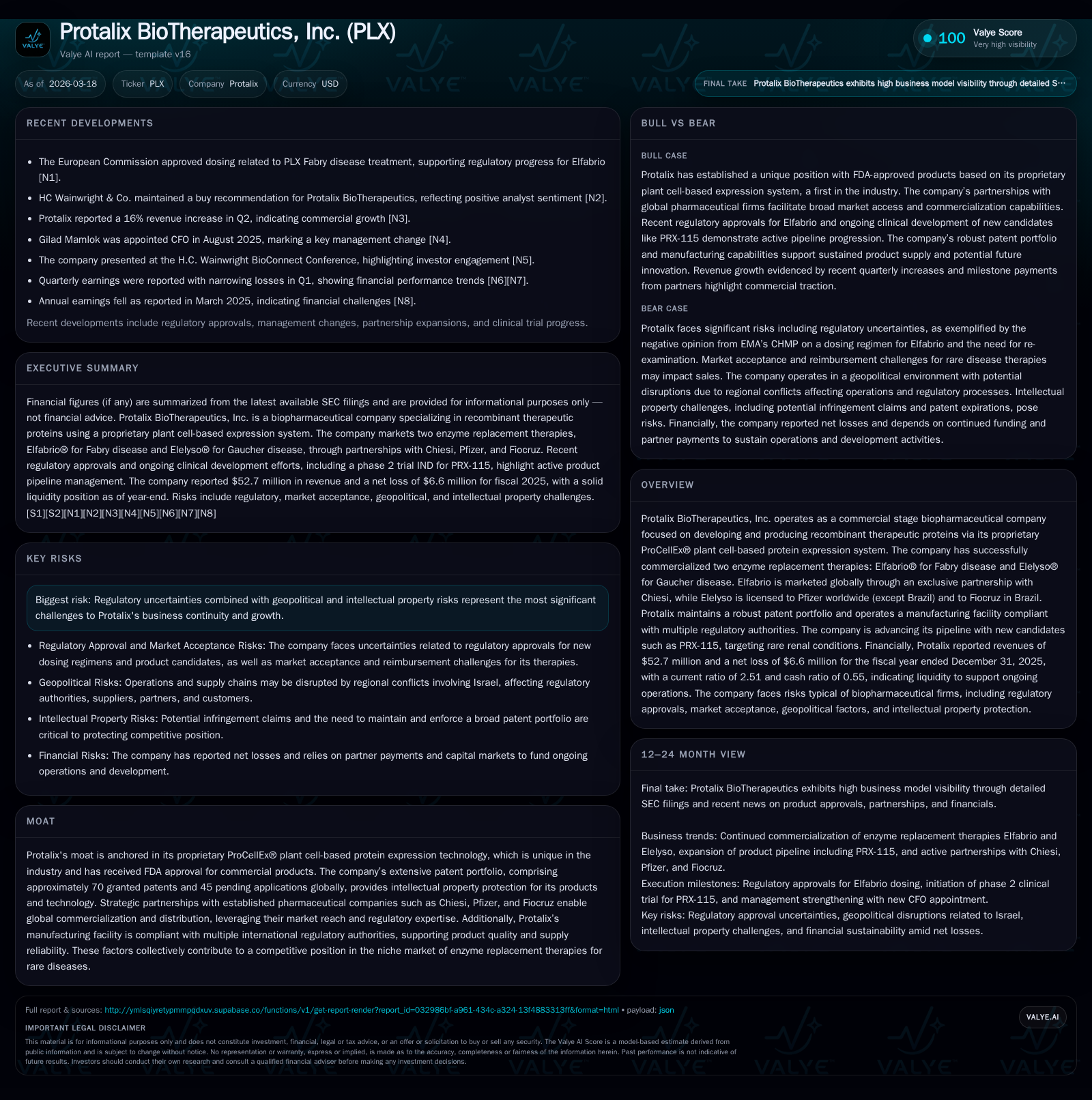

Protalix BioTherapeutics Confronts Profitability Challenges Despite Stable Enzyme Therapy Revenues

The company leverages proprietary plant-based protein technology and strategic partnerships while facing regulatory and operational headwinds.

Protalix BioTherapeutics, a commercial-stage biopharmaceutical firm specializing in plant cell-based recombinant protein therapies, reported a slight decline in revenue to $52.7 million in FY2025 along with a net loss of $6.6 million, reflecting increased costs and operating challenges. Its business centers on enzyme replacement therapies for rare diseases, marketed globally through key collaborations with Pfizer, Chiesi, and Fiocruz. Meanwhile, pipeline expansion efforts focus on rare kidney conditions with PRX-115 advancing into Phase 2 clinical trials. The company’s proprietary ProCellEx® platform and extensive patent portfolio underpin its competitive moat, but regulatory uncertainties and geopolitical risks in Israel remain notable threats to near-term growth and operational stability.

Company Background and Core Technology

Protalix BioTherapeutics operates as a commercial-stage biopharmaceutical company pioneering recombinant therapeutic proteins produced through its proprietary ProCellEx® plant cell-based expression system [S25]. Notably first to receive FDA approval of a plant cell-produced protein for commercial use, the company has established a foothold in rare disease enzyme replacement therapies (ERTs), focusing on Fabry disease and Gaucher disease treatments.

Elfabrio® (pegunigalsidase alfa) is approved for adult patients with Fabry disease and marketed globally via an exclusive partnership with Chiesi Farmaceutici S.p.A., while Elelyso® (taliglucerase alfa), licensed worldwide except Brazil to Pfizer and licensed separately in Brazil to Fiocruz, treats Gaucher disease [S25]. This collaborative model permits leveraging of global distribution networks and regulatory expertise.

The company maintains manufacturing operations compliant with multiple regulatory authorities to support commercial supply stability [S25]. Intellectual property is fortified with approximately 70 granted patents across key jurisdictions and around 45 pending applications protecting technologies, product candidates, manufacturing processes, and methods of use [S9].

Historical Financial Performance

Protalix’s financial trajectory over the last four fiscal years illustrates volatility typical of small biopharma firms transitioning from development to commercialization:

Historical performance (annual)

| FY | Rev ($mm) | Net ($mm) | CFO ($mm) | OpInc ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 53 | -7 | -12 | -5 | -1.2% | -325.2% |

| 2024 | 53 | 3 | 9 | 4 | -18.5% | -64.7% |

| 2023 | 65 | 8 | -1 | 10 | +37.5% | +155.7% |

| 2022 | 48 | -15 | -25 | -13 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2025 | -14 | -13.7 |

| 2024 | 7 | 6.8 |

| 2023 | -2 | 24.8 |

| 2022 | -26 | 140.3 |

Source: SEC companyfacts cache [F1].

Revenues declined modestly by approximately 1.2% between FY2024 and FY2025 after rebounding strongly from prior lower levels [F1]. Despite stable top-line figures recently, profitability eroded significantly due to higher operating expenses leading to an operating loss of $5.5 million compared with an operating profit previously [F1]. Net income correspondingly deteriorated.

Operating cash flow turned sharply negative again at nearly $12 million in FY2025 following positive inflows the prior year reflecting investments ramping up amid commercialization efforts [F1]. Capital expenditures rose nearly 28%, signaling increased spending on manufacturing capacity or technological upgrades.

Equity grew steadily reaching about $48 million at end-2025 from negative territory in early years, supported by equity financing activities including stock sales [F1][S6][S11]. No dividends or share repurchases have been reported.

Growth Drivers and Pipeline Development

While current revenues are anchored by two established ERTs—Elelyso® and Elfabrio®—future growth hinges on advancing clinical stage assets such as PRX-115 (PEGylated uricase). This candidate addresses uncontrolled gout as well as rare renal conditions, areas of significant unmet medical need where safety concerns dictate cautious therapy adoption [S25]. Clinical progress accelerated recently with FDA clearance of an Investigational New Drug application in October 2025 enabling initiation of Phase 2 trials [S10].

Additional pipeline pursuits include PRX-119 (Long Acting DNase I), targeting neutrophil extracellular traps-related diseases, alongside preclinical programs leveraging small molecules and antibodies combined with PEGylation technology [S25].

Commercial scaling relies heavily on effective collaboration execution with partners: Chiesi manages Elfabrio commercialization internationally; Pfizer oversees Elelyso outside Brazil; Fiocruz covers Brazilian markets [S1][S25]. These partnerships extend into fill/finish agreements optimizing supply chain logistics [S9].

A regulatory hurdle arose when the European Medicines Agency's Committee for Medicinal Products for Human Use issued a negative opinion on a proposed dosing regimen change for Elfabrio (2 mg/kg every four weeks) during late 2025; Protalix has requested re-examination jointly with Chiesi [S10][N1]. Outcomes could influence market access or prescribing conventions.

Risks Impacting Operations and Market Position

Key risk considerations include:

- Regulatory Uncertainties: Approval processes remain complex; adverse decisions or delays such as EMA's negative opinion can impact access [S4][S8][S20].

- Geopolitical Environment: Headquartered in Israel exposes operations to regional geopolitical tensions involving Hamas, Hezbollah, Iran among others that could disrupt supply chains or partner activities despite contingency plans [S6][S7][S16].

- Partner Dependence: Reliance on third parties for manufacturing fill/finish services (notably Chiesi), distribution (Pfizer & Fiocruz), and clinical trial conduct adds operational risk if agreements falter or compliance issues arise [S4][S10][S15].

- Competitive Landscape: Emerging alternative therapies may challenge market share if they demonstrate superior efficacy or safety profiles.

- Intellectual Property Challenges: Maintaining broad patent protection globally is critical but litigation risk exists over infringement claims either as plaintiff or defendant [S9][S10].

Capital Allocation and Financial Stability

At fiscal year-end 2025, Protalix held cash and equivalents of approximately $14.7 million against current liabilities of about $26.5 million, yielding a current ratio above two times which suggests reasonable short-term liquidity coverage [F1]. Equity financing during the trailing twelve months ending September 30, 2025 included gross proceeds near $7 million from common stock sales plus proceeds from warrant exercises; convertible notes matured fully before January 2024 reducing debt obligations [S6][S11][S13][F1].

Despite these capital inflows supporting near-term operating needs per management commentary, ongoing net losses coupled with negative operating cash flows underscore the necessity for sustained financing or operational breakeven achievement for long-term viability [F1][S12][S21]. Research & development continues as a significant expenditure area.

Outlook: Key Milestones to Monitor

Investors should track:

- Updates on PRX-115 Phase 2 trial progress including enrollment rates, safety outcomes, interim efficacy data.

- Regulatory developments concerning Elfabrio dosing regimen at EMA following re-examination request.

- Sales performance updates from partners reflecting geographic demand trends.

- Cash flow dynamics relative to new capital raises or cost management initiatives.

- Geopolitical developments affecting operational stability or partner functions.

Conclusion

Protalix BioTherapeutics distinguishes itself through its innovative plant-cell expression platform validated by FDA approval—a competitive moat difficult to replicate given technical manufacturing complexities inherent in plant-based biologics [S25][S9]. Mature enzyme replacement therapies provide stable revenue while pipeline candidates like PRX-115 offer potential expansion into additional rare disease markets including renal conditions where options are limited.

However, profitability setbacks in FY2025 highlight persistent cost structure challenges amid heightened R&D investment and regulatory hurdles compounded by external geopolitical risks that could impair momentum if escalations occur unexpectedly [F1][S6][S7][S16]. Dependence on partner collaborations introduces both strategic leverage and operational vulnerabilities common to small biotech firms.

Stakeholders should closely monitor clinical program advances alongside evolving regulatory landscapes which will critically shape Protalix's prospects for scaling growth beyond existing niche franchises while maintaining financial health under constrained cash reserves.

Disclaimer: This report synthesizes publicly available information without offering investment advice or recommendations. It reflects data as of March 18, 2026 based on company filings and credible news sources without speculative extrapolations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments