Quantum Genesis AI’s Transition from Development to Biocatalyst Licensing Faces Capital and IP Constraints

Quantum Genesis AI Corp. advances enzyme engineering for pharmaceutical APIs but faces challenges in revenue generation, patent protection, and manufacturing scale-up.

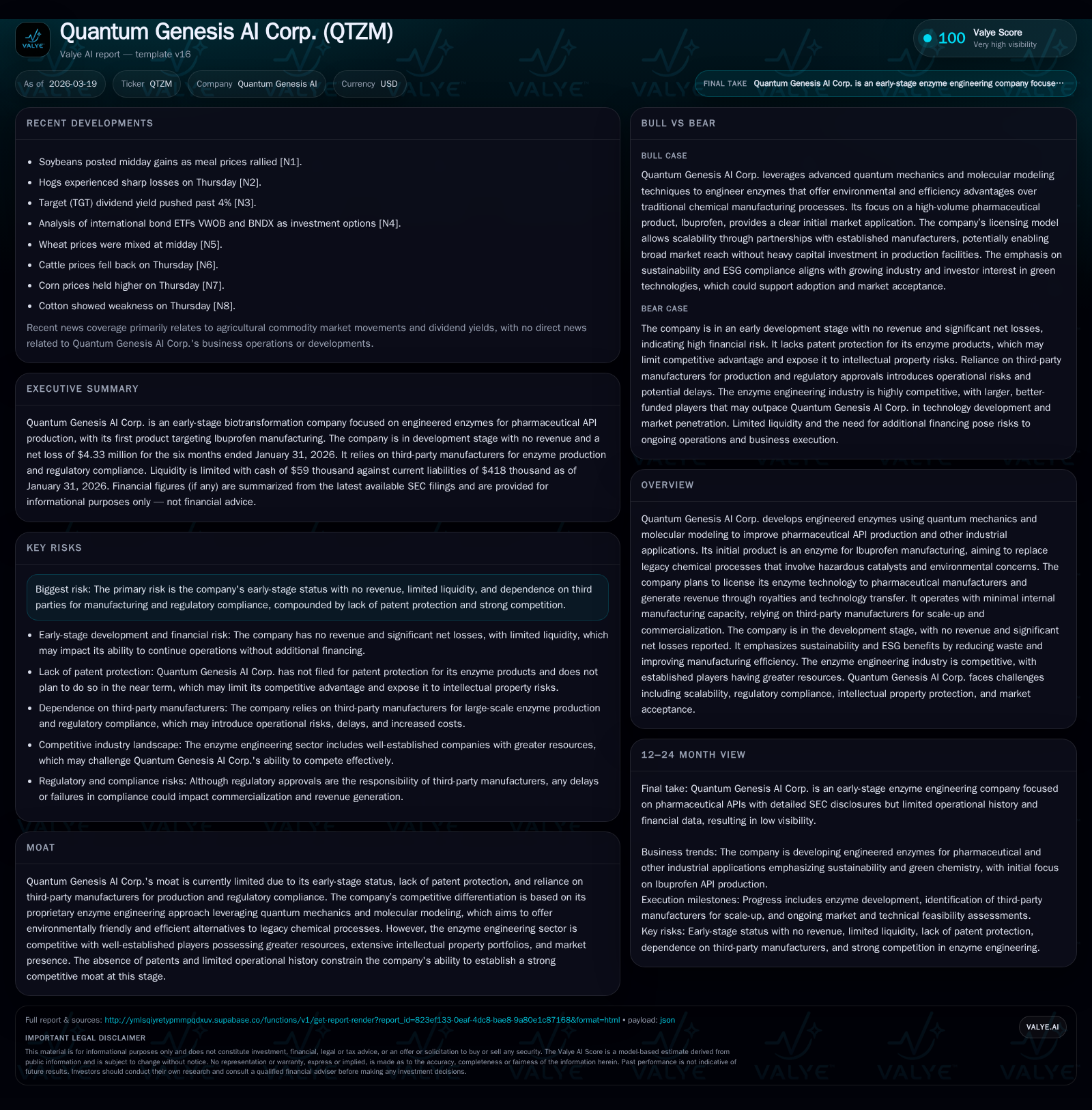

Quantum Genesis AI (QTZM) is an early-stage biotechnology company developing engineered enzymes leveraging quantum mechanics for pharmaceutical API production, initially targeting Ibuprofen manufacturing. Despite promising technology with sustainability benefits, the company has yet to generate revenue and relies heavily on third-party manufacturers amid limited liquidity and a lack of patent protections. Going forward, its growth hinges on establishing strategic partnerships, scaling production, and successfully navigating competitive and IP risks.

Company Overview and Business Model

Quantum Genesis AI Corp., formerly Quantumzyme Corp., is a development-stage biotransformation company focused on engineered enzymes to advance green chemistry in pharmaceutical manufacturing. Using proprietary approaches grounded in quantum mechanics and molecular modeling, the company targets improvements in enzyme activity, selectivity, and specificity applicable initially to active pharmaceutical ingredients (API), with its first commercial focus being the manufacture of Ibuprofen. Unlike traditional chemical synthesis that relies on hazardous catalysts under high temperature and pressure conditions, QTZM promotes enzyme catalysis at milder conditions that promise sustainability benefits including reduced waste generation and lower environmental footprint [S1][S27].

The company operates primarily as an intellectual property licensing business; it designs enzymes but outsources large-scale manufacturing to third-party contract manufacturers due to the absence of internal production facilities [S11][S27]. This trend aligns with broader industry practices where firms specializing in enzyme engineering often rely on external fermentation and process scale-up partners.

Historical Performance

QTZM remains pre-revenue with no product sales reported through the latest fiscal period ending July 31, 2025 [F1]. The company has sustained net losses each year since inception with -$199K net income loss recorded for FY2025 compared with smaller prior-year losses. Operating cash flows also remain negative at approximately -$125K for FY2025 signaling ongoing cash burn associated with R&D activities without offsetting operating inflows [F1].

Equity has turned negative in aggregate reflecting accumulated deficit growth, standing at roughly -$441K by mid-2025 [F1]. The balance sheet liquidity position is minimal: by January 2026 cash & equivalents held was a nominal $59 versus current liabilities exceeding $418K—resulting in an effectively zero current ratio [F1]. This underscores significant near-term financing risk that the company must manage.

Historical performance (annual)

| FY | Rev ($) | Net ($) | CFO ($) | Rev YoY | Net YoY |

|---|---|---|---|---|---|

| 2025 | 0 | -199269 | -125181 | ||

| 2018 | 93550 | -28167 | -2744 | -27.0% | +14.3% |

| 2017 | 128147 | -32858 | -37077 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | ROE% |

|---|---|

| 2025 | 45.2 |

| 2018 | 330.4 |

| 2017 | -183.1 |

Source: SEC companyfacts cache [F1].

Revenue dropped off completely from some early sporadic sales reported years ago indicating abandonment of prior product lines or shifts toward longer development horizons [F1]. There are no dividends or share repurchase programs reported; all available capital appears directed toward sustaining product development efforts [S26].

Growth Prospects

QTZM's future growth depends heavily on multiple interdependent factors:

- Commercialization of Engineered Enzymes: The focal point is licensing their Ibuprofen production enzyme to generic drug manufacturers—a sizable market given Ibuprofen’s status as one of the world’s highest-volume pharmaceuticals [S27]. Success would require demonstrating superior catalytic efficiency, cost-effectiveness, regulatory approval support, and clear environmental benefits relative to legacy chemical processes.

- Strategic Partnerships: Revenue generation will rely on forming alliances or licensing deals with pharmaceutical companies capable of adopting enzyme technologies commercially. No formal agreements or milestones have been publicly disclosed yet [S1][S27].

- Scale-Up Manufacturing: Dependence on contract manufacturers requires securing reliable partners able to produce enzymes at commercial scale without delays or quality issues—a known bottleneck risk area [S11][S25].

- Intellectual Property Strategy: Notably QTZM has not filed patents on its current lead product citing cost-benefit considerations instead favoring trade secret protection initially [S12]. This leaves the competitive moat vulnerable as rivals could potentially replicate or surpass their technology absent patent barriers.

- Expansion into Adjacent Markets: The firm indicates intent to extend enzyme applications beyond APIs into sectors like fragrances, flavors, sustainable materials, plastic degradation, and carbon capture technology—each carrying distinct technical challenges but enhancing long-term addressable market size [S1][S27].

Risks include stiff competition from entrenched players with substantial R&D budgets and existing IP portfolios as well as potential regulatory hurdles unique to genetically engineered components used industrially [S24][S28].

Forecasts / Milestones / Expectations

Currently there is no explicit financial guidance or publicly announced milestones regarding timing for first revenues or partnership agreements disclosed by QTZM [N#][S2]. The company intends to continue iterative validation phases typical of enzyme product development—enzyme discovery, lab validation of wild type followed by engineering modifications and scale-up testing—but lacks definite timelines beyond these process descriptions [S27].

Key developments to watch:

- Securing binding scale-up contracts with third-party manufacturers,

- Entering exclusive licensing arrangements or strategic collaborations with pharmaceutical API producers,

- Regulatory clearances related to biocatalyst use in drug production,

- Potential patent applications or other IP strengthening measures.

Until any of these materialize visibly QTZM remains reliant on investor patience amidst continued losses.

Returns / Capital Allocation

With no revenues generated there are no returns metrics such as ROE directly interpretable outside the historical loss context. Approximate ROE calculated from FY2025 data yields a positive figure around 45% due solely to negative equity creating a mathematical artifact rather than operational profitability [F1]. Thus it should not be read as meaningful performance indicator.

Operating cash flow trends display steep negative outflows consistent with investment-phase spending centered around R&D implementation rather than capital return to shareholders [F1]. No dividends or stock buyback programs have been undertaken reaffirming reinvestment priority.

The capital structure includes a history of equity issuance concentrated among founders including CEO Mr. Naveen Kulkarni who also serves as sole employee managing core operations—reflecting founder control but exposing execution risk tied closely to individual capacity [S29][S14]. The firm has identified need for further capital infusion within next twelve months given working capital deficits raising liquidity concerns unless addressed through new financing or revenue realization pathways [S9][S20].

Industry Context Analysis (labeled analysis)

Enzyme engineering for industrial biotransformation aligns with global green chemistry trends aiming at reduced reliance on toxic catalysts traditionally used at high temperatures/pressures. Pharmaceutical APIs remain one of the largest application segments due to strict purity standards, high volumes, and cost pressures motivating process innovation.

Notably, advances in computational modeling—particularly incorporating quantum mechanical calculations—have become increasingly important for rational design of more efficient enzymes tailored precisely for targeted substrate conversions. This distinguishes QTZM's approach albeit competitors also invest heavily in integrating AI-driven molecular simulation techniques.

Challenges common across the sector include scaling lab discoveries economically; ensuring robust enzyme stability during prolonged manufacturing runs; navigating complex regulatory environments; protecting valuable IP given fast-paced innovation cycles; plus building customer confidence in switching from incumbent chemical processes.

Competitive Positioning & Moat Considerations

QTZM’s core moat proposition rests upon combining quantum mechanics-based molecular modeling within their enzyme engineering workflow potentially enabling more precise catalyst design than standard directed evolution methods alone. However:

- Absence of patent filings leaves IP vulnerable;

- Heavy dependence on third-party contract manufacturers introduces supply chain risk;

- Minimal workforce size constrains operational agility;

- Market competition features dominant incumbents wielding extensive tech portfolios and deeper financial resources capable of faster scaling;

- Customer adoption cycles in pharma are lengthy due to validation requirements;

- ESG advantages provide differentiation but competitors also pursue sustainability initiatives vigorously.

Risks Summary (highlighted)

Major risks detailed in SEC filings include:

- Complete absence of revenue thus far accompanied by ongoing net losses threatening going concern assumptions without fresh capital raising or swift market traction;

- Limited human capital concentrated in single executive exposing leadership continuity risks;

- Reliance on non-binding arrangements for critical testing facilities potentially risking delays;

- Intense intellectual property threat landscape without currently filed patents increasing litigation vulnerability;

- Economic downturns impacting willingness by pharma customers to invest in process change;

- Regulatory complexities specific to genetically engineered enzymes applied in drug manufacturing pipelines;

- Risks inherent in reprisals from established producers launching competing technologies prematurely blocking market entry [S1][S4][S11][S24].

Conclusion (analysis)

Quantum Genesis AI represents a quintessential early-stage biotech innovator targeting a niche at the intersection of enzyme engineering and green chemistry transformation for pharmaceuticals. Its differentiated scientific foundation employing quantum mechanical design methodologies offers a plausible path toward novel biocatalysts that could disrupt traditional chemical synthesis routes.

However significant hurdles remain including urgent need for capital infusion beyond minimal cash reserves; establishment of durable commercial partnerships enabling royalty streams; enhancement of intellectual property protections; scaling reliable manufacturing through vetted external suppliers; expanding organizational capabilities beyond sole leadership; plus mitigating entrenched competitive threats.

Movements such as the recent corporate rebranding signal strategic intent toward refining identity possibly aligned with broader recognition of AI-driven innovation approaches—but execution risks typical of any emerging-growth biotech persist robustly. Stakeholders should monitor progress toward definitive licensing agreements, patent prosecution activity should it commence, improvements in liquidity ratios, and operational hires indicative of transition from pure R&D stage toward early commercialization phases.

This analysis is based exclusively on public SEC filings up through March 19, 2026 ([F1], [S1]-[S29]) and relevant market news context. It does not constitute investment advice or recommendations but aims to provide a rigorous overview synthesizing verifiable facts about Quantum Genesis AI Corp.’s business footing relative to industry dynamics and capital market realities.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments