Red Cat Holdings Navigates Revenue Challenges and Deepening Losses Amid Defense Drone Market Dynamics

Red Cat Holdings faces significant revenue contraction and growing net losses despite ongoing investments in advanced tactical unmanned systems for defense applications.

Red Cat Holdings Inc operates in the defense technology sector, focusing on tactical unmanned aerial and surface systems. The company has experienced a steep decline in revenue alongside escalating operating losses in recent years, influenced by competitive pressures and supply chain constraints. While Red Cat maintains strategic partnerships and a foothold in U.S. defense contracts, persistent financial deficits and regulatory complexities temper its near-term outlook.

Business Overview

Red Cat Holdings Inc specializes in advanced unmanned systems primarily designed for defense and national security applications. Its product portfolio includes small tactical drones such as Black Widow™, Teal 2, FANG™ FPV drones, VTOL fixed-wing Edge 130 drones, and unmanned surface vessels developed through the Blue Ops division. These platforms enhance multi-domain military operations across air, land, and sea environments by integrating proven hardware and software solutions. The company emphasizes rapid adaptation of existing technologies combined with strategic partnerships to meet evolving battlefield needs [S1].

Historical Financial Performance

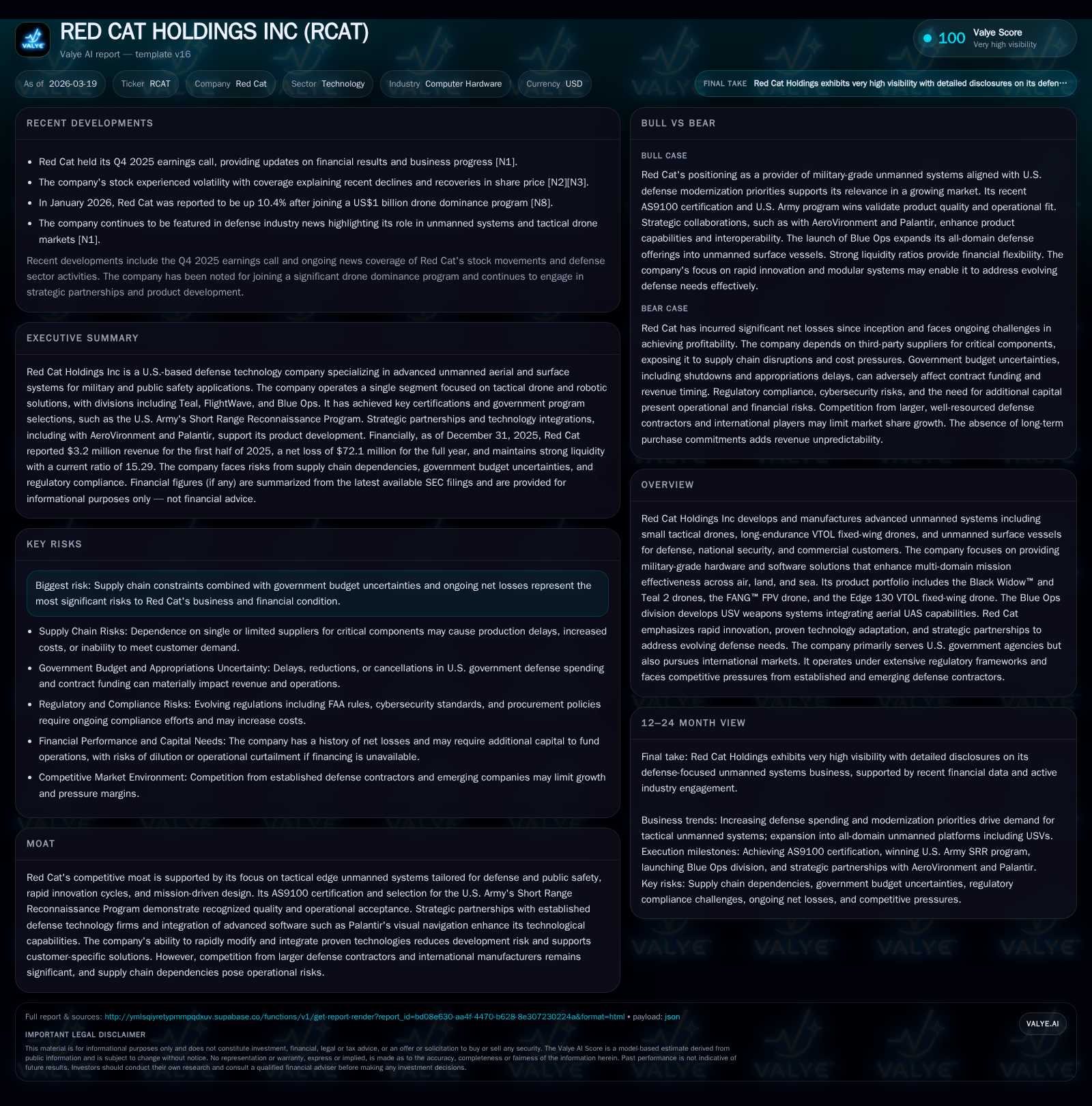

Red Cat’s revenue has exhibited notable volatility over recent fiscal years. Revenue peaked at approximately $9.9 million for the fiscal year ending April 2023 but then contracted sharply to about $4.9 million by December 2024 — a decline exceeding 50% year-over-year [F1]. This reflects challenges related to scaling sales volumes during competitive pressures.

Operating income deteriorated significantly from a loss of roughly $25.8 million in 2024 to nearly $66.6 million negative in 2025 — more than doubling operating losses [F1]. Net income losses deepened from -$43.6 million to approximately -$72.1 million over the same period. These trends indicate increasing operational expenditures relative to declining revenues.

Operating cash flow remains negative; for example, fiscal year 2023 reported a deficit near $29.2 million, highlighting ongoing cash burn despite sustained research and development efforts [F1]. The balance sheet reveals a strong current ratio of about 15x at the end of 2025, suggesting ample short-term liquidity predominantly supported by equity capital raises rather than operating cash generation [F1].

Historical performance (annual)

| FY | Rev ($mm) | Net ($mm) | CFO ($mm) | OpInc ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | -72 | -67 | -65.3% | |||

| 2024 | 5 | -44 | -26 | -51.1% | -61.0% | |

| 2023 | 10 | -27 | -29 | +54.2% | -131.7% | |

| 2022 | 6 | -12 | -16 | +28.6% |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | ROE% |

|---|---|

| 2025 | -29.3 |

| 2024 | -87.0 |

| 2023 | -49.6 |

| 2022 | -15.0 |

Source: SEC companyfacts cache [F1].

Note: Some financial metrics are not available uniformly across all years.

Drivers Behind Past Performance

Revenue volatility is linked to the inherent uncertainty of government contracting where customers issue purchase orders without long-term commitments [S13]. Supply chain disruptions have compounded challenges due to sole-source suppliers for critical components facing shortages and escalating costs [S5][S8]. Margins are pressured by elevated expenses related to integrating emerging technologies such as autonomy suites and maintaining compliance with regulatory frameworks including FCC emissions standards and environmental laws like RoHS/WEEE directives [S9][S11].

Research & development investments are substantial—approaching $6 million annually excluding stock-based compensation—reflecting Red Cat's focus on maintaining technological leadership within the tactical UAV segment [S13][F1]. However technical challenges and lengthening product development cycles have constrained timely commercialization.

Competition intensifies from major defense contractors including Lockheed Martin and Northrop Grumman as well as specialized firms like AeroVironment. These competitors benefit from economies of scale and integrated solution ecosystems that reinforce their market positions despite Red Cat’s strategic contracts through U.S. Army programs [S21].

Future Growth Prospects

Growth opportunities center on rising demand for unmanned systems driven by modern battlefield requirements emphasizing force multiplication via AI-enabled autonomy and network-centric warfare capabilities. Red Cat’s strategy of rapid innovation tailored to mission-specific configurations positions it well for niche contract awards within U.S. defense agencies [S6]. Collaborations with technology partners such as Palantir enhance capabilities like visual navigation software essential for evolving military needs.

The company is pursuing international expansion targeting allied nations that prioritize domestically manufactured secure drone platforms amid geopolitical tensions; however regulatory complexities including export licensing under Export Administration Regulations impose constraints on speed-to-market abroad [S6][N1].

Risks include fluctuations in federal defense budgets subject to political cycles and potential delays or cancellations common in government procurement that could cap revenue growth unpredictably [S20]. Continued supply chain fragilities remain a concern given dependence on financially constrained suppliers unable to scale rapidly with demand surges [S5], alongside increasing cybersecurity certification requirements adding cost hurdles for contract eligibility [S22].

No explicit management guidance has been provided regarding revenue or profitability targets beyond ongoing R&D spending and scaling efforts noted during recent earnings discussions [N1]. Monitoring improvements in backlog visibility and contract wins will be critical indicators of future trajectory.

Returns and Capital Allocation

Red Cat Holdings has not achieved positive net income since inception; accumulated deficits approach $197 million as of fiscal year-end 2025 reflecting cumulative losses relative to equity capital infusion [F1][S1]. Approximate return on equity stands deeply negative at around -29%, consistent with ongoing unprofitability [F1]. Negative operating cash flows underscore reliance on external financing rather than internally generated funds.

The company does not pay dividends nor has it engaged in share repurchases historically—typical of growth-stage firms prioritizing capital deployment toward product development and working capital needs [F1][S13][S18]. Capital allocation emphasizes expanding domestic manufacturing capacity while maintaining compliance with quality certifications such as AS9100 critical for military-grade hardware acceptance [S21][S18].

Equity financing appears to be the primary liquidity source supporting operations given large positive equity balances contrasted against persistent operating losses; no notable debt usage is evident indicating conservative leverage consistent with early commercialization risk management [F1].

Industry Context Analysis (Non-Company Specific)

The unmanned systems sector is rapidly evolving fueled by advances in autonomous navigation sensors coupled with tightening defense modernization priorities globally focused on domain-integrated warfare capabilities. Small tactical drones offer cost-effective alternatives performing ISR (Intelligence Surveillance Reconnaissance) and electronic warfare support roles traditionally filled by manned or higher-cost assets.

Procurement trends increasingly emphasize cybersecurity-hardened domestic supply chains motivated by national security concerns amid heightened global tensions constraining foreign component sourcing within allied blocs.

Competitors with broader product portfolios integrating drone platforms into layered combat networks enjoy advantages including cross-selling after-market services that support lifecycle operating margins—areas where specialized firms like Red Cat face challenges.

Risks Summary

Key risks include:

- Continued net losses raising doubts about achieving sustainable profitability absent significant revenue growth or expense restructuring.

- Supply chain vulnerabilities impacting production timelines or component costs due to sole-source dependencies.

- Lengthy product development cycles vulnerable to technical setbacks delaying revenue recognition.

- Increasing regulatory complexity elevating compliance costs across emissions standards, cybersecurity frameworks, export controls, and environmental mandates.

- Customer concentration risk given predominant dependence on discretionary U.S. government appropriations subject to political variability [S19][S24].

- Potential intellectual property infringement claims or data protection failures imposing legal liabilities disrupting operations [S17].

- Intense competition from established aerospace & defense contractors limiting pricing power adversely affecting margins.

Conclusion

Red Cat Holdings remains a technologically relevant participant within the tactical UAV domain serving critical military segments through nimble innovation and strategic alliances. However its financial profile evidences pronounced challenges stemming from shrinking revenues alongside mounting operating deficits aggravated by supply chain bottlenecks and regulatory compliance demands.

The company’s future depends on converting evolving defense priorities favoring affordable unmanned systems into firm order backlogs while managing costs toward breakeven operations. Close attention should be paid to contract award visibility improvements alongside supply chain resilience metrics and regulatory developments impacting manufacturing or international sales capabilities.

This analysis is based solely on disclosed financial data and documented company information without offering investment recommendations or price forecasts.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments