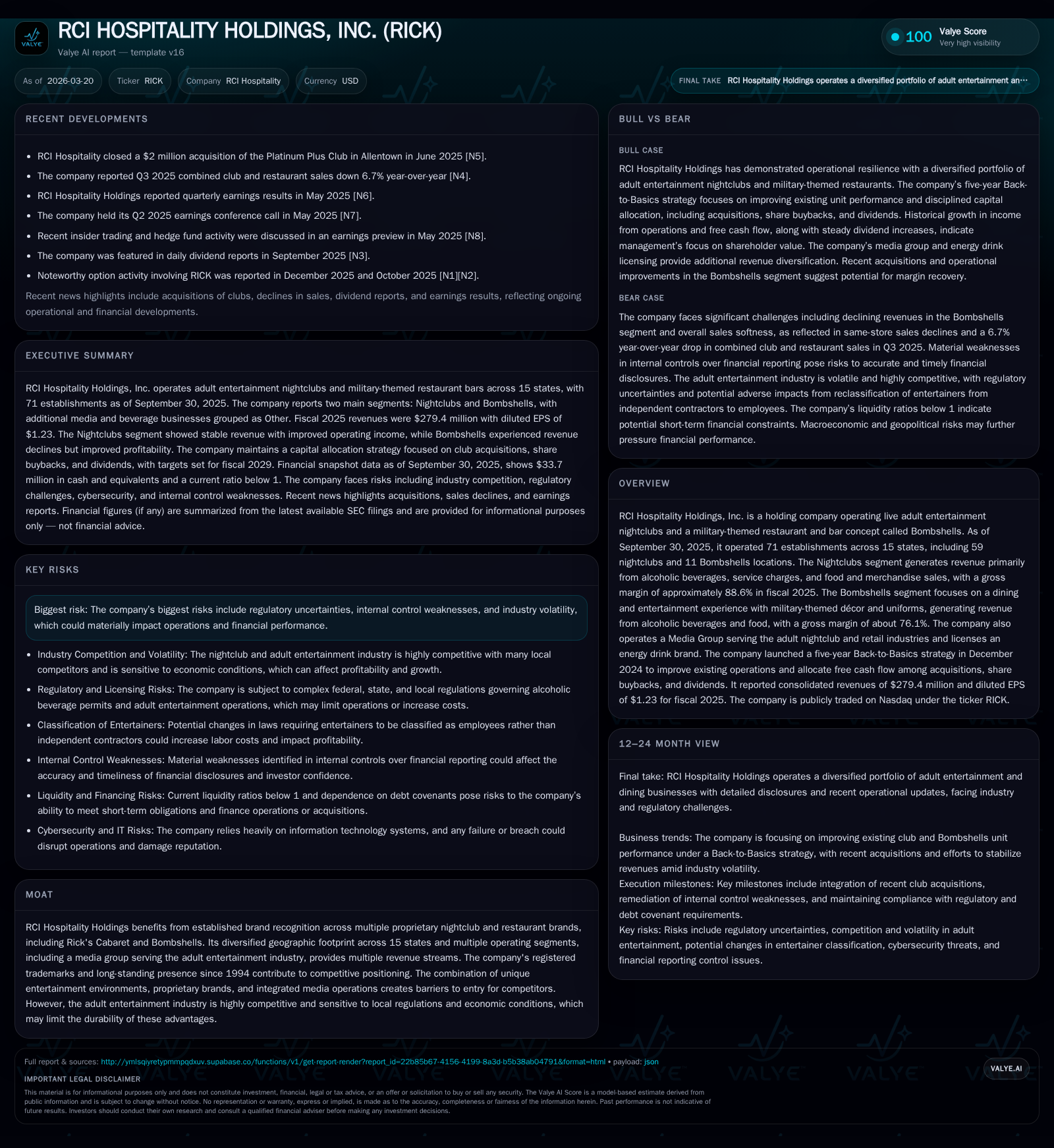

RCI Hospitality Holdings: Revenue Growth Challenges and Legal Headwinds Impact Profitability

RCI's fiscal 2025 results reveal divergent revenue growth and earnings pressures compounded by ongoing legal challenges and strategic recalibration.

RCI Hospitality Holdings reported an 18.7% revenue increase in fiscal 2025 driven partly by acquisitions, yet operating income swung to a loss of $0.5 million, reflecting significant expense impacts including legal contingencies. The company's Nightclubs segment remains its core revenue contributor with high gross margins, while the Bombshells restaurant chain faces same-store sales declines and strategic downsizing. Legal indictments concerning tax matters and regulatory scrutiny impose additional uncertainties. Despite solid operating cash flows and a positive free cash flow of over $9 million, material weaknesses in internal controls and insurance challenges persist. RCI is executing a five-year Back-to-Basics strategy aimed at stabilizing operations amid industry volatility and regulatory risk.

Historical Financial Performance: Revenue Trajectory vs Profitability Erosion

RCI Hospitality Holdings experienced a paradoxical fiscal year in 2025: while consolidating top-line strength with an 18.7% year-over-year revenue rise ($279.4 million) compared to the prior year [$F1], profitability metrics deteriorated markedly. Operating income flipped from a positive $3.5 million in FY2024 down to a loss of approximately $0.5 million in FY2025—a staggering downturn of roughly 115% [$F1]. Net income mirrored this pattern with losses expanding over twentyfold from a marginal profit of $0.24 million to a negative $5.5 million.

This divergence reflects higher operating expenses likely tied to ongoing legal matters—specifically the indictment disclosed in September 2025—and operational inefficiencies as the firm integrates recent acquisitions and navigates a complex industry backdrop [S1][S4]. Same-store sales trends indicate softness: Nightclubs posted -2.1% while Bombshells faced larger declines (-13.6%), intensifying pressure on core venues [S6][S9].

Operating cash flow (CFO) remained relatively resilient, contracting only about 11%, ending at roughly $49.4 million [$F1]. However, capital expenditure rose steeply (68%), reaching over $40 million as RCI invests in club refurbishments and targeted expansions [$F1]. This capex surge further strained earnings.

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|---|

| 2025 | -6 | 49 | -1 | -2354.9% | |

| 2024 | 0 | 56 | 4 | -88.9% | |

| 2023 | 2 | 59 | 6 | 40 | -79.4% |

| 2022 | 11 | 65 | 18 | 24 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($mm) | Buybacks ($mm) | FCF ($mm) |

|---|---|---|---|

| 2025 | 2 | 12 | |

| 2024 | 2 | 21 | |

| 2023 | 2 | 2 | 19 |

| 2022 | 2 | 15 | 41 |

Source: SEC companyfacts cache [F1].

Table summarizes recent years' financial results highlighting stark profitability contraction despite revenue gains.

Segment Analysis: Nightclubs, Bombshells, and Other Business Contributions

RCI's two primary reporting segments—Nightclubs and Bombshells—present contrasting operational dynamics [S6][S9].

The Nightclubs segment dominates revenues with adult entertainment venues such as Rick's Cabaret encompassing diverse brands targeting segmented demographics across multiple states (15 states; total of 59 clubs). In fiscal year 2025, its revenues slightly declined by approximately 0.6%, juxtaposed against an operating income increase of about 20%. This implies efficiency improvements or cost discipline within mature venues despite mixed same-store sales declining by ~2%. The segment's gross margin sits at an exceptional level of approximately 88.6%, typical for high-margin beverage/service-centric nightclub operations focusing heavily on alcohol sales (43%) and service fees (40%) [S6].

Conversely, the Bombshells segment—which operates military-themed restaurant-bars blending dining with entertainment—suffered a sizable revenue drop (-29%) paired with reduced losses turning into modest profitability ($177 thousand positive from a prior loss of $10 Million). The decline coincides with closing underperforming locations including three Texas units and one food hall in Denver, indicating operational pruning toward stabilizing this experiential hospitality concept amid challenging market conditions [S9]. Bombshells' lower gross margin (~76%) reflects food service industry norms compared to nightclubs.

The 'Other' reportable segment incorporates RCI's Media Group activities—industry trade publications, conventions (ED Expo), national awards programs—and Drink Robust energy drink licensing [S9], representing diversified but smaller-scale revenue contributors outside hospitality venues.

Together these segments demonstrate RCI’s strategic balance between high-margin nightlife entertainment and branded experiential dining concepts but highlight increased segmentation risk as Bombshells grapples with repositioning.

Legal Challenges and Regulatory Risks Weighing on Operational Stability

A defining overhang for RCI remains a high-profile legal indictment filed in September 2025 involving senior executives—including former CEO Eric Langan and CFO Bradley Chhay—and several subsidiaries based in New York alleging conspiracy, bribery, criminal tax fraud related to purported use of “Dance Dollars” promotional credits for illicit tax reductions [S4][S5]. These allegations are serious: they implicate corporate governance lapses that may lead to significant fines or sanctions if proven.

The Company maintains the presumption of innocence but acknowledges that lawsuits arising from such matters risk extensive defense costs along with potential reputational damage that may detract management focus from operations [S4]. The complexity escalates given historical insolvency of the previous liability insurer responsible for coverage until October 2013 leaving litigation funding risks on RCI for uncovered claims [S8].

Complementing this are operational regulatory risks pervasive in adult entertainment such as exposure under dram shop statutes which can hold venues liable for damages stemming from over-serving intoxicated patrons; these laws vary across U.S states where RCI functions [S7][S18]. Furthermore, evolving employment law rulings around classification of entertainers as independent contractors versus employees could materially affect cost structure.

Finally, compliance burdens escalate with cybersecurity risks highlighted due to dependence on information technology systems processing sensitive customer data via point-of-sale platforms—an area exposed to increasing cyberattack sophistication requiring ongoing investments [S21][S26].

Capital Management: Cash Flow Strength amid Divergent Net Income and Expense Profiles

Despite mounting net losses in fiscal 2025 ($-5.5 million), RCI reported robust operational cash generation at nearly $49.4 million resulting in positive free cash flow approximating $9 million after accounting for significant capital expenditure outlays totaling ~$40 million [$F1]. The capex jump (+68%) largely supports club acquisitions (Flight Club et al.) alongside renovations aligning with its Back-to-Basics growth strategy.

The company continues returning capital via dividends increasing modestly to $2.46 million (~8% growth YoY), while share repurchases declined from about $20 million to just under $12 million signaling more cautious buyback activity amid earnings volatility [$F1]. Equity remains solidly above $260 million providing some buffer against near-term income pressures; however, working capital tension is evident given current ratio below unity (approximate ratio at .81) stemming from elevated current liabilities compared with assets [$F1][S16][S23].

Return metrics like ROE eroded into negative territory (-2%), correlating with net losses [$F1]. This indicates room for improvement in translating cash flow strength into sustainable profitability.

The Five-Year Back-to-Basics Strategy: Growth Catalysts and Constraints

Initiated December 2024, RCI's five-year strategic framework focuses on reinforcing foundational club operations while managing growth prudently amidst inherent industry volatility [S1]. Specific endeavors include optimizing existing nightclub portfolios through selective acquisitions—as evidenced by clubs added during FY25—and streamlining Bombshells venues following weaker performance trends [N/A][S9].

However, constraints remain substantial due to regulatory headwinds including liquor license permits complexity varying by state jurisdictions; competitive intensity within cabaret markets; workforce availability challenges impacting service quality; plus persistent legal uncertainties [S13][S20]. The company has not issued detailed numeric targets or explicit forecasts linked directly to this plan within filings so far [N/A], making quarterly operating results updates crucial markers for progress.

Monitoring Industry-Specific Factors: Competition, Workforce, and Compliance

Adult entertainment venues face unique operational challenges: fierce local competition among both branded chains and independent clubs demands constant innovation backed by strong customer engagement programs measured often via same-store sales trends . Labor retention issues loom large due to the specialized skill sets required for managerial staff as well as entertainers treated as contractors emphasizing HR strategy importance [S22].

Compliance spans beyond liquor control regulations into public safety considerations like responsible alcohol service training programs mandated variably across jurisdictions crucial for dram shop liability protections; breaches here can result in outsized punitive damages claims substantially affecting reputation and finances [S7][S18]. Cybersecurity also presents an emerging frontier necessitating vigilance against pervasive financial data breach threats inherent in consumer-facing hospitality firms today .

All these factors collectively shape margin sustainability potential alongside expansion pathways.

Investor Considerations: What to Watch in Coming Quarters

While no formal guidance was provided explicitly for upcoming periods [N/A], investors should closely monitor developments including:

- Resolution or material progression in the New York indictments concerning executive officers which will influence risk assessment significantly;

- Stability or improvement in Nightclubs same-store sales indicating core venue health;

- Execution effectiveness of Back-to-Basics initiative visible through operational KPIs such as EBITDA margin recovery;

- Liquidity position dynamics especially around covenant compliance given debt obligations;

- Changes within senior leadership post-executive transitions signaled earlier in FY25;

- Management commentary during earnings calls describing mitigating actions addressing material weaknesses in internal controls highlighted previously.

In sum, RCI remains a complex operator balancing successful brand recognition against intensified legal/regulatory scrutiny within an economically sensitive segment requiring cautious evaluation going forward.

This report aims solely to inform on company fundamentals without providing investment advice or recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments