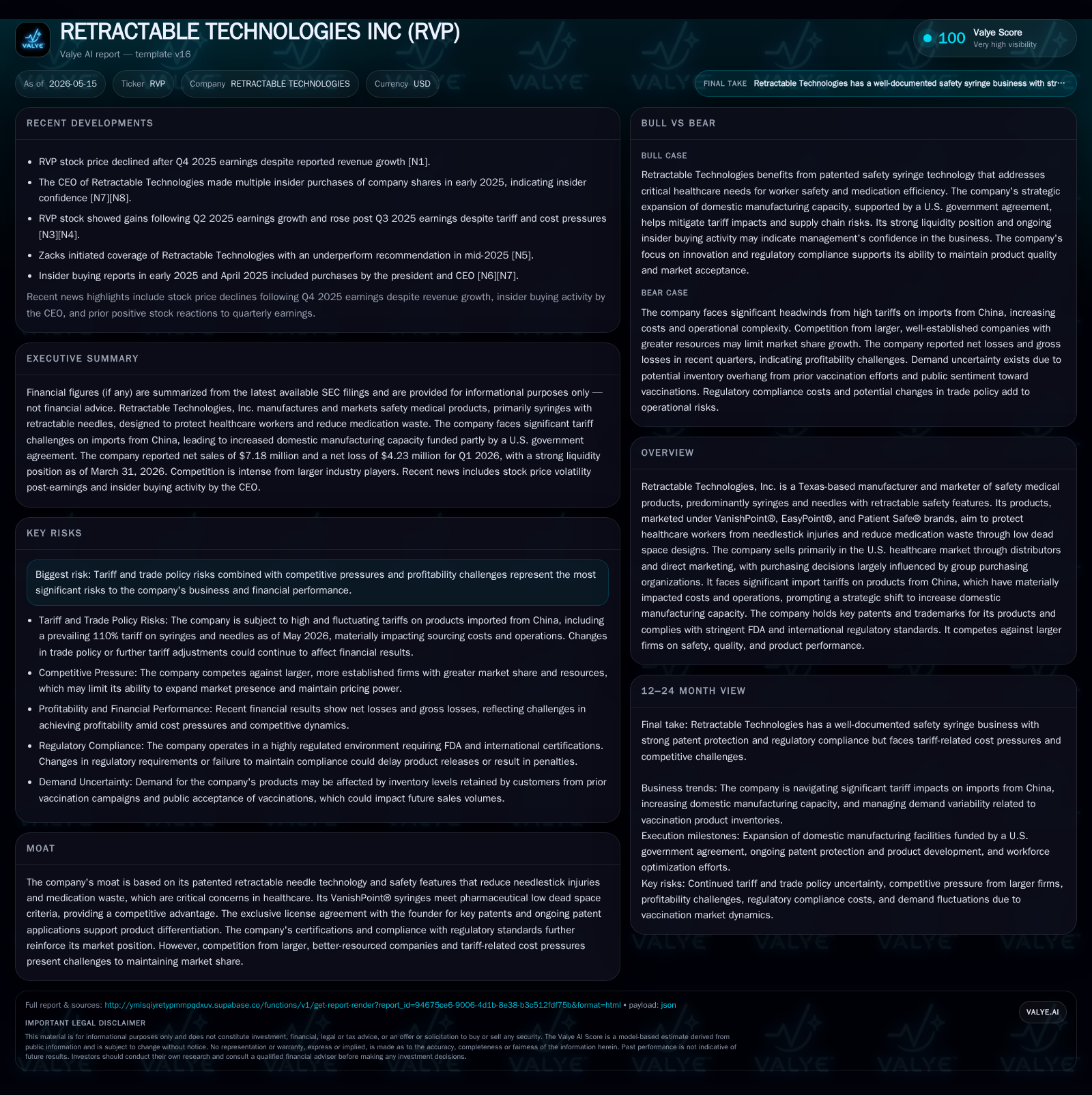

RETRACTABLE TECHNOLOGIES Confronts Tariffs with Domestic Manufacturing Expansion

Facing escalating tariffs on Chinese imports, Retractable Technologies pivots to expand domestic syringe production, reshaping its cost and supply strategies.

Retractable Technologies, a manufacturer of patented safety syringes and needles, is grappling with significant tariff pressures on imports from China that have elevated costs and complicated supply chains. The company’s latest quarterly filing reveals receipt of tariff refund overpayments and ongoing efforts to boost domestic manufacturing capacity to mitigate these effects. Despite healthy liquidity and a strong current ratio, profitability remains challenged by margin pressure from tariffs and increased operating expenses related to manufacturing shifts. The competitive landscape features regulatory barriers that support product differentiation but also intense competition from larger rivals. Key near-term growth drivers include commercializing domestically produced 0.5 mL syringes and leveraging proprietary low dead-space designs critical for vaccine administration.

Operational Update: Quarterly Results Spotlight Tariff-Driven Shifts

Retractable Technologies’ Q1 2026 10-Q reveals the immediate operational impact of heightened tariffs imposed on medical syringes and needles imported from China under evolving U.S. trade policy [S2]. The Office of the U.S. Trade Representative’s Section 301 tariffs originally set at 100% in late 2024 have effectively risen to approximately 120% following additional duties enacted after the U.S. Supreme Court vacated IEEPA-based tariffs early in 2026 [S1]. This has materially increased import costs for products forming over 60% of the company's sourcing portfolio.

The quarterly filing highlights a significant tariff refund overpayment received totaling $467,552 reflecting adjustments in retrospective tariff assessments [S2]. However, despite receiving this partial clawback, supply chain volatility persists given the complexity surrounding fluctuating tariff interpretations and supplier constraints [S2].

In direct response, RETRACTABLE TECHNOLOGIES has accelerated capital investments to expand its domestic manufacturing footprint in Little Elm, Texas. Modifications to existing equipment intend to enable fully domestic production of key products such as the 0.5 mL insulin syringe variant — a strategic priority as it reduces exposure to punitive tariffs [S1], [S2]. The company does caution that supply disruptions remain possible during this transition phase despite increasing localized output capacity.

Moreover, the firm executed workforce reductions amounting to approximately 16%, targeting $2.2 million in annualized payroll savings aimed at offsetting overhead increases related to scaling domestic manufacturing operations [S9]. This affirms management's pragmatic approach prioritizing operational efficiency alongside strategic realignment under external cost pressures.

Business Model and Product Portfolio: Safety Syringes Anchored by Proprietary Technology

RETRACTABLE TECHNOLOGIES operates by designing, manufacturing, and marketing safety-focused medical consumables within the healthcare sector — predominantly retractable syringes and needles designed to minimize needlestick injuries among healthcare workers while reducing medication waste through patented low dead space technologies [S1], valye_report_excerpt.

Revenue generation primarily stems from sales of branded products such as VanishPoint®, EasyPoint®, and Patient Safe® syringes distributed largely across U.S.-based healthcare institutions either through distributors or directly via group purchasing organizations (GPOs) [S1]. These organizations wield significant influence over procurement decisions due to aggregate buying power.

The company holds an exclusive license agreement for patented needle retraction technology held jointly with founder CEO Thomas J. Shaw since inception [S1]. This IP exclusivity creates considerable structural barriers against commoditized competition by embedding the safety mechanism into its core products. Moreover, low dead space syringes in their portfolio meet pharmaceutical industry criteria effectively enhancing drug utilization per vial, a compelling proposition amidst stringent medication stewardship initiatives pervasive in healthcare settings.

Patent protections cover both design features and mechanisms integral to retractability; ongoing patent applications sustain differentiation against larger competitors who produce conventional non-retractable devices or less optimized substitutes [S1].

Industry Positioning: Competitive Landscape and Regulatory Tailwinds

Within the specialized medical device market segment serving infection control needs, RETRACTABLE TECHNOLOGIES commands a defensible niche enabled by its technological IP moat yet faces stiff competition from larger global medtech firms capable of leveraging broader product portfolios and scale economies [S13].

Regulatory compliance forms both a hurdle for new entrants and a long-term advantage for incumbents like RETRACTABLE given their ISO 13485:2016 certification adherence along with participation in the Medical Device Single Audit Program (MDSAP) [S25]. This rigorous quality management system maintenance aligns with FDA clearance protocols requiring substantial investment in product development, clinical validations, labeling controls, and post-market surveillance — factors that collectively raise switching costs within hospital supply chains.

Tariff-induced input cost inflation imposes additional indirect competitive dynamics by elevating landed expenses especially for firms reliant on overseas component sourcing; conversely expanding U.S.-based production capabilities positions RETRACTABLE more favorably relative to import-dependent rivals potentially exposed to similar trade measures [S1],.

Growth Drivers: Domestic Manufacturing Pivot and Innovation Pipeline

RETRACTABLE TECHNOLOGIES' immediate growth catalyst stems from its strategic pivot toward enhanced domestic manufacturing capabilities intended to circumvent escalating import tariffs particularly impacting syringe assembly lines sourced out of China [S2]. By investing in new machinery adaptations at its Texas site capable of producing commercially viable batches of sensitive dosage instruments like the 0.5 mL insulin syringe domestically, management aims to stabilize input costs while shortening supply chains [S1].

This shift dovetails with a federally backed Technology Investment Agreement (TIA) extending through mid-2030 which supports capitalization initiatives including equipment upgrades while granting government preference rights amid public health emergencies—an endorsement reinforcing operational resilience plus innovation velocity within biologics administration tools [S1].

Further augmenting growth prospects is RETRACTABLE’s proprietary patent estate covering engineering nuances that optimize dose efficiency via low dead space designs prevalent in VanishPoint® syringes used heavily in vaccine delivery protocols — where reducing waste translates directly into cost savings for institutional buyers, [S7].

Healthcare demand fundamentals such as growing vaccination programs globally combined with regulatory mandates promoting safer injection practices sustain structurally robust end-market demand despite cyclical elements related to seasonal prevalence such as flu shots implementation patterns [S1],. Organizational emphasis on GPO contract renewals spotlight customer retention dynamics crucial for securing recurring revenue pools as unit volumes scale alongside higher-margin domestic product lines.

Risks and Constraints: Tariffs, Competition, and Supply Chain Uncertainties

Despite operational adjustments designed to mitigate trade policy exposures, ongoing tariff volatility constitutes a persistent growth dampener creating unpredictability in forecasting landed costs particularly amid fluid geopolitical environments involving Section 301 powers supplemented by enactments under International Emergency Economic Powers Act (IEEPA) provisions later struck down by the Supreme Court [S1],. The residual combined tariff rate currently charged at ~120% on syringe imports plus an additional ad valorem duty compounds margin pressure forcing continuous strategic rebalancing.

Competitive intensity emanates chiefly from larger diversified medical device manufacturers who can absorb cost shocks through scale or redirect distribution advantages but lack comparable patented safety features embedded within RETRACTABLE’s commercial products limiting price wars to some extent while capping market share gains by smaller peers [S13], valye_report_excerpt.

Legal risk exposure revolves around maintaining patent enforceability against potential challenges or expiry scenarios that could undermine protection layers enabling premium pricing structures; renewal cycles for exclusive founder licensing agreements require ongoing diligence lest IP licenses become contested or nonexclusive over time [S1].

Additionally, supply chain risks remain salient notwithstanding moves toward U.S.-based production—material procurement delays or quality deviations on complex device components can disrupt fulfillment schedules adversely affecting distributor relations and buyer confidence especially under time-sensitive public health campaign calendars.

Lastly regulatory compliance costs tied to evolving international data privacy statutes (e.g., EU GDPR convergence laws), FDA cybersecurity guidelines for medical devices alongside healthcare fraud/anti-kickback statutes introduce operational friction points demanding sustained capex allocation not always immediately revenue-accretive but essential for uninterrupted market access [S13].

Forward Look: Key Milestones and Demand Signals to Monitor

Strategic progress hinges critically on achieving commercial-scale production capability milestones for domestically manufactured syringes notably the planned rollout of a fully made-in-USA 0.5 mL insulin syringe line projected imminent based on ongoing equipment adaptation disclosures in Q1 filings [S2]. Monitoring output volumes ramped via manufacturing KPIs alongside inventory turnover rates will illuminate operational execution success.

Trade policy developments remain a wildcard warranting close attention—any legislative amendments affecting Section 301 implementation or new bilateral trade agreements revising tariff structures could materially alter cost bases going forward.

Further indicators include contract award announcements from GPOs reflecting customer adoption velocity plus backlogs reflecting pipeline strength within hospital systems adapting injection safety standards aligned with regulatory mandates.

Regular review of quarterly profitability metrics encompassing gross margins net of royalty obligations payable under founder licensing terms will help assess whether cost containment efforts outweigh residual tariff expenses whilst general administrative overhead stabilizes post recent workforce rationalizations [S9].

Finally, intellectual property developments such as pending patent grants or infringement claims will influence longer-range competitive positioning sustainability.

Financial Snapshot: Liquidity, Leverage, and Profitability Trends

Latest financial snapshot

| Metric | Value | Period |

|---|---|---|

| Cash & equivalents | $2.77 million | |

| 2026-03-31 | ||

| Total debt | $895,645 | |

| 2025-12-31 | ||

| Current assets | $59.96 million | |

| 2026-03-31 | ||

| Current liabilities | $10.45 million | |

| 2026-03-31 | ||

| Current ratio | 5.74x | |

| 2026-03-31 |

Source: SEC companyfacts cache [F1], Q1 2026 10-Q [S2].

As of March 31, 2026 end-quarter reporting indicates cash & cash equivalents at approximately $2.77 million supported by current assets totaling nearly $60 million contrasted against current liabilities around $10.45 million yielding a robust current ratio near 5.74 — signaling strong short-term solvency buffers amidst working capital demands accompanying business model transformation efforts [F1], [S2].

Total debt stands at roughly $895 thousand corroborated by latest full-year balance sheet snapshots illustrating modest leverage levels contributing to manageable financial risk profiles [F1].

On income statement fronts trailing twelve months continue showing operating losses attributable principally to amplified cost structures driven by tariffs plus incremental expenses tied to manufacturing investment activities alongside residual inefficiencies during capacity scale-up phases evident in year-end 2025 disclosures where loss from operations exceeded $21 million albeit partially offset by royalty expense increases closely correlated with sales trends [F1], S7], S10].

| Metric | Amount ($) |

|---|---|

| Cash & Cash Equivalents | 2,765,893 |

| Total Debt | 895,645 |

| Current Assets | 59,958,211 |

| Current Liabilities | 10,446,106 |

| Current Ratio | 5.74 |

| Tariff Refund Received | 467,552 |

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments