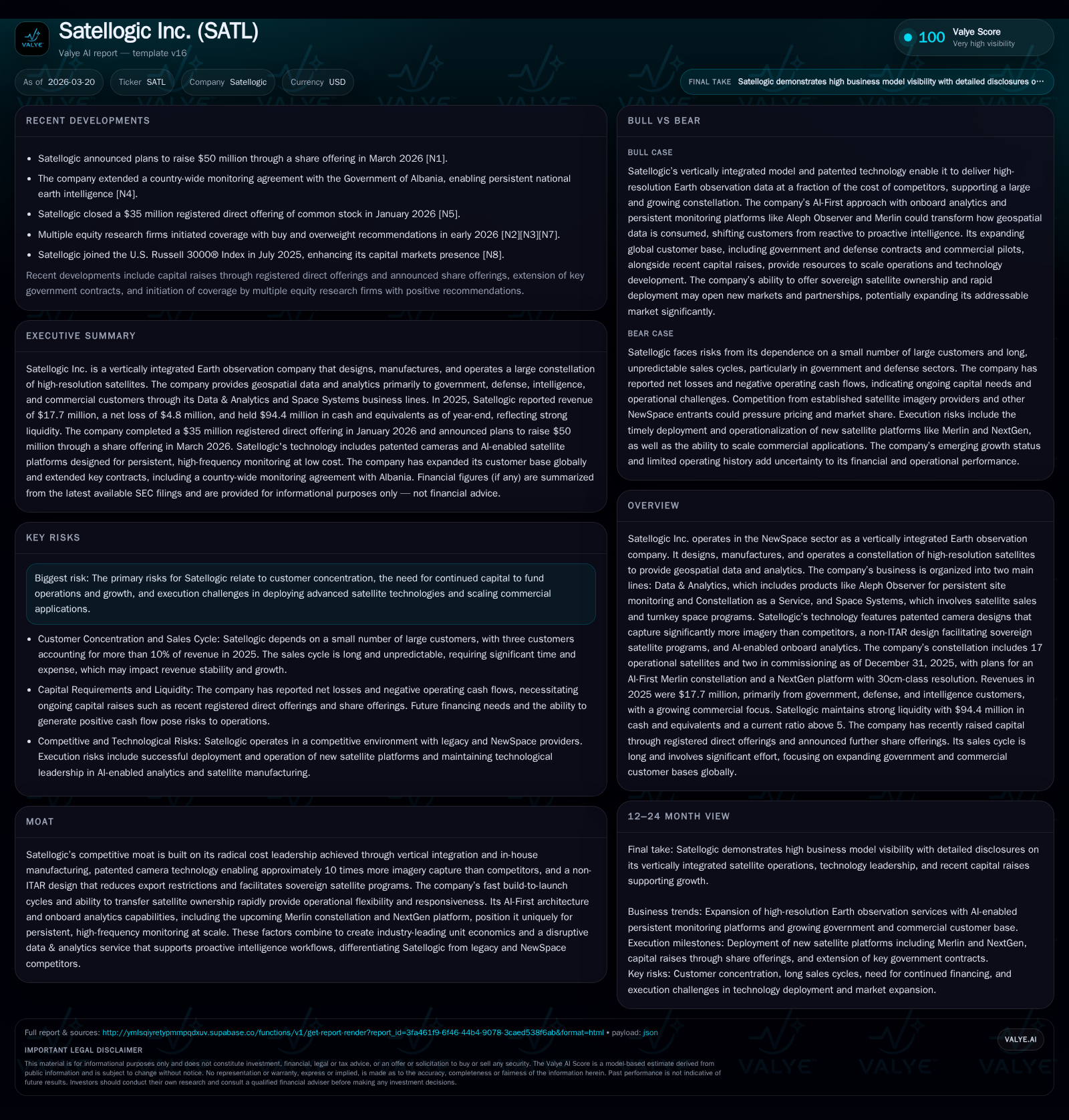

Satellogic Inc. Advances High-Resolution Earth Observation With Cost Leadership and AI Integration

Satellogic’s vertical integration and patented technology drive growth in data services and satellite sales amid a constrained EO market.

Satellogic Inc., a vertically integrated Earth observation company, operates one of the largest commercial high-resolution satellite constellations with radical cost advantages through in-house manufacturing and patented camera designs. The company focuses on Data & Analytics—including its Aleph Observer platform for persistent monitoring—and Space Systems, involving turnkey satellite sales primarily to government clients. In 2025, revenue increased 37.6% year-over-year to $17.7 million, reflecting growing demand from government and commercial customers. Despite continued operating losses, improved operating income and cash flow trends signal progress toward sustainable growth as the firm expands its constellation and AI-enabled platforms.

Company Overview

Founded in 2010 by Emiliano Kargieman and Gerardo Richarte, Satellogic Inc. is a vertically integrated NewSpace Earth observation company that designs, manufactures, launches, and operates a proprietary constellation of high-resolution satellites combined with advanced analytics platforms serving government agencies, defense/intelligence (D&I) customers, and commercial operators globally [S1][S16]. The company's mission is to democratize access to geospatial data addressing large-scale challenges such as climate change and food security.

As of December 31, 2025, Satellogic operated 17 satellites with two additional units undergoing commissioning—forming one of the largest high-resolution EO constellations commercially deployed today [S1]. This asset base underpins the firm's capacity advantage within a supply-constrained market where demand routinely exceeds legacy providers’ availability.

Historical Performance

Financially, Satellogic has shown improving profitability trends while continuing to scale. Annual revenues increased nearly 38% from $12.87 million in 2024 to $17.71 million in 2025 led by growth within Data & Analytics—including Aleph Observer—and steady contribution from Space Systems satellite sales [F1][S15]. Operating loss narrowed to $31.0 million in 2025 from $52.2 million the prior year due largely to improved cost absorption across production and R&D as scale accelerated [F1].

Operating cash flows used also declined but remained negative at approximately $26.9 million due primarily to ongoing investments expanding satellite production capabilities and operational scaling efforts [F1][S1]. Capital expenditures increased to $7.4 million reflecting ramped factory development and satellite component purchases necessary for future constellation growth.

Historical performance (annual)

| FY | CFO ($mm) | OpInc ($mm) | Capex ($mm) |

|---|---|---|---|

| 2025 | -27 | -31 | 7 |

| 2024 | -36 | -52 | 5 |

| 2023 | -50 | -69 | 15 |

| 2022 | -68 | -91 | 27 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Buybacks ($mm) | FCF ($mm) |

|---|---|---|

| 2025 | -34 | |

| 2024 | -41 | |

| 2023 | 0 | -64 |

| 2022 | 9 | -96 |

Source: SEC companyfacts cache [F1].

Note: Operating income has improved steadily while revenues have increased since at least 2024; capital expenditures reflect investment cycles.

Liquidity strengthened through equity raises totaling approximately $125 million during late 2025 through early 2026, increasing cash & equivalents to $94 million at year-end—deemed sufficient by management for at least twelve months of operations [N1][S6][F1]. No dividends or share repurchases occurred during this period consistent with typical capital preservation priorities of growth-stage NewSpace companies [S20].

Competitive Moat and Differentiation

Satellogic’s competitive advantage derives from radical cost leadership achieved via vertical integration controlling nearly all aspects of satellite design, manufacture, and operations centralized in Montevideo, Uruguay—a free-trade zone easing logistics and tax burdens—and proprietary technologies including patented camera modules capturing about ten times more imagery per satellite than peers [S1][S22]. This capacity enables higher revisit rates at lower costs.

The company’s non-ITAR hardware design avoids U.S.-export restrictions enabling sovereign space program contracts globally with rapid knowledge transfer models where governments locally assemble satellites supported remotely or onsite as needed [S1][S12][S23].

An AI-first architecture underpins platforms like Aleph Observer which shifts EO procurement away from episodic tasking toward continuous persistent monitoring across extensive site portfolios—critical for intelligence and defense sectors [S1][S21]. The forthcoming Merlin constellation expected circa 2027 aims to embed onboard analytics enabling near real-time decision-grade intelligence generation extending reach beyond traditional geospatial customers.

These factors yield strong unit economics positioning Satellogic both as a cost champion and market disruptor expanding EO's addressable market into commercial sectors reliant on costly or fragmented alternatives like drones or third-party datasets [S9][S16].

Revenue Breakdown and Customer Concentration

Revenue derives mainly from two streams: Data & Analytics including tasking services bundled under "Constellation as a Service" offerings like Aleph Observer (90%+ contribution), complemented by Space Systems sales comprising direct satellite sales or turnkey programs primarily for international governments seeking sovereign orbital assets (10%+) [S15][S16]. Geographic revenue distribution is North America (68%), Europe (16%), Asia-Pacific (14%), South America (2%) reflecting global reach weighted toward developed markets with ongoing expansion into emerging regions [S12][S26].

Customer concentration remains significant with three clients each accounting for over 10% of total revenues during 2025 including a technology company providing software-for-imagery credits annually ($4m/year minimum commitment) alongside longstanding government D&I contracts renewed early 2026—highlighting execution risks given lengthy public-sector sales cycles [S4][S8][S22].

Growth Prospects and Strategic Initiatives

Mid-to-long term growth plans focus on scaling the AI-first Merlin constellation aimed at planetary persistent monitoring capable of servicing millions of sites daily—moving from reactive imagery provision toward autonomous intelligence workflows underpinning predictive security threat identification or supply chain resilience analyses [N2][N3][S1][S19]. This requires augmented manufacturing throughput supported by recent factory expansions alongside modular NextGen platform improvements targeting enhanced resolution (30 cm-class), onboard multispectral processing, non-ITAR exportability, and full AI analytic integration on-orbit expanding sovereign customer appeal plus commercial adaptability [S23].

Commercialization includes self-service booking APIs via Aleph Platform reducing friction for enterprise clients especially in agriculture or utilities sectors demanding scalable access without manual tasking standard in EO industry ecosystems [S8][S21]. Partnerships such as exclusive U.S. distribution through Vantor Intelligence focusing on defense/intelligence clients alongside regional resellers like Suhora Technologies support geographic diversification ambitions; potential acquisitions may further enhance vertical integration or complementary software capabilities depending on capital availability [S19][N2].

Risks And Challenges

Execution risks include balancing capital-intensive manufacturing scale-up against nascent commercial revenue generation resulting in ongoing negative cash flows requiring continued capital inflows despite recent equity raises—any disruption could impair runway notably if major customer orders decline amid concentrated governmental buyer base subject to geopolitical budget fluctuations [S10][S11][S27].

Competition includes aerospace incumbents deploying higher-cost feature-rich satellites alongside emerging low-cost NewSpace entrants trading resolution versus revisit frequency limiting capture volume—Satellogic’s high-volume imagery approach faces pressure if state-backed competitors undercut pricing or innovate faster across technology facets simultaneously [S17][S18]. Intellectual property protection challenges may arise especially where enforcement is limited risking erosion of proprietary advantages.

Regulatory compliance costs related to anti-corruption laws internationally along with geopolitical sensitivities selling dual-use technologies increase operational complexity necessitating robust governance frameworks commensurate with expanded footprint—risks include reputational damage or legal exposure particularly when partnering via third-party resellers common in global defense supply chains [S10][S11][N3].

Capital Allocation Summary

Capital allocation prioritizes reinvestment into production facilities and R&D rather than shareholder returns—no dividends declared nor share repurchases conducted consistent with growth-stage profile balancing liquidity preservation against expansion plans absorbing around $7–8 million annually focused mainly on satellite manufacturing assets upgrades and facility expansions benefiting from Uruguay’s favorable trade status reducing landed costs versus traditional aerospace hubs [F1][S20].[F1] Return measures approximate negative ROE near -7.9% for FY 2025 calculated from net loss relative to reported equity base reflecting continuing need to scale profitably albeit signaling improvement versus prior years marked by heavier losses underpinning management’s emphasis on controlled workforce growth while advancing go-to-market initiatives focused on market expansion rather than margin contraction typical among NewSpace players currently requiring patient capital cycles before returns materialize [F1].[F1]

What To Watch Forward (Analysis)

- Execution of Merlin constellation launches planned through 2027 unlocking broad-scale persistent intelligent monitoring essential for expanding beyond initial governmental anchor customers.

- Sales cycle dynamics surrounding renewals of key multi-year contracts within U.S., allied D&I agencies serving as barometer for sustained government spend commitment amid geopolitical tensions.

- Expansion success into commercial verticals leveraging Aleph Platform's self-service API model signaling validation beyond traditional space policy-driven budgets.

- Potential strategic partnerships or acquisitions enhancing vertical integration or software analytic capabilities augmenting data product differentiation within competitive EO landscape.

- Ongoing capital raising appetite necessary to fuel manufacturing throughput increases balanced against timing toward positive operating cash flow conversion marking inflection point signaling sustainable financial health.

Disclaimer

This analysis is based solely on publicly available information including SEC filings through March 19, 2026 and referenced news releases without any confidential insight or forward-looking guidance issued directly by the company beyond disclosed materials. All financial figures are derived strictly from reported historical data without forecasts or investment recommendations offered here.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments