Sky Harbour Group Corp Expands HBO Campuses to Address Soaring Private Jet Hangar Demand

Sky Harbour leverages proprietary HBO campus designs to solve capacity constraints in private jet hangars amid surging demand for larger business aircraft.

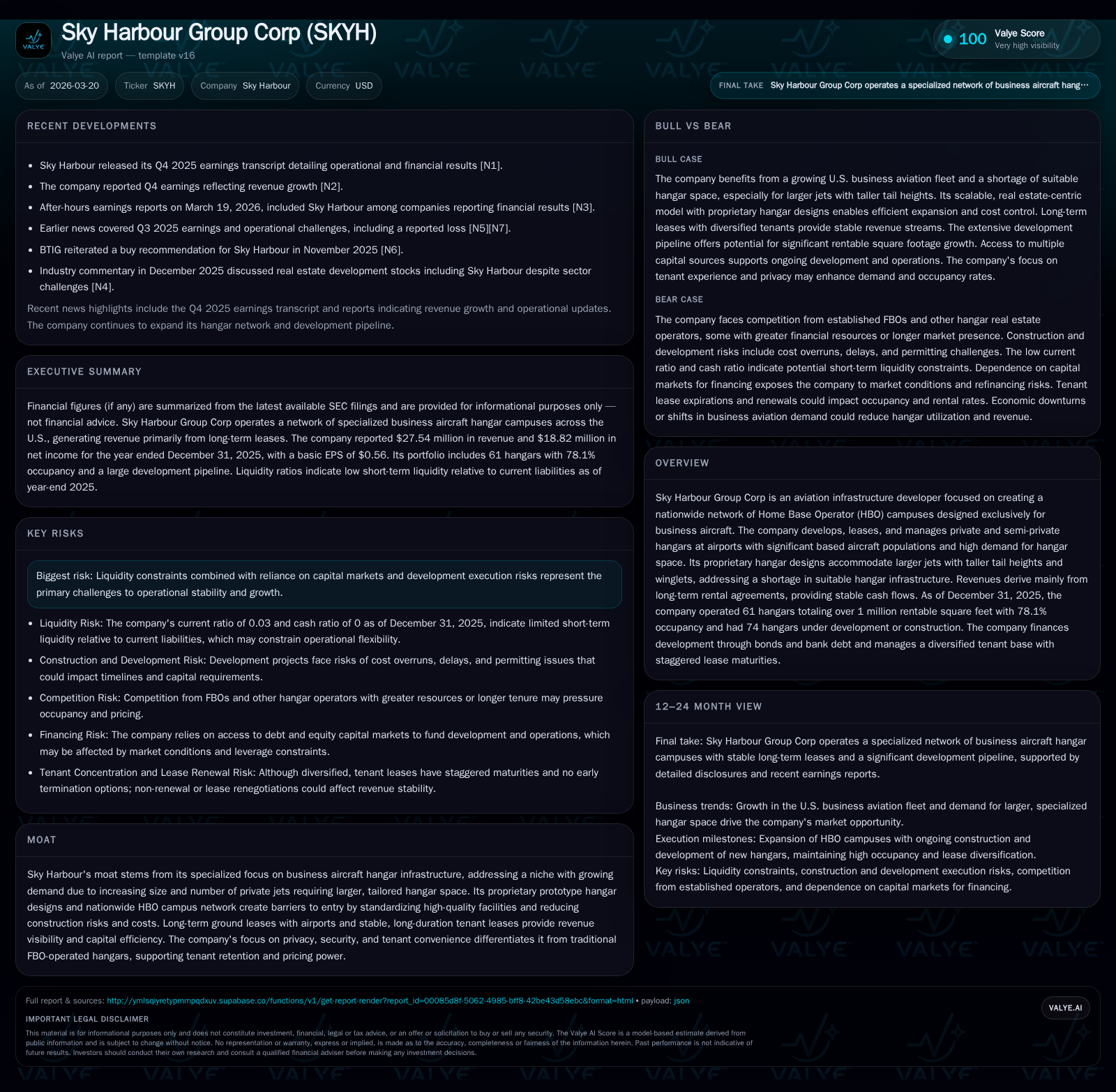

Sky Harbour Group Corp has rapidly expanded its footprint in the niche market of business aircraft hangar infrastructure, capitalizing on a structural shortage of suitably sized hangars driven by the growth of large private jets with taller tail heights and winglets. Despite strong top-line growth reaching $27.54 million in 2025, operating losses remain elevated due to aggressive capital expenditures required for development of new HBO campuses. The company maintains a diversified tenant base with long-term leases providing steady revenue visibility but faces liquidity and execution risks given its dependence on bond financing and bank debt. Monitoring project completions, occupancy stabilization near current ~78%, and capital market conditions will be critical to assess Sky Harbour's path toward positive operating cash flow and sustainable returns.

Historic Revenue Surge Driven by Strategic HBO Campus Expansion

Sky Harbour Group Corp's revenue trajectory exemplifies its aggressive expansion within the Home Base Operator (HBO) aviation infrastructure niche. From a modest $1.85 million in fiscal year (FY) 2022, revenues climbed sharply to $7.58 million in FY2023 (+311%), $14.76 million in FY2024 (+94%), and reached $27.54 million by FY2025, an impressive +86.6% growth over the prior year [F1]. Despite this revenue acceleration, operating income remained negative at -$28.03 million in FY2025, deepening from -$20.41 million in FY2024, reflecting high operating costs tied to development activities and scale-up expenses.

Net income displayed marked volatility: losses peaked at -$45.23 million in FY2024 before swinging to a positive $18.82 million net income in FY2025 [F1]. This turnaround is likely driven by non-operating factors including interest rate hedging benefits, revaluation items, or tax effects rather than core operational profitability given continued negative operating income.

Capital expenditures surged to $9.51 million in FY2025 from just $2.26 million a year earlier (+320%), underpinning ongoing construction across multiple HBO campuses [F1]. However, the company's operating cash flow remains negative (-$2.34 million FY2025), resulting in free cash flow estimated at approximately -$11.85 million after accounting for capex [F1]. This dynamic illustrates the capital-intensive nature of scaling infrastructure assets despite top-line gains.

Historical performance (annual)

| FY | Rev ($mm) | Net ($mm) | CFO ($mm) | OpInc ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 28 | 19 | -2 | -28 | +86.6% | +141.6% |

| 2024 | 15 | -45 | -9 | -20 | +94.9% | -179.6% |

| 2023 | 8 | -16 | -8 | -17 | +310.6% | -408.1% |

| 2022 | 2 | -3 | -27 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) |

|---|---|

| 2025 | -12 |

| 2024 | -11 |

| 2023 | -9 |

| 2022 | -29 |

Source: SEC companyfacts cache [F1].

Table summarizes annual financial performance highlighting rapid revenue growth overshadowed by substantial operating losses and heightened capital expenditure.

Structural Demand Drivers: Growth in Larger Business Jets Constraining Traditional Hangars

The fundamental driver behind Sky Harbour’s strategic positioning is the pronounced demand imbalance for business jet hangar space rooted in the fleet composition shift toward larger aircraft requiring customized infrastructure solutions [S1]. The cumulative physical footprint of the U.S. business aviation fleet grew by roughly 46 million square feet since circa 2009–10 — a +73% increase through mid-2020s — while supply has lagged considerably.

Notably, the segment of large jets exceeding a tail height of approximately 24 feet has seen an even more dramatic rise of +120% over this timeframe [S1]. Modern winglets further complicate conventional storage methods used by fixed base operators (FBOs), such as wing-over-wing stacking — as winglet interference restricts compact hangar layouts.

These dynamics have resulted in multi-year waiting lists at airports with significant based aircraft populations where conventional shared or community-style hangars prove inadequate both in size and privacy/security provisions.

Forecasts underpinning this trend include expected delivery of up to approximately 8,500 new business jets worth over $283 billion between calendar years 2025–2034 — predominantly comprising larger aircraft requiring extended height clearances — supported by robust order backlogs totaling over $57 billion [S1]. This secular expansion places Sky Harbour’s specialized HBO campus model at a pivotal position amidst constrained airport real estate.

Assessing Supply-Side Constraints and Sky Harbour’s Prototype Economies of Scale

With widespread underinvestment prevalent among FBO-style general aviation operators—and lingering obsolescence issues—Sky Harbour’s scalable approach via replicable prototype hangar designs introduces efficiencies absent from fragmented competitors [S1][N1].

Developed through centralized construction management capabilities and general contracting expertise executed internally by Sky Harbour LLC subsidiaries allows streamlined permitting processes alongside standardized procurement.

This model promotes cost control benefits while accelerating time-to-completion timelines essential for tapping today’s undersupplied markets characterized by high demand elasticities among sophisticated owners requiring flexibility combined with superior privacy features.

Long-term ground leases secured from airport authorities spanning several decades reduce tenure risks providing foundational platform stability beneficial for capital markets financing as evidenced by the issuance of Series Bonds backed by such collaterals [S4][S8]. This barrier-to-entry effect limits immediate competitive encroachment given complex regulatory environments paired with financing thresholds difficult for single-asset operators.

Tenant Base Stability and Lease Visibility Amid Scaling Operations

Tenant diversification is key considering leasing risk inherent to niche aviation real estate sector characteristics [N1][S21]. As of late FY2025 reporting dates, Sky Harbour managed approximately 85 tenant leases scattered across its portfolio featuring staggered maturities averaging roughly five-and-a-half years weighted by contractual payments [S21].

Occupancy hovered near ~78%, reflecting reasonable absorption rates given the addition of over one million rentable square feet across owned facilities as well as new construction underway totaling an additional portfolio of some seventy-four hangars [N1][S1].

Lease structures primarily involving long-term gross or triple-net formats ensure tenants bear expenses related to insurance/taxes/common area maintenance while enabling Sky Harbour consistent rental escalations tied often to prevailing market indices bolstering pricing power.

Privileged positioning through curated client access emphasizing privacy and security enhances tenant retention likelihood relative to FBO alternatives where shared transient operations dilute such exclusivity norms.

Balancing Accelerated Capital Spend and Liquidity Constraints

Capital intensity remains one of the defining challenges as Sky Harbour executes a multi-year buildout plan that could scale into billions cumulatively by targeting an approximate fifty-airport system over time [S26][N1].

FY2025 capex nearly quadrupled compared to FY2024 reflecting both expedited project delivery efforts as well as inflationary pressures on construction labor/material costs [F1]. To fund this expansion pipeline management leverages a structured capital stack blending bank term loans ($200 million facility arranged September ‘25), private activity bonds issued periodically starting with Series 2021 Bonds ($166 million principal outstanding), and issuance of additional unsecured promissory notes aggregating ~$25 million [S4][S5][S9]. Equity issuance programs like ATM facilities supplement financing flexibility though trading price considerations moderate active utilization levels [S4].

Covenant frameworks embedded within loan agreements enforce standard leverage caps (~65%) alongside financial metrics including minimum debt service coverage ratios (DSCR ≥1.25x commencing post substantial project completions circa late CY2028/early CY2029 per agreement terms) restricting distributions/dividends until such conditions met [S10][S15]. Such covenant discipline aligns with broader bondholder protections while constraining discretionary capital returns during ramp phases.

Interest Cost Hedging and Debt Covenants: Managing Financial Risk

Since Q4 ’25 onwards Sky Harbour implemented interest rate swaps fixing underlying SOFR components on drawn term loan balances up to $200 million aiming around 2.65% effective fixed rates inclusive of spreads – reducing exposure amid rising global rates environment [S6][S10]. Series Bonds carry fixed coupon rates ranging from circa mid-4% for Series 2021 maturities out through mid-2050s versus recently issued Series 2026 Bonds at a higher rate (6%) tied to longer maturity horizons with mandatory tender/refinance clauses approx every five years introducing refinancing contingencies [S9][S26].

Additional guarantees such as Non-Recourse Carveout Guaranties limit parent level risk exposure primarily pertinent under misconduct or default scenarios thereby ring-fencing asset subsidiaries holding underlying real estate collateral pools facilitating needed risk segregation attractive to lenders/investors [S7][S15].

Near-Term Milestones: Progress in Development Pipeline and Occupancy Targets

Recent strategic initiatives exemplify Sky Harbour’s progress with ground lease acquisitions finalized at Long Beach Airport covering about seventeen acres on fifty-year terms commencing mid-2027 alongside Fort Worth Meacham International Airport lease extending forty years starting immediately as announced late CY’25 / early CY’26 respectively [N1][S23]. These agreements expand geographical diversification bandwidth beyond incumbent hubs while catering primarily to premium clientele demanding HBO services unmatched elsewhere.

The confidential leasing velocity metrics from ongoing developments directly influence adjustment timing on debt service reserve account releases according to credit agreements suggesting sustained progress must materialize for easing financial restrictions ahead of main amortization phases starting circa CY2032 per bond schedules [N1][S15][S16].

Monitoring occupancy upticks beyond current three quarters threshold (~78%) along with lease renewal adherence will serve as barometers bridging transition from development losses towards cash flow positivism.

Investment Implications: Cash Flow Challenges Temper Long-Term Growth Vision

The economic reality facing Sky Harbour involves reconciling robust demand fundamentals driving sizable backlog orders for large business jets against sizeable upfront capital needs manifesting as persistent negative free cash flows nearing -$11.85 million last fiscal year despite improved operational scale benefits [F1][N1]. While net income turned positive owing notably to non-cash/non-recurring elements ROE stood around negative -102%, indicating legacy accumulated deficits still dominant.

Accessing attractive incremental funding through debt/equity markets relies heavily on market sentiment around real estate infrastructure plays compounded by broader macroeconomic interest rate trajectories influencing borrowing costs/spread premiums thus impacting funding availability on favorable terms going forward.[S26]

Execution risks associated with construction delays permit risk buffers embedded via phased loan draws but warrant close scrutiny especially amid labor/material inflation pressures.[N1]

In summary, stakeholders should watch lease-up velocity stabilizing above prior occupancy benchmarks alongside scheduled project completions triggering covenant relaxations enabling liquidity releases while ongoing cost containment fosters sustainable cash flow turning points necessary before deeming earnings quality improvements durable.

This analysis synthesizes available public financial filings and company disclosures without making investment recommendations or forecasts beyond documented guidance or explicitly stated milestones.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments