Stoke Therapeutics’ Phase 3 Trial Progress and Financial Turnaround Reflect Biotech Operational Maturation

Clinical-stage Stoke Therapeutics moves toward potential regulatory filings for zorevunersen while sharply improving financial metrics.

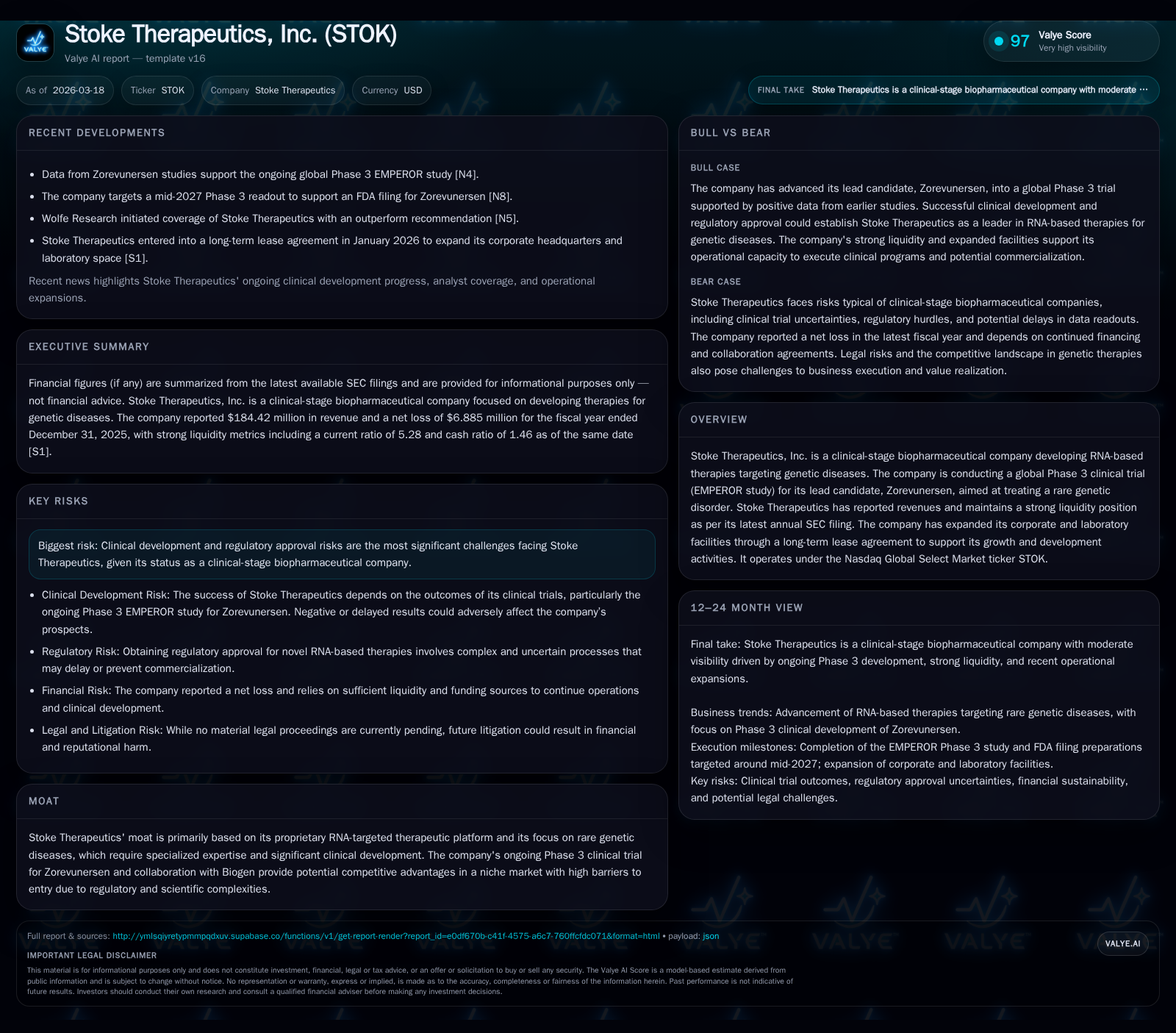

Stoke Therapeutics, a clinical-stage RNA therapeutics company focused on rare genetic diseases, is advancing its lead asset zorevunersen through a global Phase 3 trial. The company’s revenue surged over 400% year-over-year in fiscal 2025, driven by collaboration milestones and licensing income, alongside a marked improvement in operating losses and cash flow. With an expanded corporate footprint and liquidity expected to fund operations into 2028, Stoke is navigating clinical and regulatory complexities amid ongoing FDA interactions. The forthcoming EMPEROR trial data readout in mid-2027 and anticipated New Drug Application submission form the near-term operational focus.

Company Overview and Industry Position

Stoke Therapeutics operates at the frontier of RNA-based therapeutic modalities targeting genetically driven diseases with substantial unmet need. Its sole late-stage asset, zorevunersen, is being developed as a novel antisense oligonucleotide therapy intended to alter disease progression in Dravet syndrome—a rare, severe form of epilepsy manifesting early in life. This focus situates Stoke within the specialized niche of rare disease biopharma where scientific expertise, regulatory complexity, and patient population fragmentation create formidable barriers to entry but also significant reimbursement potential for successful therapies.

The company’s proprietary RNA modulation platform enables allele-selective upregulation or downregulation of gene expression. Phase 1/2a data coupled with ongoing open-label extension studies have demonstrated durable seizure frequency reductions, associated cognitive and behavioral benefits, and an acceptable safety profile—elements critical for regulatory validation in this class of medicines. Collaboration with Biogen provides both development funding and strategic commercialization support.

Historical Financial Performance

From a financial standpoint, Stoke has progressed from early-stage development losses typical in biotech towards operational inflection points characterized by meaningful revenue gains largely attributed to milestone achievements under collaboration agreements. According to the latest fiscal year-end SEC filing (FY2025), revenues surged by over fourfold to approximately $184 million compared to roughly $36.5 million in FY2024 [F1]. The increase primarily reflects license fees and milestone receipts from Biogen collaborations rather than product sales given the absence of approved commercial products.

Operating losses narrowed dramatically to about $20.6 million from previous multi-year deficits exceeding $100 million annually (e.g., -$114.8M in FY2023) indicating improved expense management as clinical programs mature and non-recurring costs subside. Net losses also decreased substantially to roughly $6.9 million in FY2025 from nearly $89 million the prior year [F1]. Importantly, operating cash flow turned positive at $45.6 million versus negative cash flows previously—reflecting milestone-related cash inflows outpacing R&D and G&A expenditures [F1]. Capital expenditures remain modest relative to operational scale.

Summary Financials Table

Historical performance (annual)

| FY | Rev ($mm) | Net ($mm) | CFO ($mm) | OpInc ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 184 | -7 | 46 | -21 | +404.5% | +92.3% |

| 2024 | 37 | -89 | -87 | -101 | +316.3% | +15.0% |

| 2023 | 9 | -105 | -81 | -115 | -29.2% | -3.6% |

| 2022 | 12 | -101 | -32 | -104 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2025 | 45 | -2.0 |

| 2024 | -87 | -38.9 |

| 2023 | -83 | -65.6 |

| 2022 | -36 | -54.7 |

Source: SEC companyfacts cache [F1].

Revenues reflect explosive growth primarily driven by external collaborations; significant reduction in operating losses evidences scale efficiencies.

Forward-Looking Development Milestones

The pivotal Phase 3 EMPEROR study continues with an enrollment target of approximately 150 patients worldwide aimed for completion in Q2 calendar year 2026. Mid-2027 is targeted for full data readout which Stoke anticipates will underpin its initial rolling New Drug Application submission to FDA within the first half of that year [S18][N4]. FDA interactions indicate ongoing dialogue requesting additional data but no changes mandated on trial design or timelines thus far. Stoke is actively exploring opportunities for accelerated regulatory review leveraging unmet clinical needs and encouraging preliminary results [S18].

These milestones represent critical inflection points that will materially influence Stoke’s regulatory trajectory and downstream commercialization roadmap.

Capital Allocation and Liquidity Position

As of December 31, 2025, Stoke held approximately $84.2 million in cash and equivalents supported by total current assets exceeding $305 million against current liabilities near $57.9 million—yielding a strong current ratio above five-to-one which underscores short-term financial health [F1]. Combined with eligible proceeds from Biogen collaborations reported in early January press releases [S9][S18], this liquidity is expected to fund operations into at least calendar year-end 2028.

Strategic capital allocation includes a long-term lease agreement for roughly 98,500 square feet of expanded corporate headquarters and laboratory facilities through March 2038—signaling intent to scale infrastructure aligned with late-stage clinical advancement demands [S16].

CEO Ian F. Smith’s appointment as permanent head effective October 6, 2025 marked executive leadership stabilization; his compensation package includes performance-based incentives tied directly to company milestones achieved since his interim tenure beginning March 2025 [S24][S28].

Return metrics such as ROE remain negative due to net losses typical of clinical-stage biotechs pre-commercialization; however free cash flow turned positive at approximately $44.9 million in FY2025 after subtracting capital expenditures from operating cash flow—supporting operational sustainability absent immediate financing needs [F1].

Risks Highlighted by Company Disclosures

Clinical development risks predominate; success depends on favorable Phase 3 outcomes translating into regulatory approvals under stringent safety benchmarks while managing complex side effect profiles inherent to CNS disorders treated via intrathecal dosing routes [S4][S6][S19]. Intellectual property defense costs and potential litigation exist but no material proceedings currently threaten operations [S1][S4][S5]. Market acceptance post-approval will require pricing negotiations amid competitive orphan drug landscapes.

Conclusion

Stoke Therapeutics exemplifies a maturing clinical-stage biotech transitioning from heavy R&D spend phases into revenue-generating milestones tied to late-stage clinical progress. Revenue growth fueled by milestone payments provides monetization potential crucial for sustaining innovation ahead of pivotal regulatory events.

With its lead RNA-targeting candidate nearing key data inflection points supported by stable financial footing and collaborative backing from Biogen, Stoke is positioned at a critical juncture where scientific validation could translate into tangible commercial opportunities within rare genetic neurology treatments.

This analysis presents factual information based on current public disclosures without offering investment advice or recommendations related to Stoke Therapeutics shares or securities.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments