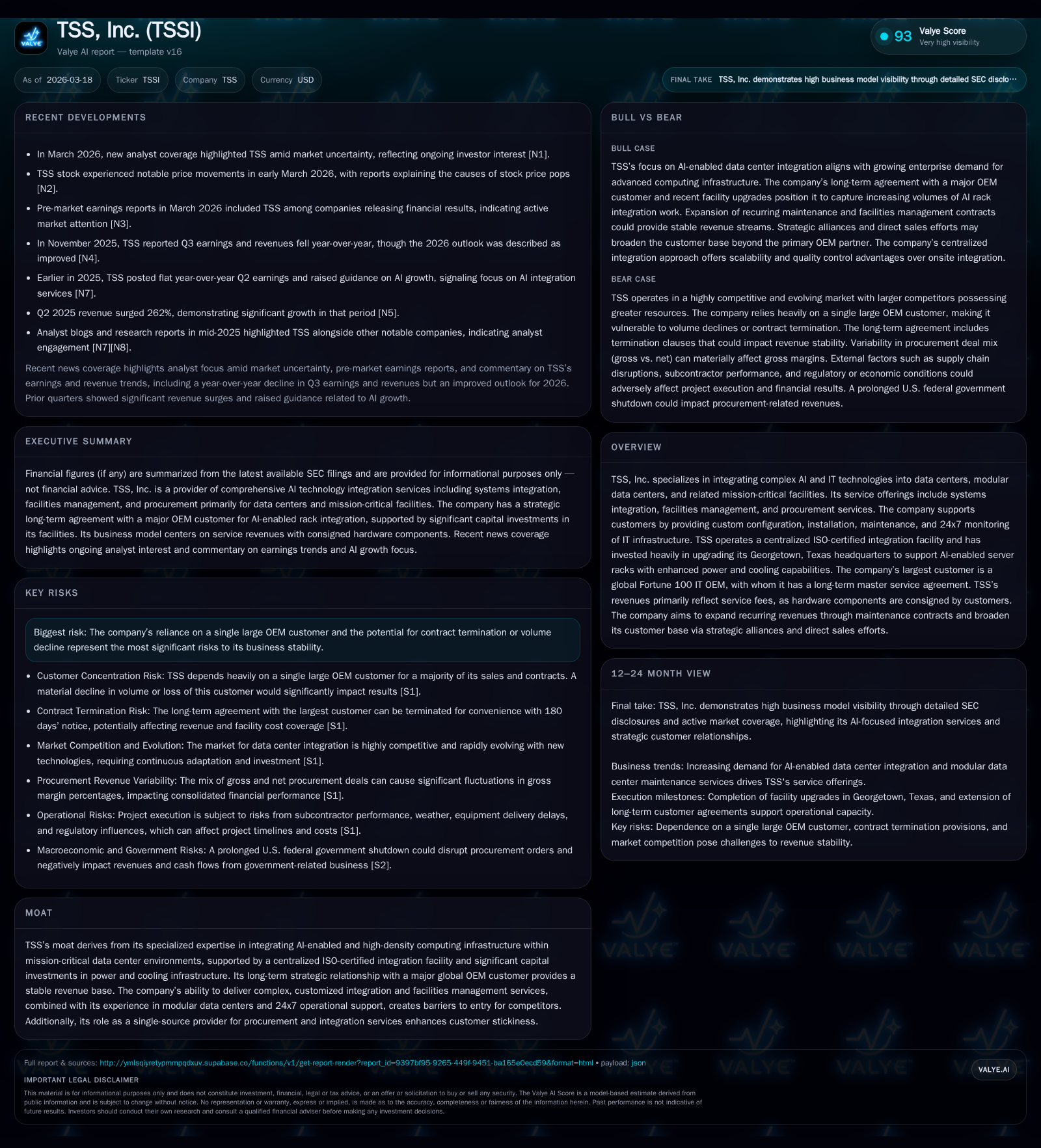

TSS, Inc.'s Strategic Focus on AI Rack Integration Amid Concentrated Customer Dependency

TSS, Inc. leverages specialized integration capabilities and facility investments to serve AI-driven data center demands while navigating risks from its revenue concentration.

TSS, Inc. specializes in integrating AI-enabled server racks and managing mission-critical facilities, relying heavily on one Fortune 100 OEM customer that accounts for nearly all revenue. The company has invested over $40 million in a state-of-the-art integration facility to support advanced power and cooling requirements critical for AI workloads. While revenue surged sharply in 2025 driven by AI rack services, operating income declined partially due to increased fixed costs and pricing updates. TSS aims to diversify its customer base and increase recurring revenues through maintenance contracts, but the heavy dependence on a single client presents material risks tied to contract changes or volume fluctuations.

Company Overview and Market Position

TSS, Inc. operates at the intersection of cutting-edge AI infrastructure deployment and mission-critical data center services. It has carved out a niche specializing in integrating complex Artificial Intelligence (AI) enabled computing hardware into data centers, modular data centers (MDCs), and similar facilities pivotal for today’s accelerated computing environment [S1][S17]. Its core offerings encompass systems integration services focused largely on custom AI rack configurations, facilities management including deployment and maintenance of MDCs, as well as procurement of hardware and software solutions.

The company’s strategic decision to consolidate its operations into a new, larger ISO-certified integration facility in Georgetown, Texas represents a key competitive differentiator. This $40 million investment enhances electrical power availability and advanced cooling capabilities—both air-cooled and direct liquid cooled (DLC)—tailored for the rapidly growing demand for dense AI server racks [S11][S16][S19]. These infrastructural improvements underscore TSS’s positioning as an end-to-end integrator uniquely prepared to meet the evolving technical complexity of next-generation generative and inferencing AI systems.

Historical Performance: Growth Trajectory Fueled by AI Integration

TSS experienced exceptional revenue growth in recent years with revenues increasing from approximately $148 million in 2024 to $246 million in 2025—an impressive 65.9% increase supported heavily by expanded AI rack integration services secured through a long-term master service agreement with a global Fortune 100 IT OEM [F1][S16].

Despite top-line growth, operating income declined by about 25.6% from $8.5 million in 2024 to $6.3 million in 2025 due primarily to increased fixed costs associated with the new Georgetown facility and updated pricing terms reflecting higher power consumption demands [F1][S16]. However, net income rose significantly to $15.1 million in 2025 from $6 million in the prior year, reflecting operational leverage, improved cost management, or possibly non-operating factors [F1]. Operating cash flow more than doubled year-over-year reaching nearly $35 million—indicating strong cash conversion during capital expenditures [F1]. This liquidity supports ongoing service innovation and balance sheet strength.

Historical performance (annual)

| FY | Rev ($mm) | Net ($mm) | CFO ($mm) | OpInc ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 246 | 15 | 35 | 6 | +65.9% | +153.1% |

| 2024 | 148 | 6 | 15 | 9 | +7975.7% | |

| 2023 | 0 | -8 | 2 | +201.4% | ||

| 2022 | 0 | 15 | 1 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Buybacks ($mm) | ROE% |

|---|---|---|

| 2025 | 5 | 19.7 |

| 2024 | 4 | 83.7 |

| 2023 | 0 | 2.1 |

| 2022 | 0 | -2.5 |

Source: SEC companyfacts cache [F1].

Note: Capex details available qualitatively rather than numerically post-2012; buyback levels indicate modest capital returns.

Business Model Nuances & Customer Concentration

Unlike traditional hardware vendors, TSS's revenue model predominantly reflects service fees since customers consign most hardware components for integration; thus revenues recognize only the value-added labor and services performed [S4][S22]. This contributes to relatively stable gross margins but means top-line scales with activity volume rather than hardware sales.

The company’s dominant customer is a single large US-based OEM representing approximately 99% of revenues in recent years — an unusually high concentration that translates into substantial business risk should this relationship deteriorate [S1][S9][S16]. This OEM relationship includes a long-term AI rack integration agreement with guaranteed minimum monthly payments designed to offset fixed operating costs of the large integration facility [S16]. The amended contract extends its term with automatic renewals but allows termination for convenience with six months’ notice, leaving downside risk if volumes fall or contract terminates unexpectedly.

Efforts to diversify beyond this major OEM include expansion into procurement services acting as an agent or principal for third-party hardware/software purchases, targeting additional OEMs, value-added resellers, systems integrators, and MDC providers [S16][S15]. However, these initiatives are nascent and may require further investment before materially offsetting concentration risk.

Growth Drivers & Constraints

Future growth hinges significantly on continued adoption of high-density AI-enabled server racks requiring advanced power/cooling solutions that only select integrators like TSS can provide effectively [S17][S19]. The relentless pace of generational increases in GPU count per rack and corresponding energy needs underpins sustained demand for TSS’s system integration expertise.

Expanding recurring maintenance contracts on existing MDCs also holds promise for steadier revenue streams as annual maintenance revenues rise relative to new build cycles—although industry-wide trends showed more retirements than deployments recently [S18][S26].

Geographic concentration remains primarily domestic US with no significant international exposure noted [S4][S17]. Strategic alliance building within IT consulting firms and technology providers is designed to broaden solution offerings but must translate into customer wins [S11]. Competitive pressure exists from larger IT service firms capable of bidding aggressively yet TSS leverages its specialized focus and quality controls within its centralized ISO-certified facility [S11][S23].

Constraints include potential OEM strategic shifts reducing purchase volumes due to supply chain delays or product demand changes as well as the unknown trajectory of future AI rack power consumption challenging infrastructure scalability without further capital outlays [S9][S16].

Capital Allocation & Financial Health

The company's liquidity position appears robust with approximately $85 million cash/equivalents against current liabilities near $72 million yielding a healthy current ratio above 1.6 as of December 31, 2025 [F1]. This cash buffer underpins working capital needs amid factoring arrangements used creatively to mitigate extended payment terms from large customers [S7][S24]. The factoring program enables effective receivables conversion at favorable rates compared with borrowing costs.

Long-term debt reached $20 million drawn from a credit agreement established end-2024 primarily financing the Georgetown facility build-out—with amortizing payments starting mid-2025 tied to floating SOFR plus spread terms [S6][S10]. The debt covenants impose leverage limits tightening progressively through September 2026 onward [S10].

Modest share repurchases have been executed recently ($4.9 million in FY25), indicating some return of capital focus alongside reinvestment priorities [F1]. Return on equity approached ~19.7% in FY25 reflecting efficient net income generation relative to equity base after several years rebuilding positive earnings momentum [F1].

Risks Summary

- Customer Concentration: With roughly 99% revenue dependency on one global Fortune 100 IT OEM with termination rights subject to six months’ notice; any change could cause severe adverse financial impacts including underutilization of fixed-cost heavy infrastructure [S1][S9]. This concentration overshadows other risks.

- Facility Fixed Costs & Debt Obligations: High fixed charges from large new facility investments mean downturns will disproportionately impact profitability if volumes fall below committed minimums without contractual relief [S16][S19].

- Power & Cooling Demand Uncertainty: Future server rack power needs remain uncertain; inability to match infrastructure capacity could limit ability to secure new contracts or retain existing ones under evolving tech standards [S9][S16].

- Competitive Landscape: Presence of larger established IT integrators creates pricing pressure; size constraints may limit ability to bid on very large projects reducing growth opportunities [S11][S23]. Quality differentiation via centralization partially mitigates this.

- Cybersecurity Threats: Handling sensitive high-value systems makes TSS vulnerable to cyber incidents affecting operations or client trust; reliance on subcontractors adds complexity risk in delivery assurance [S23].

- Contractual Cancelations: Most agreements aside from the core rack integration deal permit short-notice cancellation limiting revenue visibility outside that primary contract [S18].

Outlook & What to Watch

Explicit guidance was not provided; however key metrics indicative of trajectory will include:

- Progress on diversifying client base beyond the main OEM customer.

- Utilization rates at the Georgetown integration center relative to operating leverage.

- Expansion traction in recurring maintenance contract book versus one-time project revenues.

- Developments around updated pricing structures reflecting AI rack power intensities.

- Management commentary on potential new strategic partnerships or technology acquisitions aligned with expansion plans.

- Impact of economic environment or government shutdowns affecting procurement orders per prior disclosures given some government-related procurement exposure [N1][N2][N3].

Conclusion

TSS stands at a technologically sophisticated intersection supporting enterprise-scale AI infrastructure rollouts via deeply integrated systems expertise fortified by significant capital investment into purpose-built facilities embracing next-gen thermal management innovations. The pronounced dependency on one principal OEM forms both a reliable revenue cornerstone via long-term minimum payment agreements as well as a material vulnerability should commercial dynamics shift unfavorably.

Growth prospects rooted in proliferating demand for complex AI server racks coupled with service expansion into maintenance contracts provide pathways toward steadier recurring revenue streams yet require successful diversification execution over coming years alongside sustained operational excellence.

This analysis synthesizes publicly filed financial documents including SEC filings up through March 18, 2026 ([F1],[S1]-[S29]), alongside recent market commentary ([N1]-[N3]). It does not constitute investment advice but aims to offer an informed internal perspective on TSS Inc.’s current status and strategic challenges within its specialized sector niche.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments