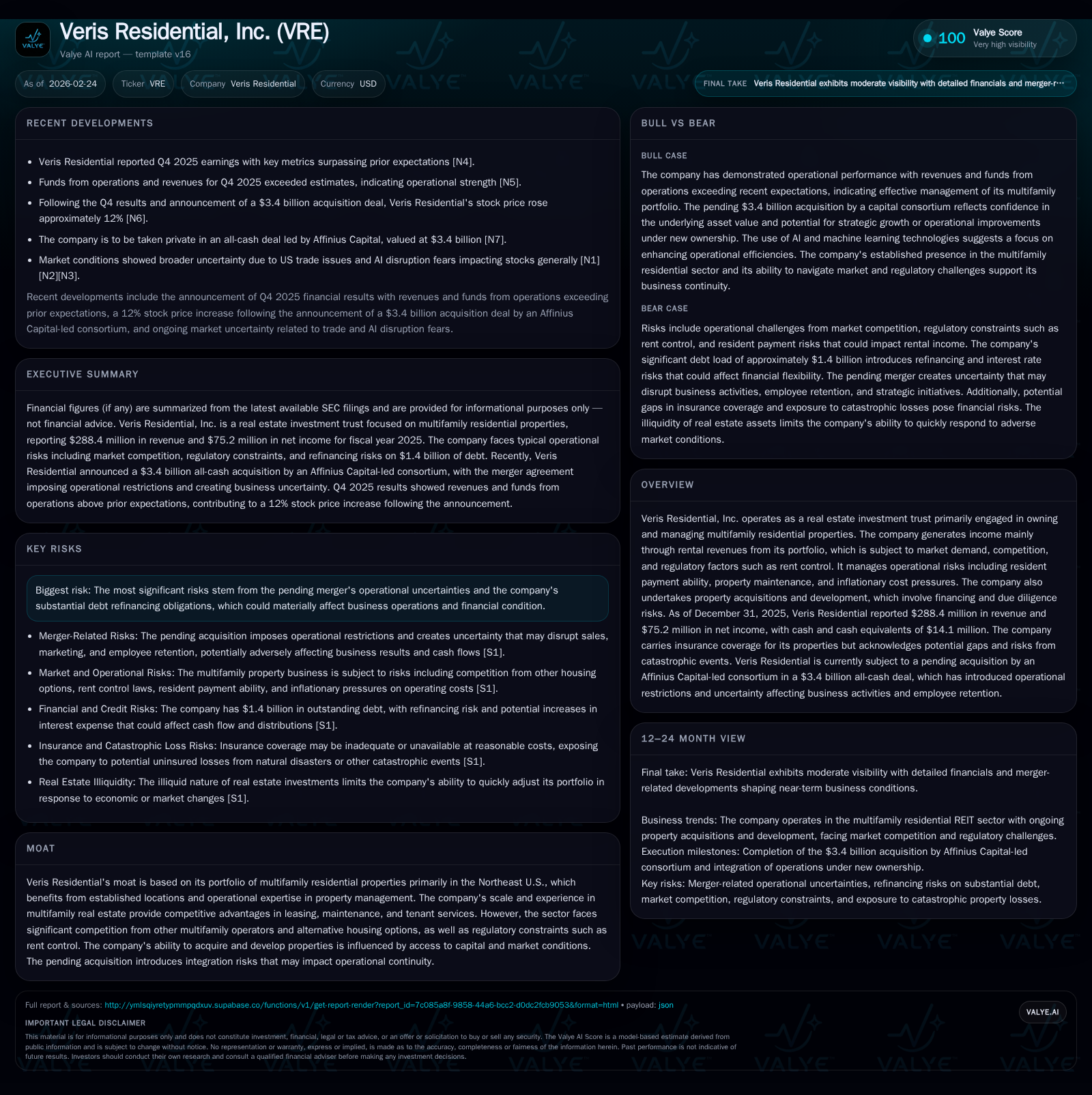

Veris Residential's Turnaround: From Losses to Acquisition Premium

Veris Residential recovered from multi-year net losses to post a significant profit in 2025, catalyzing a $3.4 billion acquisition offer.

After enduring a stretch of net losses between 2022 and 2024, Veris Residential reversed course with $75.2 million of net income in 2025, driven by operational improvements and focused portfolio management. This turnaround set the backdrop to Affinius Capital-led consortium's all-cash $3.4 billion acquisition offer, which has significantly boosted the stock price but raised integration and refinancing uncertainties. The company's capital structure shows rising leverage with $1.4 billion in debt, imposing refinancing risks amid rising interest rates and mortgage covenants. While buybacks have been modest and dividends restricted under merger terms, future growth hinges on successful deal closure and regulatory navigation in the Northeast multifamily market.

From Deficits to Profitability: Veris Residential's Historical Performance and Growth Drivers

Veris Residential executed a notable financial turnaround as it emerged from consecutive years of steep net losses towards profitability in fiscal year 2025. After posting net losses of approximately -$52 million in 2022, -$107 million in 2023, and -$23 million in 2024, the company reported net income of $75.2 million for the full year ending December 31, 2025 [F1]. This inflection was achieved despite a revenue base ($288.4 million) that was only moderately higher—up about 6.4% year-over-year—from the prior year’s $271.1 million.

Key drivers included active portfolio optimization focusing on high-demand multifamily residential properties concentrated primarily in the Northeast U.S., where leasing velocity gained traction despite persistent inflationary pressures impacting maintenance and operational expenses [S1]. Cost management measures combined with improved rent collections contributed positively amid regulatory challenges like rent-control policies constraining rapid rent increases [S8]. Operating cash flow corroborated this progress, improving by roughly 45% from $52.3 million in 2024 to about $75.9 million in 2025 [F1], signaling enhanced cash earnings quality alongside nominal top-line expansion.

Historical performance (annual)

| FY | Rev ($mm) | Net ($mm) | CFO ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|

| 2025 | 288 | 75 | 76 | +6.4% | +425.4% |

| 2024 | 271 | -23 | 52 | -3.1% | +78.4% |

| 2023 | 280 | -107 | 46 | -21.2% | -106.0% |

| 2022 | 355 | -52 | 66 |

Note: Omitted columns lack sufficient annual XBRL coverage in the provided tags (need ≥2 annual points): OpInc, Capex, Div, FCF. Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Buybacks ($mm) | ROE% |

|---|---|---|

| 2025 | 0 | 6.5 |

| 2024 | 0 | -2.1 |

| 2023 | 0 | -9.4 |

| 2022 | 3 | -4.2 |

Source: SEC companyfacts cache [F1].

Note: Operating income is unavailable for consistent annual comparison; dividend payment data are not available from provided tags.

Acquisition Announcement Sparks Stock Surge and Raises Integration Questions

On February 23, 2026, Veris Residential disclosed a definitive agreement whereby an Affinius Capital-led consortium will acquire the company for approximately $3.4 billion in an all-cash transaction [N2][N10]. The news immediately propelled the stock higher by about 12% on heavy volume [N1], signaling investor approval of the premium valuation implicit in this takeover.

The merger agreement restricts Veris’s ability to engage in major strategic initiatives or pursue new property acquisitions pending deal closure—actions necessary to preserve deal economics but potentially disruptive to growth momentum [S10][S15]. Moreover, sizeable integration risks loom around employee retention amid organizational uncertainty as well as continuity of key tenant relationships critical to maintaining operational cash flow post-transaction [S1]. The prospect of merger-related termination fees of up to $60 million also places a high premium on timely closing without regulatory or financing hiccups [S12].

Navigating Financial Structure Risks Amid Growing Leverage and Refinancing Needs

Despite its recent profit resurgence, Veris carries approximately $1.4 billion gross debt as of end-2025 including revolving credit facility borrowings (~$30 million) and roughly $1.3 billion in secured mortgages and loans payable [F1][S6]. About $185 million bear variable rates but are hedged against interest rate fluctuations [S7]. Nonetheless, ongoing refinancing risk persists given prevailing interest rate volatility and stringent mortgage covenants limiting lien expansions, lease modifications beyond stipulated guidelines, and additional secured borrowings without lender consent [S7][S10].

These covenants raise operational leverage concerns typical of real estate investment trusts where debt structures can compress flexibility during periods requiring costly capital replenishment or strategic repositioning [S6][S7]. Failure to comply could trigger defaults with potentially severe ramifications including foreclosure risk or accelerated debt repayment demands possibly forcing asset sales under pressure [S7].

Capital Allocation Patterns: Balancing Buybacks, Dividends, and Funding Growth

Capital allocation highlights a conservative stance amidst transitional uncertainty with only modest share buybacks totaling approximately $456 thousand in fiscal year 2025 after no repurchases in prior year [F1]. This restrained approach aligns with transactional lock-up imposed by the merger agreement limiting dividend distributions (capped at regular quarterly payments not exceeding $0.08 per share through Q1-26) while preserving REIT status compliance through mandatory distributions [S15][S25]. Specific dividend payment amounts are not disclosed in provided data.

Veris continues relying on external capital sources—such as equity offerings initiated via At-The-Market programs launched late-2023—and debt financing to fund property acquisitions and development ventures [S4][S25]. Such programs inherently carry dilution risks for existing shareholders but remain necessary given internal earnings insufficiency for organic expansion constrained by mandatory REIT distribution obligations [S4].

Outlook Post-Acquisition: Growth Prospects and Operational Constraints

The company’s forward trajectory hinges on completion of the privatization deal which promises strategic recalibration freed from public market scrutiny but entails near-term restrictions on capital deployment arising from merger covenants preventing new investments until closing completion [N2][S15]. Regulatory factors unique to Northeast U.S.—including evolving rent control frameworks—alongside intensifying competition from other multifamily operators as well as single-family rentals form structural headwinds capping potential rental rate escalations even during recovery phases [S8].

Operationally, merger closure could unlock efficiencies via scale consolidation though success depends on mitigating integration risks notably those related to workforce stability and tenant retention amid transitional noise [N10][S1]. Failure to consummate the acquisition would expose Veris to share price downside risks reflecting reversion from premium valuation levels plus costs incurred during the bidding process including potential $60 million termination penalties [S12][S15].

Key Metrics to Watch: Earnings Quality, Cash Flow Stability, and Deal Milestones

Market participants should closely monitor sustained operating cash flows relative to debt servicing obligations given Veris’s leveraged position; continued improvement would confirm earnings quality underpinning standalone viability amid refinancing cycles [F1]. Deal-related milestones such as shareholder approvals (requiring majority vote), absence of adverse regulatory rulings or material adverse effects clauses activation will temper timing risk around closure expected within next fiscal quarters [S15][N10].

Additionally, scrutiny will focus on realized net income trends verifying persistence beyond one-time gains linked to milestone accounting adjustments or transaction-related benefits reported alongside recent quarters’ results [N3][N8]. Investor sentiment post-announcement remains fragile due to geopolitical macro factors affecting broader risk assets though VRE’s fundamentals have registered positive momentum since acquisition disclosure [N1][N4][N6].

Missing Metrics Disclosure

Data for dividends paid during fiscal years are not available from provided XBRL company facts tags; likewise, detailed operating income figures for recent years are limited or unavailable for consistent trend analysis across all periods.

Disclaimer: This report is for informational purposes only and does not constitute investment advice or a recommendation regarding Veris Residential, Inc., its securities or related financial instruments. It synthesizes publicly available filings and news without making projections beyond documented statements or engaging in speculative forecasts.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments