Westwater Resources Advances Patented Graphite Plant as FCA Offtake Termination Delays Debt Funding

Westwater pushes forward with Kellyton plant build and eco-friendly purification despite offtake disruption, raising equity and seeking government support amid rising losses and negative cash flow.

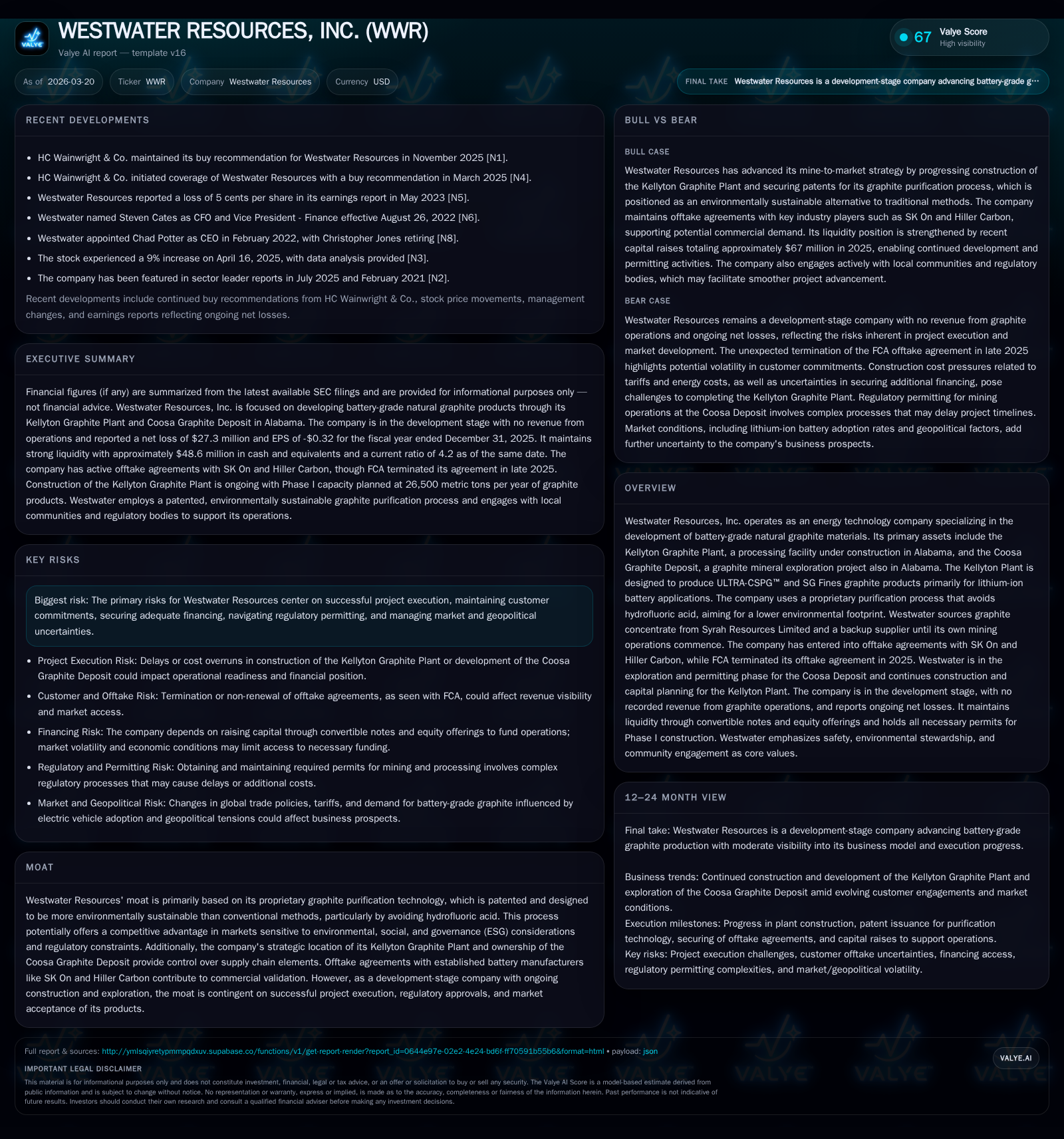

Westwater Resources, Inc. is an energy technology company focused on producing battery-grade natural graphite materials using patented environmentally friendly purification processes. The company’s Kellyton Graphite Plant in Alabama is under construction, aiming to supply lithium-ion battery manufacturers with its ULTRA-CSPG™ products. Despite advances in plant construction and patent issuance in 2025, the unexpected termination of a key FCA offtake agreement has paused planned debt syndication efforts, compelling Westwater to rely on equity financings and explore government-backed funding alternatives. As a development-stage entity, the company continues to post net losses and negative cash flows while strategically managing capital raising and operational readiness for commercial production.

Company Overview

Westwater Resources, Inc. is an energy technology company specializing in battery-grade natural graphite materials crucial for lithium-ion batteries. Its core assets include the Kellyton Graphite Plant — a graphite processing facility under construction in Alabama — and the Coosa Graphite Deposit mineral exploration project also located in Alabama. Westwater's proprietary ULTRA-CSPG™ graphite products use a patented purification process that notably excludes hydrofluoric acid, thereby reducing environmental hazards compared to traditional methods [S1].

Historical Growth and Operational Performance

Westwater has not reported operational revenues from its battery-grade graphite business segment since at least 2019 but has focused on developing its supply chain infrastructure including raw material sourcing arrangements pending commencement of mining operations at Coosa [S1]. The company remains in a development stage with consistent net losses.

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | Net YoY |

|---|---|---|---|

| 2025 | -27 | -10 | -115.9% |

| 2024 | -13 | -6 | -63.3% |

| 2023 | -8 | -11 | |

| 2022 | -13 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | ROE% |

|---|---|

| 2025 | -15.1 |

| 2024 | -9.5 |

| 2023 | -5.5 |

| 2022 |

Source: SEC companyfacts cache [F1].

Note: CFO = Cash Flow from Operations; Equity represents shareholders' equity at fiscal year-end; Revenue is zero due to pre-revenue status as disclosed [F1][S1][S5].

Net losses escalated sharply in 2025 to $27.3 million from $12.7 million the prior year—more than doubling—driven largely by expanded operating expenses related to plant construction progress and corporate costs [F1]. Operating cash flow remained negative at nearly $9.9 million indicative of ongoing burn typical for a company transitioning from development into commercial production phases.

Advancement of Graphite Business: Strategic Developments

Kellyton Graphite Plant Construction Progress

During 2025:

- Cumulative capital invested reached approximately $128.2 million as of December 31.

- The original Phase I budget was about $271 million but was optimized down to approximately $245 million after engineering reviews and debottlenecking measures.

- Cost pressures from geopolitical tariffs and elevated energy prices have kept management’s cost estimate steady at $245 million despite further optimization potential.

- Installation and commissioning of key equipment such as micronization and spheroidization mills advanced qualification line capabilities producing over one metric ton of CSPG samples for customer evaluation [S1].

Proprietary Purification Technology & Intellectual Property

On September 17, 2025, Westwater secured its first U.S. patent covering its proprietary hydrofluoric acid-free graphite purification method [S1]. This innovation enhances the company's environmental credentials amid increasing regulatory scrutiny on hazardous chemical usage.

Coosa Graphite Deposit Exploration & Permitting

Permitting activities progressed in late 2025 including filing for a National Pollutant Discharge Elimination System permit with Alabama regulators as part of advancing potential future mine development [S1]. Drilling programs continued with external support aligned with a mine-to-market strategy supporting domestic critical minerals policies.

Customer Engagement & Offtake Agreements

Binding offtake agreements remain active with SK On and Hiller Carbon securing initial commercial outlets; however, FCA unexpectedly terminated its agreement in November 2025 which had been expected to underpin planned debt financing efforts [S1]. The termination led to pausing planned secured debt syndication tied closely to FCA support. The company continues supplying samples and pursuing additional customer opportunities.

Capital Structure & Capital Raising Activity

Liquidity Position

At year-end 2025, Westwater held approximately $48.6 million in cash equivalents against current liabilities near $11.6 million resulting in a current ratio around 4.2 [F1][S5], providing reasonable short-term liquidity though substantial funding will be required to complete plant construction.

Financing Sources

In response to capital needs stemming from remaining Phase I expenditures (~$117 million), Westwater raised approximately $67 million during 2025 through:

- Convertible Notes offerings totaling $10 million (Series A-1 & B-1 Convertible Notes).

- Equity raises via ATM Sales Agreement with H.C. Wainwright and Lincoln Park equity financing agreements. These inflows supported ongoing equipment acquisition and permitting work despite suspension of debt syndication following FCA's contract termination [S1][S4][S13][S16][S17].

Convertible Notes Terms

Convertible notes contain customary covenants limiting beneficial ownership below approximately 10% per holder upon conversion with no accruing interest except during default periods where it rises to punitive rates (18%). Maturity occurs within two years if not converted [S12][S16]. Shares have been issued upon note conversions adjusting carrying amounts accordingly [S15].

Financial Performance Outlook & Risks

While explicit forward guidance is not provided given the developmental stage, management highlights near-term priorities:

- Completion of Kellyton Phase I construction contingent on securing additional funding beyond current cash reserves.

- Aggressive pursuit of permitting approvals for Coosa mining operations alongside construction progress.

- Expansion of customer base through qualification ramp-up with product performance validation essential.

- Necessity of diversified off-take agreements due to FCA departure impacting credit perceptions.

- Exposure to energy price volatility and trade policy uncertainties influencing capital planning flexibility.

- Anticipation of further equity or debt financings as operating losses continue until commercial production begins [S1][S20].

Returns & Capital Allocation Strategy

No dividends or share repurchases have been declared or paid given Westwater’s pre-revenue status and capital-intensive investment profile [F1][S19]. Capital allocation focuses on maintaining liquidity through equity issuances alongside convertible debt instruments that convert into stock rather than incurring cash interest payments.

Industry Context Analysis

Battery-grade graphite is critical for electric vehicle growth where suppliers face tightening environmental regulations restricting hazardous chemicals like hydrofluoric acid used traditionally in purification processes. Westwater's HF-free method aligns well with expected ESG compliance trends among North American lithium-ion battery manufacturers seeking secure local supply chains amid geopolitical trade tensions affecting global graphite supply dominated by China.

Successful scale-up from pilot to commercial production remains challenging especially for juniors requiring significant capital expenditure amid fluctuating investor risk appetite. The loss of FCA’s commitment illustrates typical commercial volatility faced by critical minerals start-ups balancing innovation against execution risk.

Summary Table: Financial Highlights (USD thousands)

| Metric | FY2019 | FY2024 | FY2025 |

|---|---|---|---|

| Revenue | 0 | NA | NA |

| Net Income | -10,565 | -12,657 | -27,326 |

| CFO | -11,430 | -5,814 | -9,897 |

| Cash & Eq | 3,675 | 4,272 | 48,576 |

| Current Liab | NA | NA | 11,622 |

| Equity | 141,968 | 133,122 | 181,529 |

| Current Ratio | NA | NA | ~4.2 |

Closing Thoughts

Westwater Resources exemplifies a development-stage ESG-focused critical minerals producer aiming to secure U.S.-based clean battery materials supply through innovative processing technology. Recent milestones include patent protection and plant construction progress but challenges such as loss of key customer support complicate financing pathways. Market acceptance will depend on successful execution at Kellyton alongside permitting progress at Coosa plus securing diversified off-take contracts within a competitive strategic battery materials sector shaped by evolving trade dynamics and energy transition mandates.

This report is prepared solely for informational purposes based on publicly available SEC filings [F1][S#] without offering investment advice or recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments