Zion Oil & Gas Faces Capital Intensity and Geopolitical Risks in Israeli Onshore Exploration

Despite technology advances and a strategic foothold, Zion's path to production hinges on financing amid regional instability.

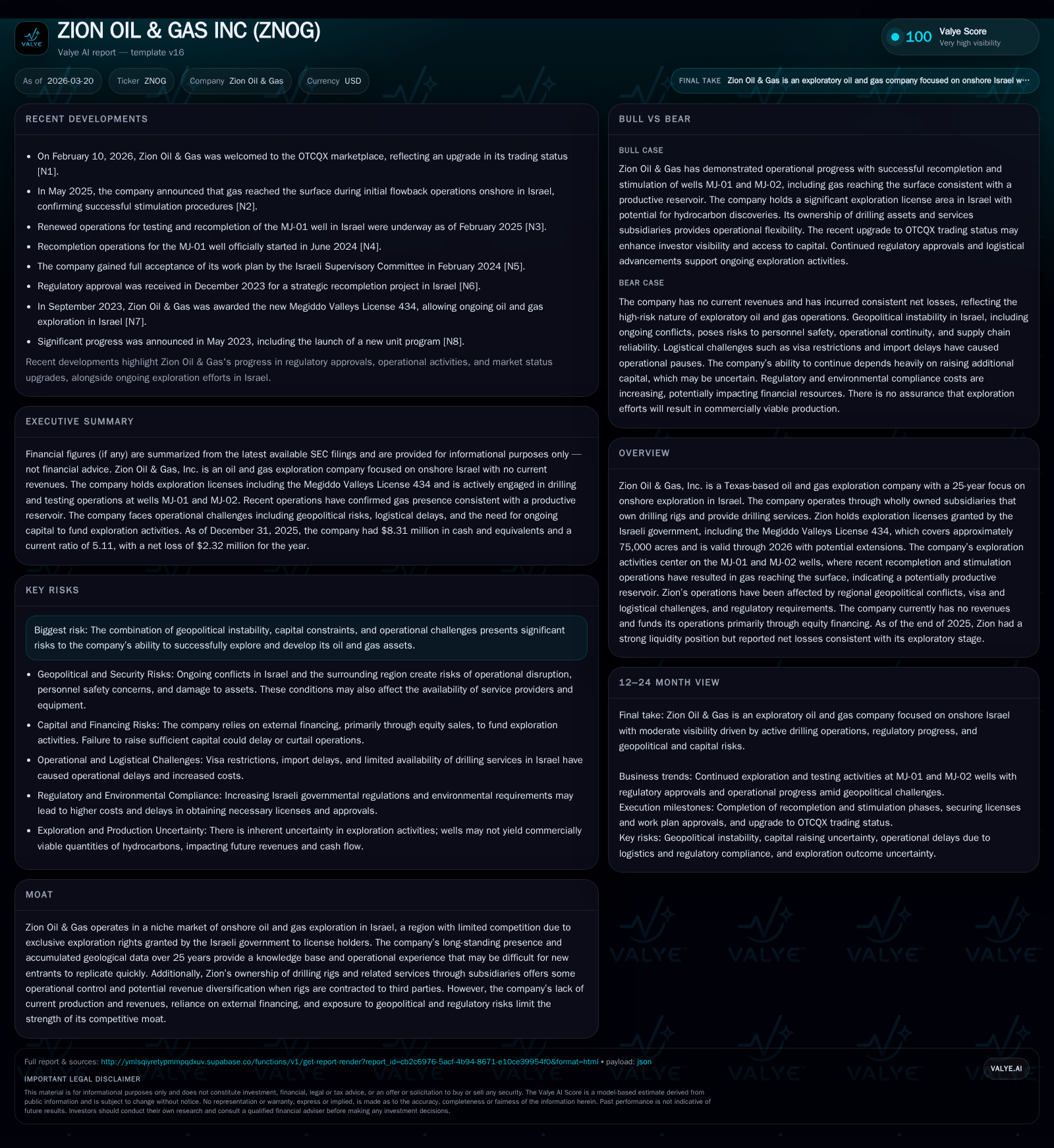

Zion Oil & Gas has focused for over 25 years on onshore oil and gas exploration in Israel, operating under exclusive licenses granted by the Israeli government. The company holds extensive acreage but currently generates no revenue, relying heavily on equity sales to fund costly exploration programs. Recent recompletion efforts at its MJ-01 and MJ-02 wells have shown promising gas flows, yet commercial viability remains uncertain. Zion contends with complex regulatory landscapes, visa constraints, and geopolitical risks that could delay operations and inflate costs. Its financials reveal sustained net losses, negative operating cash flow, and substantial capital requirements ahead. The company’s future growth depends critically on successful drilling outcomes and continued access to capital.

Historical Financial Performance and Growth Drivers

Zion Oil & Gas, incorporated in 2000 with its corporate home now in Texas as of mid-2025, has dedicated over twenty-five years to exploring onshore Israeli hydrocarbon potential [S1]. Its primary asset is the Megiddo Valleys License 434 (NMVL 434), encompassing approximately 75,000 acres, valid until late 2026 with possibility of multiple one-year extensions through 2030 [S1][S27]. This exclusive license framework limits competition within its acreage but adds risk related to license renewal.

Financially, Zion remains an exploration-stage entity with zero revenue reported for the past years including fiscal 2025 [F1]. Operating losses have hovered around $7.3 to $7.7 million annually from 2024 to 2025 without meaningful improvement (operating income: -$7.7M in FY25 vs -$7.3M in FY24), reflecting intensive expenditures associated with exploration activities [F1]. Net losses similarly demonstrate modest year-over-year deterioration (net loss of -$2.3M in FY25 vs -$1.7M in FY24) although smaller than operating losses due to non-operating adjustments [F1].

Operating cash flow paints a more challenging picture with negative figures amounting to approximately -$8 million in FY25 [F1]. The company’s Capex dropped steeply (~94% YoY), signaling perhaps deferred or reduced asset additions in line with funding constraints [F1][S12][S13]. Equity rose from $28.4 million in FY24 to $42.4 million in FY25 due to successful equity raises primarily conducted through the Dividend Reinvestment and Stock Purchase Plan (DSPP) [F1][S6][S8].

Historical performance (annual)

| FY | Rev | Net ($mm) | CFO ($mm) | OpInc ($mm) | Net YoY |

|---|---|---|---|---|---|

| 2025 | 0 | -2 | -8 | -8 | -33.0% |

| 2024 | 0 | -2 | -6 | -7 | +78.1% |

| 2023 | -8 | -5 | -8 | +85.6% | |

| 2022 | -55 | -6 | -55 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2025 | -5.5 | |

| 2024 | -6.2 | |

| 2023 | -5 | -36.1 |

| 2022 | -6 | -238.4 |

Source: SEC companyfacts cache [F1].

Financial data via [F1]

Operational Overview and Exploration Efforts

Zion operates wholly owned subsidiaries owning drilling rigs and providing services domestically within Israel – this vertical integration offers some operational flexibility absent from many pure explorers [S1]. Through these entities — Zion Drilling Inc., Zion Drilling Services Inc., and Zion Drilling Israel Ltd — it maintains equipment and personnel readiness for ongoing work as well as possible third-party contracts [S1].

Exploration activity centers on re-entry and stimulation of MJ-01 and MJ-02 wells located within NMVL 434. In mid-2025 after substantial technical efforts including perforation and stimulation techniques using new technologies tailored for Israeli geological conditions (e.g., multi-stage horizontal fracturing), natural gas was successfully brought to surface during flowback operations—marking a significant milestone as it confirmed the presence of productive reservoirs [S27]. However commercial quantities remain unproven.

The MJ-02 well will serve as a starting point for follow-up operations featuring advanced horizontal drilling strategies aimed at targeting multiple zones within the reservoir effectively [S26]. Success here is crucial for advancing from exploratory phase to feasibility assessments.

Growth Prospects and Operational Constraints

Growth prospects depend primarily on successful conversion of current acreage into commercially viable production assets. Yet significant operational headwinds constrain this path:

- Geopolitical Instability: Continuous regional conflict including wars involving Hamas and Hezbollah raise security risks that can delay operations or damage infrastructure [S26][S28].

- Regulatory Complexity: Israeli licensing involves multiple local authority approvals beyond energy ministry endorsement—ranging from environmental planning commissions to military zones—lengthening timelines substantially [S22][S28]. Newly enacted regulations impose stricter environmental stipulations and require performance bank guarantees amounting to roughly 10% of planned drilling costs locked in restricted deposits [S26].

- Visa and Labor Challenges: Changes in Israeli visa policies delay crew deployment critical for drilling schedules; rig personnel require periodic renewals complicated by recent policy shifts from calendar-year resets to six-month post-expiration resets [S27][S26].

- Financial Constraints: Ongoing exploration is capital-intensive; current cash balances are sufficient only through March 2027 assuming no major acceleration or unexpected costs [S8][S26]. Any shortfall necessitates capital raises that may dilute shareholders significantly given no current revenues or reserves.

Milestones and What To Watch

Key milestones include:

- Completion of mandated regulatory inspections including five-year rig recertification ensuring compliance with national/IADC standards before resuming full-scale drilling at MJ-02 [S26].

- Execution of horizontal sidetrack drilling targeting reservoir zones within MJ-02 wellbore expected post-inspection phase.

- Ongoing evaluation of gas test data quality from prior flowback which informs technical decisions about next well stimulations or sidetrack attempts.

- License extensions beyond September 2026; potential use of annual extension options would impact timing of development decisions [S27].

No explicit forward guidance is disclosed regarding production timelines or reserves conversion probabilities; thus market participants should monitor operational updates closely alongside geopolitical developments affecting the region's stability.

Capital Allocation and Returns Profile

Zion does not pay dividends nor currently generates positive free cash flow; all investment proceeds are directed toward operational expenditures required for exploration licensing maintenance or drilling campaigns [S15][F1]. Share repurchases are not part of the capital allocation strategy.

The company’s approximate return on equity based on latest net income attributable to shareholders against book equity stands near negative 5.5%, reflective of ongoing losses typical for early-stage explorers lacking revenue streams [F1]. Active dilution occurs through frequent sales of common stock via DSPP which accounted for the majority of financing during recent years raising above $21 million in fiscal 2025 alone [S6][F1]. Reliance on a small number of participants dominates these issuances posing concentration risk if participation declines.

Liquidity remains a material concern supported by:

- Cash & equivalents balance around $8.3 million at end-FY25 paired with high monthly expenditure rates ($600K when inactive versus up to $3M during active drilling) limits runway without new financing inflows [F1][S26].

- Auditor’s going concern note underscores inability to generate sustainable operation cash flows absent external funding or discovery commercialization near-term [F1][S6].

Industry Context Analysis

Onshore oil exploration in Israel is a niche sector characterized by complex geology combined with tight regulatory oversight influenced by environmental sensitivities and national security priorities. Unlike offshore Mediterranean projects operated by larger consortia involving international majors like Chevron/Delek Group who benefit from deeper pockets and experience offshore plays – Zion focuses exclusively on terrestrial sites where logistical challenges such as equipment importation delays increase cost structures disproportionately [S23].

Furthermore geopolitical risk premiums associated with Middle Eastern assets deter broader mainstream exploration investments compared with global peers focused on North America or the Gulf region hence smaller players predominate locally offering modest transparency relative to international benchmarks.

Despite global ESG pressures on fossil fuels there remains strategic importance for Israel pursuing indigenous energy resources substituting imports. Activism against hydrocarbon drilling imposes reputational risks possibly translating into stricter permit conditions or public opposition prolonging project timelines further impacting economics negatively [S20].

Summary Assessment

Zion Oil & Gas embodies a classic frontier exploration profile marrying unique geographic exclusivity with high execution risks inherent to deep wildcat drilling ventures far from traditional oil hubs. While incremental technical progress such as demonstrated gas flows bolster proof-of-concept status there remains an arduous path ahead before commerciality can be established.

The company’s survival hinges precariously on securing necessary funding rounds amidst an unforgiving political backdrop intensifying cost burdens due to heightened regulation and operational hurdles related primarily to workforce mobility constraints and supply chain intricacies specific to Israel’s limited oilfield service environment.

Its strategy leveraging ownership of rigs aims partly at mitigating outsized contractor availability risks seen locally but does not fully shield commercial prospect viability reliant on yet uncertain resource delineation outcomes.

Stakeholders should monitor developments regarding license extension approvals beyond September 2026 expiration date plus operational milestones like successful horizontal well production tests carefully – these factors will materially influence future valuations but remain contingent upon factors outside Zion’s direct control particularly external capital availability given persistent negative cash flows.

This report is prepared solely for informational purposes without regard to any person’s investment objectives. It does not constitute an offer or solicitation of securities nor investment advice.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments