Zura Bio's Growth Reliant on Phase 2 Clinical Progress Amid Rising R&D Expenses

Clinical-stage biotech Zura Bio concentrates on autoimmune treatments, facing escalating losses as it advances tibulizumab trials.

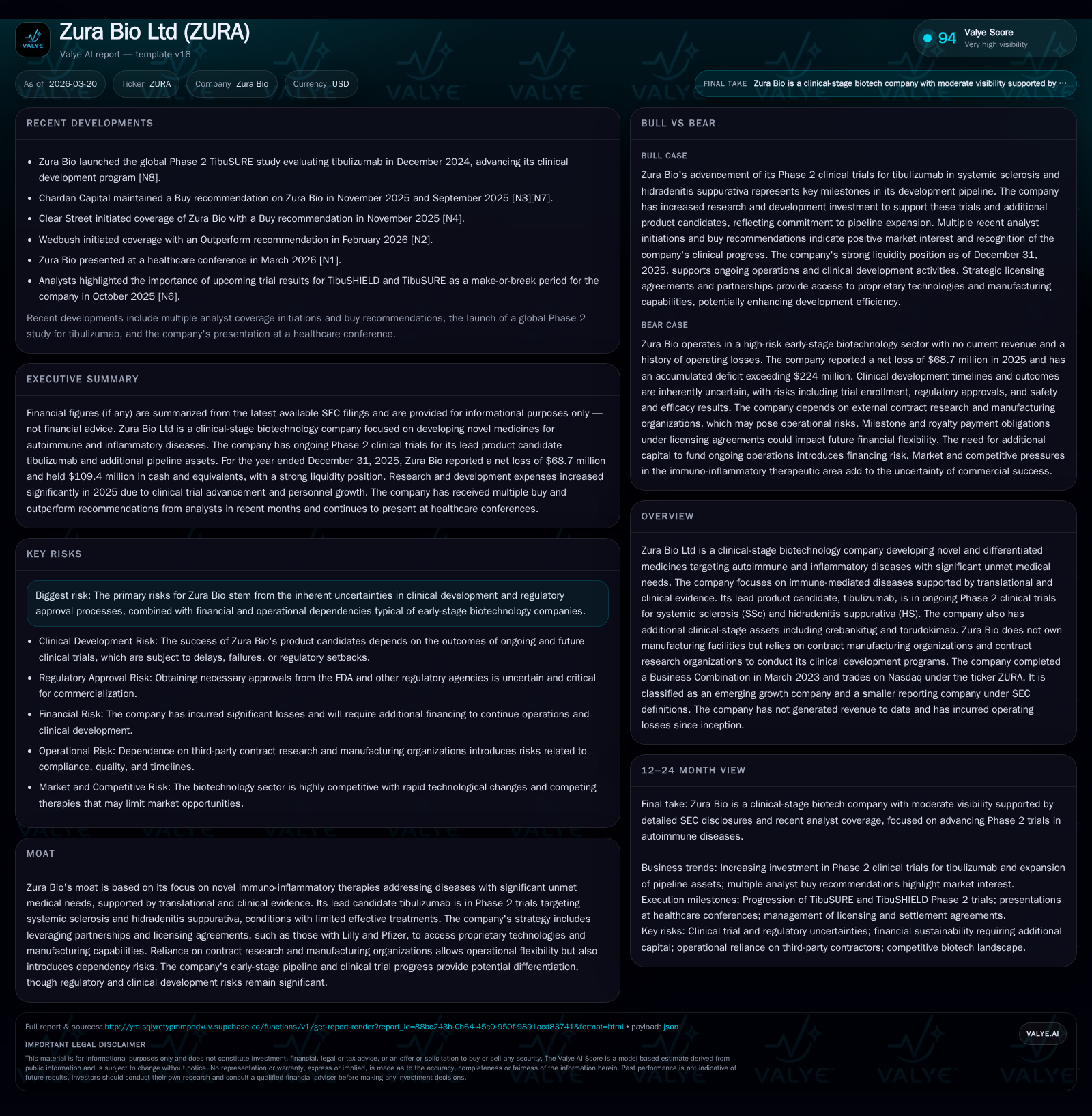

Zura Bio Limited operates as a clinical-stage biotechnology company focused on novel immuno-inflammatory therapies targeting autoimmune and inflammatory diseases with high unmet needs. Its lead asset, tibulizumab, is undergoing Phase 2 studies for systemic sclerosis and hidradenitis suppurativa. The company has incurred growing net losses driven by heightened research and development spending, relying on contract organizations for clinical development and manufacturing, and maintains sufficient liquidity to fund operations over the near term. Future growth hinges critically on clinical outcomes, regulatory approvals, and successful capital raising amid inherent biotech risks.

Company Overview and Strategic Focus

Zura Bio Ltd is a clinical-stage biotechnology firm specializing in the development of differentiated medicines for autoimmune and inflammatory disorders characterized by significant unmet medical needs. The company's scientific approach centers on targeting relevant biological pathways substantiated by translational data and clinical validation. Currently, its principal asset, tibulizumab, is actively advancing through Phase 2 clinical studies for systemic sclerosis (SSc) and hidradenitis suppurativa (HS), two debilitating indications with limited treatment options [S1][N1]. Additional assets under clinical evaluation include crebankitug and torudokimab, expanding the pipeline targeting immune-mediated diseases [S1].

Zura Bio operates without internal manufacturing or laboratory facilities, leveraging relationships with contract manufacturing organizations (CMOs) and contract research organizations (CROs), enabling operational flexibility but introducing reliance risks on external partners [S5]. Notably, partnerships with Lilly and Pfizer grant licensing access to proprietary technologies pivotal for their development programs but carry obligations for milestone payments potentially reaching multimillion-dollar levels upon regulatory milestones or sales thresholds [S6][S20][S27].

Historical Financial Performance

The company has experienced rapid increases in operating expenditures concomitant with clinical advancement since becoming publicly listed following a business combination closing in March 2023 [S15]. Annual operating losses have widened markedly: from approximately $26.8 million in FY2022 to roughly $62.6 million in FY2023, escalating further to $55.2 million in FY2024 and $75.2 million in FY2025 ([F1]).

Net income followed a similar trajectory with an inflection point shifting from a modest profit of around $3.5 million in FY2022 to sustained negative results thereafter—losses of about $60.4 million in FY2023 increasing to $52.4 million in FY2024 reaching $68.7 million in FY2025 ([F1]). This reflects acute investment into research programs without any commercial revenue inflows.

Research and development costs represent the largest cost component and have grown substantially reflecting ramped-up clinical activities. R&D expense jumped 72% year-over-year to roughly $42.1 million in FY2025 compared to approximately $24.4 million the prior year ([F1], [S19]). This increase predominantly arises from external CRO/CRO-related expenses tied directly to ongoing Phase 2 trials of tibulizumab for SSc and HS.

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($) | Net YoY |

|---|---|---|---|---|---|

| 2025 | -69 | -65 | -75 | 113000 | -31.0% |

| 2024 | -52 | -28 | -55 | 75000 | +13.2% |

| 2023 | -60 | -15 | -63 | -1800.7% | |

| 2022 | 4 | -1 | -3 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2025 | -65 | -67.6 |

| 2024 | -28 | -35.7 |

| 2023 | -101.7 | |

| 2022 | -46.5 |

Source: SEC companyfacts cache [F1].

Note: Revenue not reported as company remains pre-revenue; figures in thousands USD.

Future Growth Prospects

Growth prospects hinge fundamentally on successful clinical outcomes of current programs—most critically tibulizumab’s Phase 2 trials for systemic sclerosis and hidradenitis suppurativa. Positive efficacy and safety data can enable progression into pivotal trials which are essential for regulatory approval pathways [N1][S1]. The company’s expanded pipeline assets such as crebankitug could broaden future indications if they demonstrate therapeutic potential.

The licensing partnerships offer both technological leverage and potential financial exposure through milestone payments contingent upon successful clinical progression and potential commercialization achievements [S27]. This creates a dual-edged scenario where product successes could generate substantial future liabilities alongside opportunities.

Operationally, reliance on third-party providers introduces executional risk especially amid complex global supply chains common in biopharma—a sector where delays or quality issues at CROs/CMOs can materially disrupt development timelines.

Financial Forecasts and Milestones

While Zura Bio has provided no explicit forward-looking revenue guidance as it remains pre-commercialization [S1], key upcoming milestones developers will monitor include completion of interim Phase 2 data readouts for tibulizumab programs anticipated during ongoing trials that may shape developmental prioritization.

Liquidity management remains vital given escalating cash burn; however the firm reported cash balances of approximately $109.4 million at December 31, 2025—reducing from $176.5 million the prior year—in line with significant operating expenditures [F1]. Management indicates sufficient runway based on current liquidity to sustain operations over the ensuing twelve months [S9]. Analysts note capital raising activities including private placements totaling over $200 million since going public have underpinned operational funding without yet achieving profitability [S6][N2].

Returns and Capital Allocation

Given Zura Bio’s developmental stage status, there are no dividends or share repurchase programs active as of latest filings [S11][F1]. The company has reported no revenues or meaningful cash inflows from commercial activities—cumulative losses have translated into an accumulated deficit exceeding $224 million by end-2025 ([F1]).

Approximate return metrics such as ROE are deeply negative (circa -67% calculated via net loss over shareholder equity of roughly $101.5 million), reflecting substantial investments into R&D without offsetting earnings or revenue generation [F1]. Operating cash flow negativity (-$64.8M in FY2025) combined with modest capital expenditures (~$0.11M) confirms that all cash use principally supports research efforts rather than asset acquisitions or infrastructure expansion.

Capital structure currently comprises equity financing dominant position after numerous raises post-Business Combination closure; contractual obligations relating to licensing milestone payments could impact future resource allocation if product candidates achieve regulatory approvals triggering contingent payouts [S6][S27].

Industry Context & Competitive Positioning

Zura Bio’s emphasis on immune-mediated conditions aligns with a broader pharmaceutical industry trend targeting chronic inflammatory diseases leveraging biologics or immunomodulators—a highly competitive field populated by established large pharmas alongside emerging biotechs.

The drug development process entails prolonged timelines fraught with high attrition rates; thus the risk profile remains elevated with uncertainties around trial outcomes and subsequent regulatory reviews hereof influencing corporate valuation envelopes disproportionately . Strategic collaborations like those with Lilly/Pfizer represent critical value drivers but necessitate balancing royalty/milestone obligations versus access to innovative platforms.

The company’s mode of outsourcing manufacturing aligns with typical early-to-mid-stage biotech practices avoiding costly fixed capital investments while maintaining agility but risks service interruptions beyond direct control .

Risks Summary

Notable risks encompass:

- Clinical development failure or delays leading to capital depletion without resulting approved therapies,

- Regulatory approval uncertainties given complex disease targets,

- Financial dependency on successive capital raises amidst deepening cash burn,

- Potential contractual liabilities regarding milestone payments under partner licenses,

- External dependencies on CMOs/CROs affecting trial integrity or timelines,

- Intense competition within autoimmune diseases from established players employing advanced biologic approaches [S10][S16][N2].

Conclusion

Zura Bio Ltd stands as a dedicated emerging growth company aggressively investing in immuno-inflammatory therapeutic candidates exemplified by tibulizumab’s ongoing Phase 2 programs addressing hard-to-treat autoimmune indications. While the expanding R&D expense base manifests commitment to timely advancement of its pipeline assets supported by external partners like Lilly and Pfizer licensing ties, it simultaneously amplifies operating losses deepening the path toward eventual commercialization.

Maintaining sufficient liquidity through continued fundraising remains imperative against a backdrop of inherent development risks encompassing regulatory hurdles intrinsic to biotechnology innovation cycles. Critical forthcoming inflection points hinge upon successful midpoint trial results which will influence subsequent strategic decisions including potential late-stage campaign launches or diversification of pipeline focus areas.

Investors tracking Zura Bio should monitor upcoming clinical readouts closely alongside its cash burn rate trajectories given current negative free cash flow dynamics.

This analysis is based solely on information available as of March 20, 2026 from SEC filings and recent news releases without providing investment recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments