Amkor Technology's Growth Anchored by Advanced Packaging Innovation and Geographic Expansion

Amkor leverages technology leadership, global footprint expansion, and strategic partnerships to drive resilience and growth in a cyclical semiconductor market.

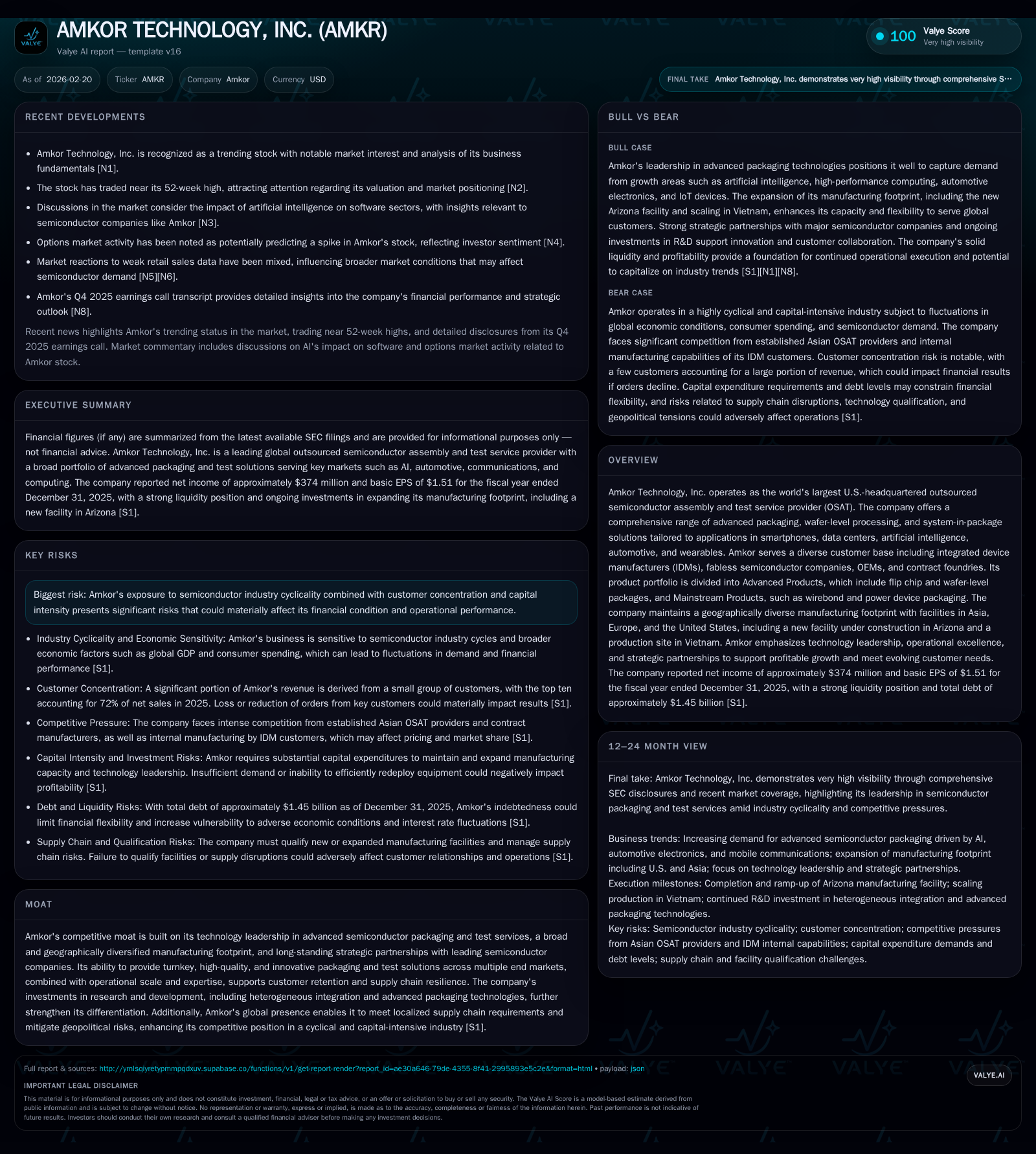

Amkor Technology, Inc. (AMKR) stands as the largest U.S.-headquartered OSAT provider, offering a broad portfolio of advanced semiconductor packaging and test services tailored for key growth markets such as AI, automotive, and data centers. The company's recent growth has been supported by investments in manufacturing capacity including its new Arizona facility and Vietnam site, along with advances in heterogeneous integration and wafer-level packaging technologies. Despite industry cyclicality and customer concentration challenges, Amkor maintains solid profitability with disciplined capital allocation focused on capital expenditures and R&D to sustain innovation and scale. Key metrics reflect steady revenue growth, stable operating margins, positive free cash flow generation, and modest dividend payouts.

Company Overview

Amkor Technology, Inc., recognized as the world’s largest U.S.-headquartered outsourced semiconductor assembly and test (OSAT) service provider, plays a pivotal role in the global semiconductor supply chain [S1][S24]. The company delivers a broad portfolio covering advanced packaging—including flip chip, wafer-level processing—and system-in-package (SiP) solutions geared toward high-growth applications such as smartphones, data centers leveraging artificial intelligence (AI), automotive electronics including ADAS systems, industrial IoT devices, wearables, and consumer electronics.

Amkor’s clientele includes integrated device manufacturers (IDMs), fabless semiconductor firms, original equipment manufacturers (OEMs), and contract foundries. This spectrum underpins diversified revenue streams while posing dependency risks due to customer concentration [S4][S5].

Historical Performance

Over recent years through fiscal 2025, Amkor has demonstrated steady top-line growth accompanied by consistent profitability despite inherent cyclicality in semiconductor markets. Below is a summary of key financial metrics:

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|---|

| 2025 | 374 | 1096 | 467 | 905 | +5.6% |

| 2024 | 354 | 1089 | 438 | 744 | -1.6% |

| 2023 | 360 | 1270 | 470 | 749 | -53.0% |

| 2022 | 766 | 1099 | 897 | 908 |

Note: Omitted columns lack sufficient annual XBRL coverage in the provided tags (need ≥2 annual points): Rev, Buybacks. Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($mm) | FCF ($mm) | ROE% |

|---|---|---|---|

| 2025 | 82 | 191 | 8.4 |

| 2024 | 179 | 345 | 8.5 |

| 2023 | 75 | 521 | 9.1 |

| 2022 | 55 | 190 | 20.9 |

Source: SEC companyfacts cache [F1].

Note: Revenue absolute figures for FY2023-24 not detailed in tags; YoY computed where possible [F1].

Notably, the operating income noticeably contracted from the exceptionally strong fiscal year of 2022—likely reflecting the peak pandemic recovery surge—but stabilized thereafter with resilient margin expansion into FY25 [F1]. The moderation in net income mirrors this dynamic while return on equity remains solid at approximately 8.4%, commensurate with capital-intensive operations [F1].

Operating cash flows have been consistently robust over this period exceeding $1 billion annually. Free cash flow remains positive but constrained owing to elevated capital expenditure aligned with strategic capacity expansion [F1]. Dividend payments have trended upward modestly though remain conservative relative to operating cash flow.

Drivers of Past Growth

Historical revenue gains have largely stemmed from:

- Increased adoption of advanced packaging technology driven by AI workloads fueling HPC demand [S9][N2].

- Diversification across end markets reducing reliance on cyclical smartphone segments; automotive content growth supports mid-teens segment share [S18][S28].

- Geographic expansion including ramp-up of recently commissioned Vietnam facility (operational since Q3/2024), which supplements lower-cost production capacity [S9][S21].

- Strategic long-term partnerships with marquee customers such as Apple (approx.29.8% sales exposure) and Qualcomm (~11%) underpinning volume stability [S4][S5].

- Sustained R&D investments targeting heterogeneous integration solutions facilitating multi-chip modules for AI accelerators and networking chips enhancing product differentiation [S6][S10].

Future Growth Prospects

Growth Catalysts

- Advanced Packaging Innovation: Continued commercialization of heterogeneous integration technologies like high-density fan-out (HDFO), panel-level fan-out (PLFO), copper hybrid bonding for ultra-fine pitch interconnects are expected to command premium product positioning addressing HPC/AI workloads [S6][S10].

- Data Center & AI Expansion: Increasing chiplet complexity necessitates turnkey SiP modules supplied by OSATs; co-packaged optics developments bolster participation in cloud-scale infrastructure growth momentum [N1][S10].

- Automotive Market Penetration: Growing semiconductors content in EVs/ADAS—with specialized power packaging for SiC devices—supports revenue diversification beyond mobile communications [S6][S18][S28].

- Geographic Footprint Expansion: Completion of the Arizona manufacturing facility under CHIPS Act funding is expected to accelerate near-shoring demands and address geopolitical risk concerns of U.S.-based OEMs or government-mandated sourcing requirements [S9][S14]

- Customer & Supply Chain Partnerships: Deepening collaboration on co-development efforts improves time-to-market acceleration for leading fabless/IDM customers incentivizing long-term order visibility even if formal backlog is minimal [S9][N2].

Constraints / Risks

- Semiconductor industry cyclicality is an enduring pressure that can produce volatile demand swings reflecting macroeconomic shifts or inventory corrections [S7][S12][S13].

- Customer concentration risk remains material: loss or volume reduction from top clients could significantly impair performance due to close to three quarters aggregate revenue reliance on top ten customers [S4][N3].

- Intense competition from Asian OSAT peers such as ASE Technology or JCET Group alongside internal IDM packaging capabilities limit pricing power amidst downward pricing pressures for mature packaging types [S11][S15][S22].

- Capital intensity demands high utilization rates to achieve attractive gross margins; underutilization risks exist especially if capacity additions outpace demand due to misaligned forecasts or execution delays [S12][S23].

- Geopolitical trade restrictions including export controls affecting China pose operational risks given significant overseas footprint spanning multiple countries including China itself [S7][S16][S20].

- Requirement for continuous innovation coupled with compliance costs related to environmental regulations could raise operating expenses over time particularly as renewable energy usage expands across factories [S14][S27]

Recent Developments & Guidance Insights

During Q4 FY2025 earnings call reports dated February ’26 ([N2], [N3], [N4]), Amkor highlighted continuing strength in AI-GPU platform demand driving volume gains especially within their advanced packaging segments. The company noted factory utilization improvements at their Vietnam site alongside progress on construction milestones for Arizona facility aligned with their obligations under CHIPS Act funding awards totaling up to $407 million [N2], [S14], marking critical investments enabling U.S-based production scalability.

While no explicit full-year financial guidance was provided post-Q4 results ([N2]), observers should monitor capacity ramp-up timelines at new plant sites, ability to win design-ins within evolving AI/automotive ecosystems as indicators ahead.

Capital Allocation & Returns Profile

Amkor’s financial strategy reflects dual priorities:

- Ongoing substantial capital expenditures ($905 million in FY25 up from $744 million prior year), focused on scaling advanced packaging capacity with payback seen incrementally over cycle durations rather than immediate margin accretion given build-out stage operational gearing effect [F1] [S22].

- Disciplined dividend policy paying ~$82 million in dividends during FY25 with no concurrent buybacks reported recently ([F1], no repurchases post FY2014), favoring reinvestment into technology modernization rather than direct shareholder returns.

Operating cash flows consistently translate well into free cash flow (~$191 million in FY25 after capex) signaling healthy internal funding capability while maintaining liquidity cushion reflected by current ratio ~2.27x ([F1])—important given the sizeable outstanding debt load exceeding $1.44 billion contemplated alongside restrictive covenants limiting further indebtedness increments without compliance reviews ([S25]). Although ROE at ~8.4% is moderate reflecting heavy asset base investment typical of OSAT players, Amkor balances growth investment against cautious leverage management effectively.

Industry Context Analysis

The OSAT segment is highly fragmented yet capital intensive. Advanced semiconductor nodes trending toward chiplet architectures compel OSAT providers like Amkor to innovate rapidly around heterogeneous integration methods including stacking techniques that minimize latency/bandwidth bottlenecks while miniaturizing form factors—deftly addressed via panel-level fan-out package advancements grounded at Amkor’s Korea-based Center of Excellence ([S6], industry analysis). Furthermore, amid rising localization tendencies triggered by geopolitical frictions between US-China relations impacting semiconductor supply chains globally (), Amkor’s investments into domestic U.S manufacturing spur a strategic advantage aligning closely with governmental subsidization initiatives occasioned under the CHIPS Act. However, competitive pressures remain intense: well-capitalized Asian rivals benefit from lower cost structures coupled with governmental support making price competitiveness an ongoing challenge alongside margin erosion pressures inherent within mature segments (). Thus operational efficiency gains from scale economies blended with higher value-add via bespoke co-development serve as critical success factors ensuring sustainable differentiation.

Conclusion

Amkor Technology exhibits strength derived from comprehensive product offerings centered on sophisticated packaging processes essential for next-generation semiconductors powering AI-centric data centers and electric/autonomous vehicles worldwide. Its strategic moves expanding geographic manufacturing capabilities enhance supply chain agility amidst mounting geopolitical uncertainties. Though the business faces cyclical headwinds typical of semiconductor industries compounded by customer concentration risk and capital intensity challenges—with consequent margin variability—the company’s focus on continued innovation combined with a geographically diverse footprint enhances competitive defensibility. Prospective investors should watch developments around new factory commissioning progress including achieving targeted operational efficiencies at Arizona facility together with evolving customer design wins in emerging technological spaces such as co-packaged optics that can materially influence midterm growth trajectory.

Disclaimer: This analysis summarizes publicly available information about AMKOR TECHNOLOGY INC., relying primarily on SEC filings and industry reports without forming any investment recommendation.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments