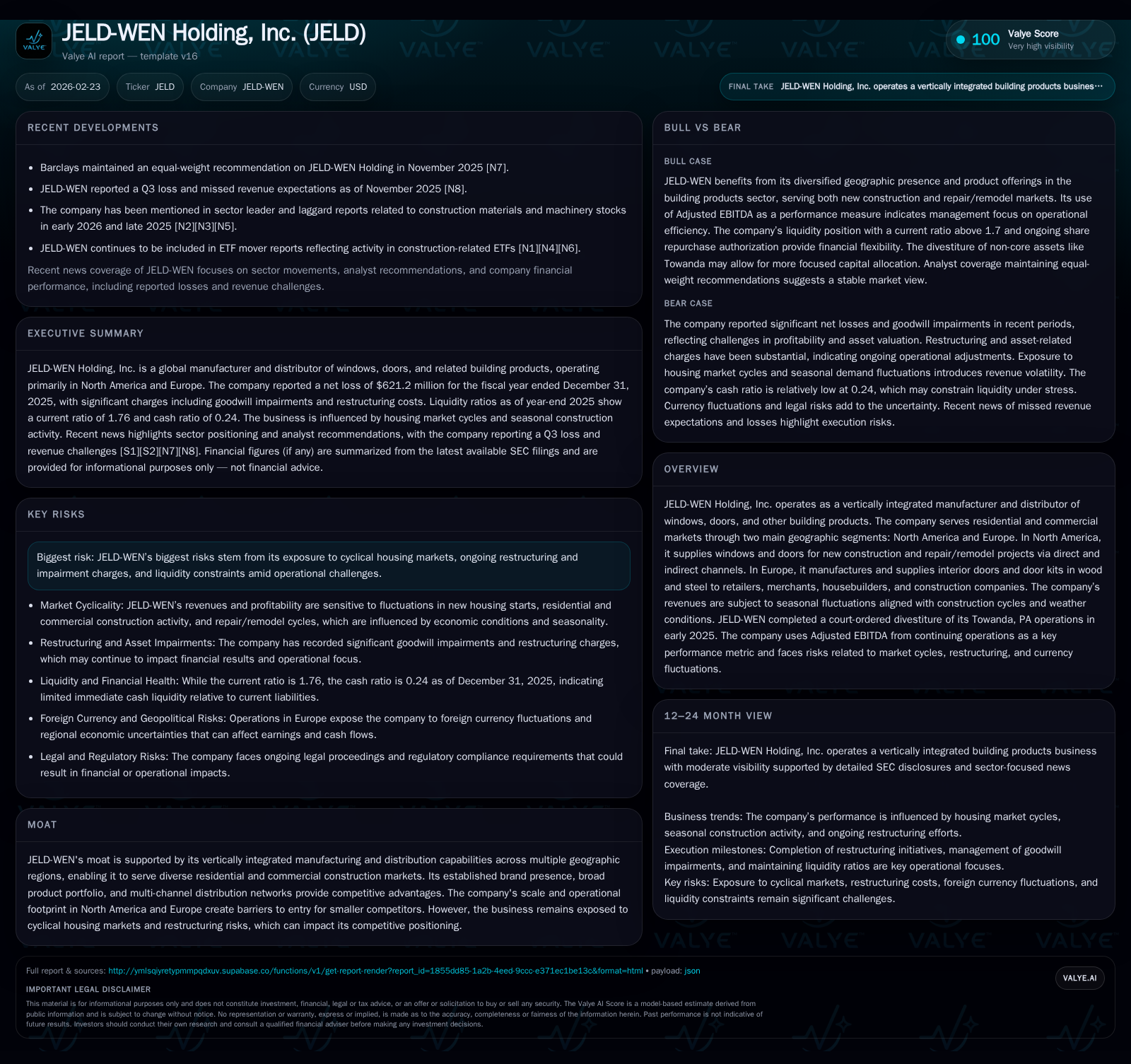

JELD-WEN Confronts Structural Losses and Legal Divestitures Amid Housing Market Cyclicality

JELD-WEN's financial deterioration reflects ongoing headwinds from housing market cycles and legacy litigation outcomes impacting its North American and European operations.

JELD-WEN Holding, Inc., a vertically integrated window and door manufacturer, has experienced significant financial setbacks with escalating operating losses and net losses through 2025, driven by cyclical housing demand and the aftermath of a court-ordered divestiture. The company’s business is divided into North American new construction and repair/remodel markets, and European interior doors channels. Despite attempts at restructuring, impairment charges and legal settlements continue to weigh on results. Liquidity remains stable with a current ratio of 1.76, supported by manageable debt maturities and refinancing activities. Capital expenditures have been reduced amid shrinking operating cash flows, while shareholder returns remain suspended with no dividends or buybacks in 2025. Future growth hinges on housing market recovery, cost control, and resolution of lingering litigation risks.

Company Overview

JELD-WEN Holding, Inc. operates as a vertically integrated manufacturer and distributor mainly focused on windows, doors, and related building products. Its footprint spans two primary geographic segments: North America and Europe. In North America, JELD-WEN sells windows and doors targeting both new residential/commercial construction as well as repair/remodel markets via broad indirect dealer networks along with direct channel sales. Europe's segment centers on manufacturing interior doors and door kits composed of wood or steel; these are supplied largely to retailers, merchants, housebuilders, and commercial construction companies [S4][S8].

The business is inherently subject to seasonal and economic cyclical factors aligning with construction activity levels and weather patterns. The company uses Adjusted EBITDA from continuing operations as a vital measure of core operational performance but faces significant challenges from restructuring costs, impairment charges, litigations including government antitrust actions, regulatory risks, and liquidity pressures [S2][S6][S22].

Historical Performance

Historical financial data reveals a stark reversal for JELD-WEN through 2025:

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|---|

| 2025 | -621 | -5 | -416 | 120 | -228.6% |

| 2024 | -189 | 106 | -126 | 162 | -443.9% |

| 2023 | -35 | 345 | 142 | 98 | -176.0% |

| 2022 | 46 | 30 | 106 | 83 |

Note: Omitted columns lack sufficient annual XBRL coverage in the provided tags (need ≥2 annual points): Rev, Div. Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Buybacks ($mm) | FCF ($mm) | ROE% |

|---|---|---|---|

| 2025 | 0 | -125 | -673.6 |

| 2024 | 24 | -56 | -30.5 |

| 2023 | 0 | 247 | -4.1 |

| 2022 | 132 | -53 | 6.3 |

Source: SEC companyfacts cache [F1].

Table notes: Revenue data was not available within provided tags; dividends have been zero since before FY2018; buyback activity ceased after FY2024 except zero in FY2025; YoY calculations based on available data excluding missing values [F1].

Operating income nosedived by over double from FY2024 driven largely by significant goodwill impairments related partly to the court-ordered divestiture of the Towanda plant completed early in calendar year (CY)2025 which carried associated asset write-downs approximating $31 million recognized late 2024 [S26]. Net loss similarly deepened due to non-cash charges coupled with continued poor earnings before special items.

Operating cash flow collapsed sharply into negative territory year-over-year consistent with operational challenges constricting free cash flow generation despite capex cutbacks approximately one-quarter lower than the prior year.

On shareholders' equity basis the return on equity plummeted to approximately negative 674%, illustrating erosion of value amid accumulating losses and impairments during FY2025 [F1].

Segment Performance & Operational Details

JELD-WEN organizes its business into two reportable segments reflecting discrete geographies:

- North America: specializing in windows and doors primarily serving residential new builds plus commercial markets plus repair & remodel demands through diverse direct/indirect sales channels such as dealers / distributors / builders / architects.

- Europe: producing interior wooden and steel doorsets/delivery kits supplied typically to large retailers, merchants specializing in building supplies as well as housebuilding firms focused heavily on interior door solutions.

Adjusted EBITDA from continuing operations for these segments came under pressure during recent quarters impacted notably by restructuring charges related to optimization efforts post-divestiture as well as impairment impacts mainly affecting goodwill allocations within each segment [S8].

Capital investment for sustaining production capabilities shows concentration notably toward North America with roughly two-thirds of annual capex spent there versus one-third in Europe which fits the company’s producing window/door focus requiring more complex plant infrastructure. Depreciation expense further confirms heavier fixed asset weight in North America.

Capital Structure & Liquidity

As of late FY2025 (September quarter), JELD-WEN carried total indebtedness exceeding $1.18 billion including senior notes due between December 2027 through September 2032 bearing coupon rates ranging from approximately mid-4%s up to a high single-digit fixed coupon at 7%, complemented by a term loan facility extended through July 2028 priced at LIBOR/SOFR plus margin (~6.43% average coupon). This profile implies ongoing debt service costs that weigh on profitability especially against shrinking earnings before interest [S21][S27].

The company maintains credit facilities including an asset-based revolving loan limited by borrowing base calculations tied to accounts receivable/inventory levels that provide working capital flexibility. Liquidity ratios measure reasonably at current ratio ~1.76 derived from $1 billion+ current assets versus ~$578 million current liabilities indicating adequate short-term coverage albeit no margin for stress given income losses and negative operating cash flow [F1].

JELD-WEN has strategically deployed proceeds from senior note issuances (e.g., $350M notes issued mid-2024) partly toward redeeming higher cost legacy debt tranches improving overall weighted average cost of debt but accrued refinancing costs impact short-term earnings [S27]. There were no share repurchases authorized or executed during FY2025 reflecting prudent liquidity conservation amidst operational disruptions [F1]. No dividend payments have been made since prior years consistent with capital preservation strategies faced by many industrials during cyclical slowdowns.

Legal & Regulatory Issues Impacting Performance

Significant legacy litigation surrounds JELD-WEN’s former CMI acquisition leading to antitrust claims notably involving Steves & Sons where courts imposed multi-million dollar damage awards coupled with mandated divestiture of certain operations including the Towanda PA manufacturing site which closed officially early CY2025 after protracted proceedings. The divestiture was executed despite JELD-WEN's motions contesting it based on changed industry conditions but ultimately upheld by district courts with appeals pending albeit unlikely reversing prior outcomes soon [S9][S18][S24].

Additionally, investigations including U.S. Department of Commerce anti-dumping/countervailing duty inquiries into wood millwork imports from China present risks of incremental tariff liabilities potentially inflating product input costs if unfavorable rulings persist beyond preliminary findings scheduled for late CY2025/early CY2026 issuance [S17][N2].

Existing litigation-related settlement charges continue being recorded including provisions that absorb cash resources while also generating headline goodwill write-downs further exacerbating headline income deficits despite management's claims of meritless allegations underlying some suits [S25][S16][S22].

Future Growth Prospects & Risks

Growth possibilities lean heavily on cyclical housing demand recovery particularly new residential construction along with increased repair/remodel spending which account for most volume downstream usage of windows/doors provided by the Company’s product portfolio. Stronger home improvement trends could benefit sales volumes but may be offset partially if raw material inflation or tariff pressures endure.

Restructuring initiatives that aim to streamline manufacturing footprints post-Towanda divestiture are ongoing but carry inherent execution risk alongside potential additional impairment charges if forecasted efficiencies do not fully materialize.

Geopolitical tensions plus supply chain constraints combined with legal uncertainties surrounding past acquisitions add layers of operational risk that might delay return-to-profitability timelines significantly beyond near term horizons.

No explicit guidance or medium-term targets have been issued publicly yet; observers should monitor quarterly Adjusted EBITDA trends excluding special items closely alongside any notices regarding debt covenant compliance or refinancing efforts given periods of fragile cash flows noted recently [N1][N2][S2][F1] (analysis).

Capital Allocation & Returns Analysis

JELD-WEN dispensed no dividends over recent years corresponding with sustained losses compounded by large non-cash goodwill impairments peaking during FY2025. Similarly buyback programs halted entirely after modest repurchases limited to prior fiscal periods suggest management focus shifted fully toward balance sheet repair rather than returns enhancement.

Free cash flow generation turned negative when subtracting capex from operating cash flow for FY2025 at roughly -$125 million undermining internal funding capacity for growth investments or shareholder distributions absent external financing support [F1].

With shareholders’ equity compressed below $100 million in latest filings showing stress on book value cushions (down from $620 million prior year), return on equity calculations yield deeply negative metrics highlighting distressed capital efficiency conditions unfavorable for value creation under current scenarios [F1].

Debt holders continue receiving contractual interest payments while equity stakeholders bear residual volatility inherent given earnings volatility influenced strongly by restructuring-related expenses and legacy litigations settlement impacts.

Industry Context (Analysis)

The building materials manufacturing sector is typically capital intensive with exposure linked closely to housing starts cycles which depend upon macroeconomic factors like mortgage interest rates, labor availability, material input costs such as lumber/panels/steel composites, and regulatory frameworks impacting energy efficiency standards for windows/doors driving product innovation requirements.

Vertical integration provides JELD-WEN scale advantages allowing it some insulation versus smaller competitors who may face more acute supply chain disruptions or pricing pressures but also increases fixed cost bases requiring steady volume throughput levels sustainable only during normalized or expansionary housing periods.

Meanwhile trade disputes involving anti-dumping tariffs specifically affect manufacturers sourcing components internationally altering competitive dynamics within North American markets feeding their plants.

Conclusion

JELD-WEN faces a considerable challenge reversing the steep downward earnings trajectory reflected by mounting goodwill impairments linked closely to mandated asset divestitures combined with ongoing legal contingencies enveloping historical acquisition disputes. The company maintains liquidity headroom but deteriorated operating cash flows alongside shrinking equity book values signal constrained financial flexibility under current market conditions.

Performance over coming quarters will hinge crucially upon stabilizing core operational margins through cost rationalization efforts while navigating prolonged industry cyclical downturn exacerbated recently by geopolitical tariff uncertainties impinging input costs. Absent an improving housing market backdrop or successful resolution minimizing litigation burdens faster than expected—prospects remain subdued near term albeit opportunities exist if markets rebound prompting increased replacement demand from aging installed bases across North America/Europe.

Investors should follow closely external indicators such as U.S./European new residential permits data along with updates on pending appellate court rulings relating to divestiture orders offering clearer visibility into how strategic repositioning unfolds financially through revised segmental contributions going forward.

This analysis is based solely on information available up to February 23, 2026, including company SEC filings and reliable news sources. It does not constitute investment advice or recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments