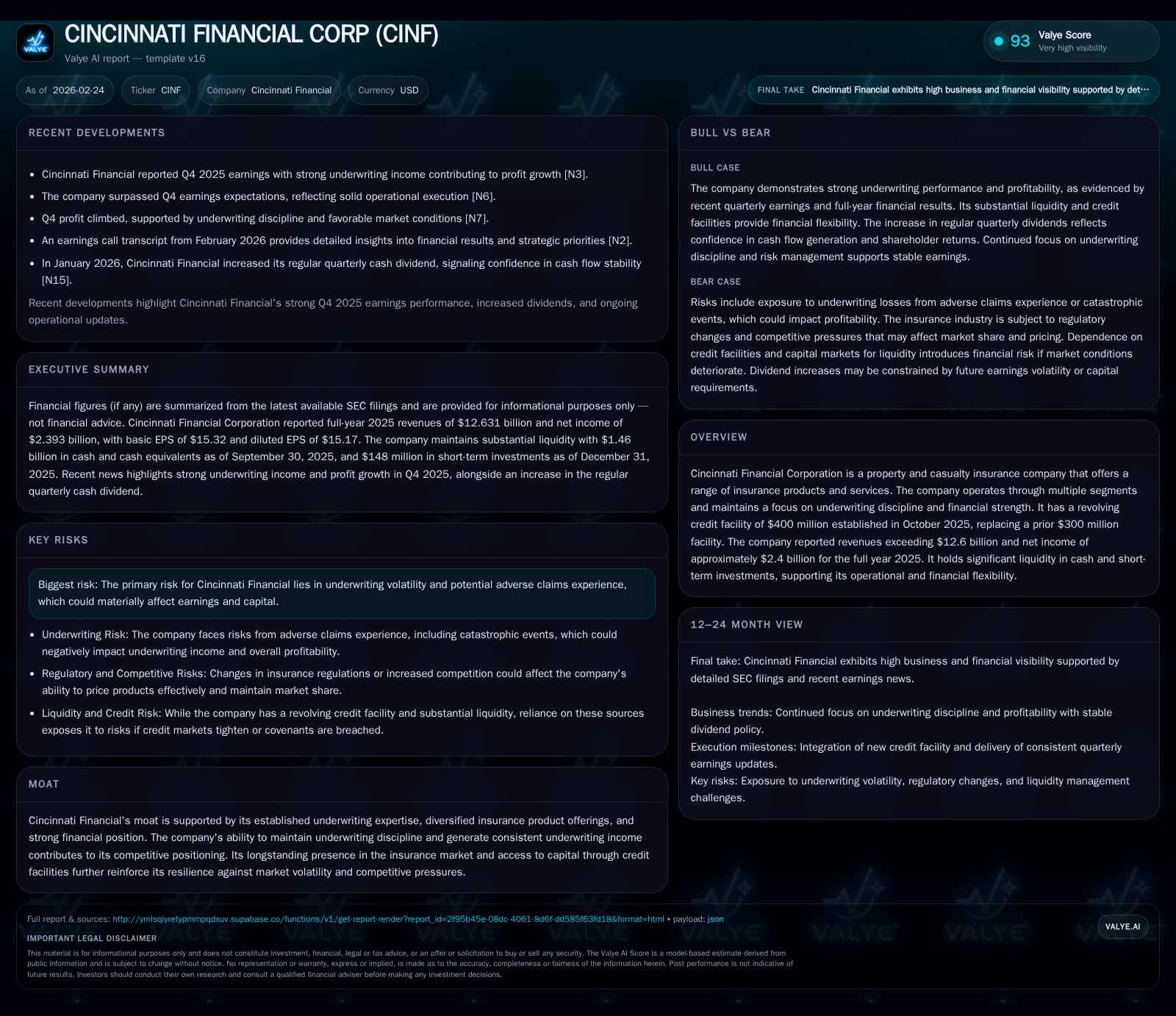

Cincinnati Financial Reveals Sustained Growth and Strategic Capital Management in 2025

The company demonstrated significant revenue growth combined with disciplined underwriting and enhanced liquidity via a new credit facility.

Cincinnati Financial Corporation recorded robust revenue expansion in 2025, driven by diversified underwriting income and effective risk controls. The strategic replacement of its revolving credit facility elevated its financial flexibility, supporting ongoing operations and shareholder returns. Despite inherent underwriting volatility risks, the firm’s strong cash flow and capital allocation underscore its resilient positioning within property-casualty insurance.

Historical Revenue Growth and Financial Performance

Cincinnati Financial demonstrated robust top-line growth with revenues increasing by 11.4% from $11.34 billion in 2024 to $12.63 billion in 2025 [F1]. Net income improved modestly by 4.4% to $2.39 billion in FY2025, continuing the recovery from a net loss of $486 million reported in FY2022 [F1]. Operating cash flows strengthened significantly by 17.5% year-over-year to $3.11 billion, while capital expenditures remained low at $20 million, underpinning strong free cash flow generation [F1].

Historical performance (annual)

| FY | Rev ($bn) | Net ($bn) | CFO ($bn) | Capex ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 12.6 | 2.4 | 3.1 | 20 | +11.4% | +4.4% |

| 2024 | 11.3 | 2.3 | 2.6 | 22 | +13.2% | +24.4% |

| 2023 | 10.0 | 1.8 | 2.1 | 18 | +52.7% | +479.2% |

| 2022 | 6.6 | -0.5 | 2.1 | 15 |

Note: Omitted columns lack sufficient annual XBRL coverage in the provided tags (need ≥2 annual points): OpInc. Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($mm) | Buybacks ($mm) | FCF ($bn) |

|---|---|---|---|

| 2025 | 525 | 205 | 3.1 |

| 2024 | 490 | 126 | 2.6 |

| 2023 | 454 | 67 | 2.0 |

| 2022 | 423 | 410 | 2.0 |

Source: SEC companyfacts cache [F1].

Note: Operating income data is not available from the provided tags; ROE is approximated as net income divided by stockholders' equity [F1].

Underwriting Discipline Amid Volatility

Underwriting discipline remains a foundational element for Cincinnati Financial’s profitability and risk management strategy [N3][S1]. The company actively manages combined ratios through disciplined pricing models and prudent reinsurance arrangements to mitigate claims volatility [S4][S6]. Maintaining adequate loss reserves is emphasized due to the inherent unpredictability of property-casualty claims trends [S6]. This focus supports stable underwriting margins even amid cyclical fluctuations.

Strategic Capital Structure Update

In October 2025, Cincinnati Financial replaced its previous $300 million credit facility with a new unsecured revolving credit facility totaling $400 million, extending maturity to October 2030 with two one-year extension options [S5][S8][S10]. This facility enhances liquidity and provides for letters of credit up to $400 million and swing line loans up to $75 million, offering diversified funding sources [S5]. Covenants include a maximum debt-to-capital ratio of 35%, preserving financial flexibility while limiting leverage risk [S8]. The credit syndicate consists of four lenders with the largest commitment capped at $125 million [S10].

Capital Allocation: Dividends and Share Repurchases

Capital returns remain balanced between dividends and share repurchases reflecting management's commitment to rewarding shareholders while supporting operational needs [S19][S20][N11]. Dividend payments increased steadily to $525 million in FY2025 from $490 million in FY2024, corresponding with sustainable earnings growth and supporting a dividend yield near approximately 2.3% [F1][N12]. Share repurchases also grew substantially to $205 million in FY2025 compared to prior years, signaling confidence in the company's intrinsic value [F1].

Liquidity and Cash Flow Strength

Operating cash flow of $3.11 billion in FY2025 underscores the company’s ability to convert earnings into liquid funds efficiently [F1]. Modest capital expenditures around $20 million primarily support technology infrastructure rather than physical assets, contributing to free cash flow estimated at approximately $3.09 billion after capex [F1]. This liquidity profile supports both operational resilience and strategic flexibility.

Risk Considerations

The company faces risks typical of the property-casualty sector including potential adverse claims experience driven by frequency or severity fluctuations, catastrophic events, and reserve inadequacy which could pressure earnings and capital adequacy [S4][S6]. Regulatory changes may also impact underwriting practices or product offerings, requiring ongoing monitoring and proactive management engagement [S7]. Litigation exposure adds further uncertainty necessitating conservative reserving.

Growth Outlook and Market Positioning

Cincinnati Financial aims to capitalize on its diversified product portfolio spanning personal auto, commercial lines, and specialty insurance products concentrated primarily across Midwestern states but gradually expanding geographically [N2][S9]. Continued emphasis on risk-based pricing agility seeks to preserve margins amid competitive pressures [N1][N13]. The company also focuses on delivering tailored solutions for small- and medium-sized enterprises supported by efficient claims management technologies.

Milestones and Forward-Looking Indicators

Upcoming earnings calls will be critical for tracking sequential combined ratio trends as indicators of underwriting performance relative to premium growth [N9]. Monitoring utilization levels of the expanded revolving credit facility will provide insight into near-term liquidity needs or investment initiatives [N3]. Dividend policy updates or changes in share repurchase programs will signal management’s confidence level regarding future earnings stability [N11][S19][S20]. Additionally, commentary on reserve adequacy adjustments or regulatory developments will be important for assessing evolving risk appetite.

Disclaimer: This analysis is based solely on publicly available disclosures as of early 2026 for Cincinnati Financial Corporation and does not constitute investment advice or recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments