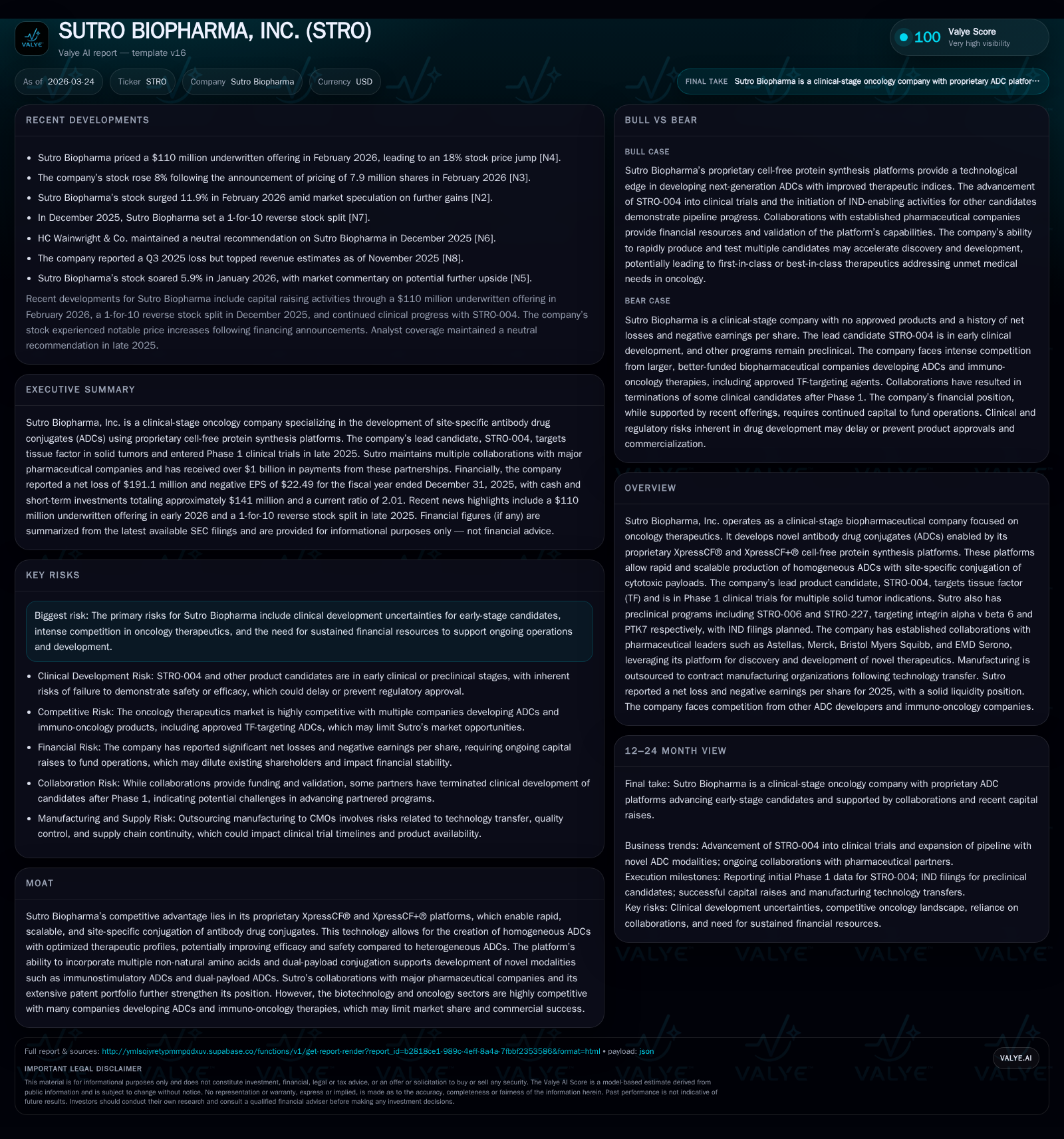

Sutro Biopharma Advances Novel ADCs Amid Clinical and Financial Challenges

Sutro Biopharma leverages proprietary cell-free protein synthesis platforms to develop next-generation oncology ADCs with promising clinical progress and ongoing operational losses.

Sutro Biopharma, a clinical-stage oncology-focused company, drives innovation through its proprietary XpressCF® platforms to produce homogeneous antibody drug conjugates (ADCs). After deprioritizing its former lead STRO-002, the company is advancing STRO-004 in Phase 1 trials targeting multiple solid tumors with data expected mid-2026. While its preclinical pipeline with STRO-006 and STRO-227 shows potential, Sutro faces typical biotechnology risks including high operating losses, negative equity as of FY2025, competition from larger firms, regulatory hurdles, and reliance on partnerships. Capital raises in early 2026 suggest liquidity support for ongoing development amid sustained cash burn.

Company Overview and Historical Performance

Sutro Biopharma is a clinical-stage biopharmaceutical company focused on oncology therapeutics centered on antibody drug conjugates (ADCs). It utilizes proprietary cell-free protein synthesis platforms—XpressCF® and XpressCF+®—to develop site-specific homogeneous ADCs that aim to improve therapeutic profiles relative to traditional heterogeneous ADCs.

Historically, Sutro recorded revenue of approximately $11.3 million in FY2019 but has incurred significant losses due to extensive R&D investment. Net income declined from -$119 million in FY2022 to -$191 million by FY2025 [F1], reflecting continued investment into clinical development and infrastructure. Operating cash flows remain negative as the company invests heavily into its pipeline.

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Net YoY |

|---|---|---|---|---|

| 2025 | -191 | -177 | -158 | +16.0% |

| 2024 | -227 | -192 | -238 | -113.0% |

| 2023 | -107 | -112 | -89 | +10.4% |

| 2022 | -119 | 4 | -129 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Buybacks ($) | ROE% |

|---|---|---|

| 2025 | 144.3 | |

| 2024 | -510.0 | |

| 2023 | 7000 | -71.4 |

| 2022 | 7000 | -54.9 |

Source: SEC companyfacts cache [F1].

Note: Revenue figures post-FY2019 are not material or reported; other financials relate to continuing operations.

By FY2025, accumulated losses resulted in negative equity, indicating ongoing financial challenges despite capital injections.

Platform Technology & Competitive Positioning

Sutro's XpressCF® platform allows for rapid synthesis of proteins incorporating non-natural amino acids enabling precise site-specific payload conjugation to antibodies. This approach contrasts with conventional cell-based methods that produce heterogeneous mixtures.

The enhanced XpressCF+® platform supports complex dual-payload conjugations combining cytotoxic agents with immunostimulatory molecules or synergistic warheads, potentially improving efficacy and safety through controlled pharmacokinetics.

These technological capabilities create competitive differentiation though the company faces formidable competition from established biopharmaceutical firms developing monoclonal antibodies, conventional ADCs (e.g., TIVDAK®), immune checkpoint inhibitors, CAR-T therapies, bispecifics, and other novel modalities [S15][S21].

Pipeline Progress and Growth Outlook

The lead wholly owned candidate STRO-004 targets tissue factor (TF) and is undergoing Phase 1 dose-escalation trials across multiple solid tumors including non-small cell lung cancer, cervical cancer, head & neck cancer, bladder cancer, and colorectal cancer. IND clearance was obtained in October 2025; dosing completed for the second dose cohort by February 2026 with third cohort dosing underway. Initial clinical data are expected mid-2026 [S1].

Preclinical programs offer additional growth prospects:

- STRO-006, targeting integrin αvβ6, is advancing IND-enabling studies aiming for filing within calendar year 2026.

- STRO-227 is a dual-payload ADC directed at PTK7 combining tubulin-disrupting and topoisomerase-inhibiting agents with anticipated IND filing late 2026 or early 2027.

These next-generation modalities leverage platform advantages potentially providing differentiated efficacy and safety profiles versus competitors' pipelines [S1][S29].

Collaborations and Licensing Agreements

Strategic partnerships provide funding support and validation:

- Collaborators include Astellas Pharmaceuticals, Merck, Bristol Myers Squibb, EMD Serono among others utilizing Sutro’s platform primarily for novel therapeutic discovery.

- The Tasly License Agreement grants exclusive rights for STRO-002 commercialization in Greater China; however global development was deprioritized following a strategic review in March 2025 [S19][S25].

These collaborations have historically provided substantial non-dilutive capital but also shape commercial rights geography-wise.

Financial Health and Capital Allocation

Financial results reflect sustained operating losses driven by heavy R&D spending without product revenues following deprioritization of STRO-002. Operating loss narrowed from $238 million in FY2024 to $158 million in FY2025 reflecting some operating leverage gains but cash consumption remains significant.

Operating cash flow was deeply negative at -$177 million for FY2025 underscoring continued investment into pipeline development [F1]. Negative equity at fiscal year-end signals cumulative losses outpacing prior investments.

Capital market activities included:

- A $110 million underwritten stock offering priced February 10, 2026 bolstered liquidity; stock price increased post-announcement indicating positive investor sentiment around developmental progress [N3][N4].

- Termination of the ATM Equity Sales Agreement with Jefferies LLC as of March 23, 2026 suggests a shift toward alternative financing approaches beyond smaller incremental sales programs [S3].

No dividends or material share repurchases have been reported; capital allocation prioritizes research advancement over shareholder returns given persistent negative free cash flow.

Regulatory Environment and Risks

The biopharmaceutical industry is highly regulated:

- FDA approval requires extensive preclinical testing followed by phased clinical trials spanning multiple years before marketing authorization.

- Early-stage assets like STRO-004 face inherent clinical trial risks; preclinical candidates carry execution uncertainties.

- Pricing pressures from healthcare reforms such as the Inflation Reduction Act mandating Medicare drug price negotiations alongside state-level regulations could constrain future margins even post-approval [S4][S10][S20].

Compliance costs arise from federal anti-kickback statutes, false claims laws, state data privacy requirements impacting patient data management, plus companion diagnostic device regulations which may apply if guided therapies become necessary [S5][S9][S27].

Intellectual property risks include defending proprietary technology against competing claims affecting freedom-to-operate or exclusivity duration [S12][S18][S24].

Competitive Environment Analysis

The ADC space is intensely competitive involving large pharmaceutical companies pursuing established targets like TF using conventional linkers/payloads alongside emerging biotechs innovating bispecific ADCs or cell therapies. Additionally, Chinese biotech firms backed by state enterprises add complexity to licensing and commercial landscapes globally [S15][S16].

Specifically:

- The approved TF-targeting ADC TIVDAK® provides a clinical benchmark but leaves room for differentiated molecules offering improved tolerability or efficacy enabled by Sutro’s homogeneous conjugation technology.

- Multiple ITGB6-targeting or PTK7-targeting biologics/ADCs are under active development creating crowded indication spaces necessitating clear differentiation for market success.

Success depends on demonstrating superior therapeutic indices supported by robust patent protection covering chemistry and manufacturing innovations.

Outlook and Key Upcoming Milestones

Mid-2026 will be pivotal with initial human data readouts from the STRO-004 Phase I study informing dose selection and safety profiles critical for progression into later-stage trials.

Additionally:

- Progression toward IND filings for STRO-006 and STRO-227 will demonstrate pipeline execution capability beyond a single asset.

- Monitoring cash runway against current burn rates plus any new financing will be crucial given ongoing net losses exceeding hundreds of millions annually.

Pipeline advancement must navigate intensifying competition alongside regulatory cost pressures that could affect speed-to-market or pricing power upon launch.

Investors should watch clinical milestone announcements alongside updated capital strategy disclosures through the remainder of calendar year.

Conclusion

Sutro Biopharma represents a small-cap biotech innovator specializing in advanced ADC technologies leveraging proprietary cell-free protein synthesis platforms aimed at redefining safety and efficacy paradigms in oncology treatments. While its lead candidate recently entered clinical evaluation after years of R&D investment without product revenue beyond collaborations, upcoming data will be pivotal for strategic direction.

Persistent operating losses coupled with negative equity underscore typical financial challenges faced by early-stage biotechs; however recent capital raises illustrate market willingness to finance further development bets. Competition is intense across targeted tumor antigens compounded by evolving regulatory landscapes impacting approval pathways and reimbursement dynamics.

Overall Sutro's future hinges on translating proprietary science into clear clinical benefit supporting eventual commercialization amid common oncology biotech industry risks.

Disclaimer: This report reflects publicly available information as of March 24th, 2026. It does not constitute investment advice nor endorsement.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments