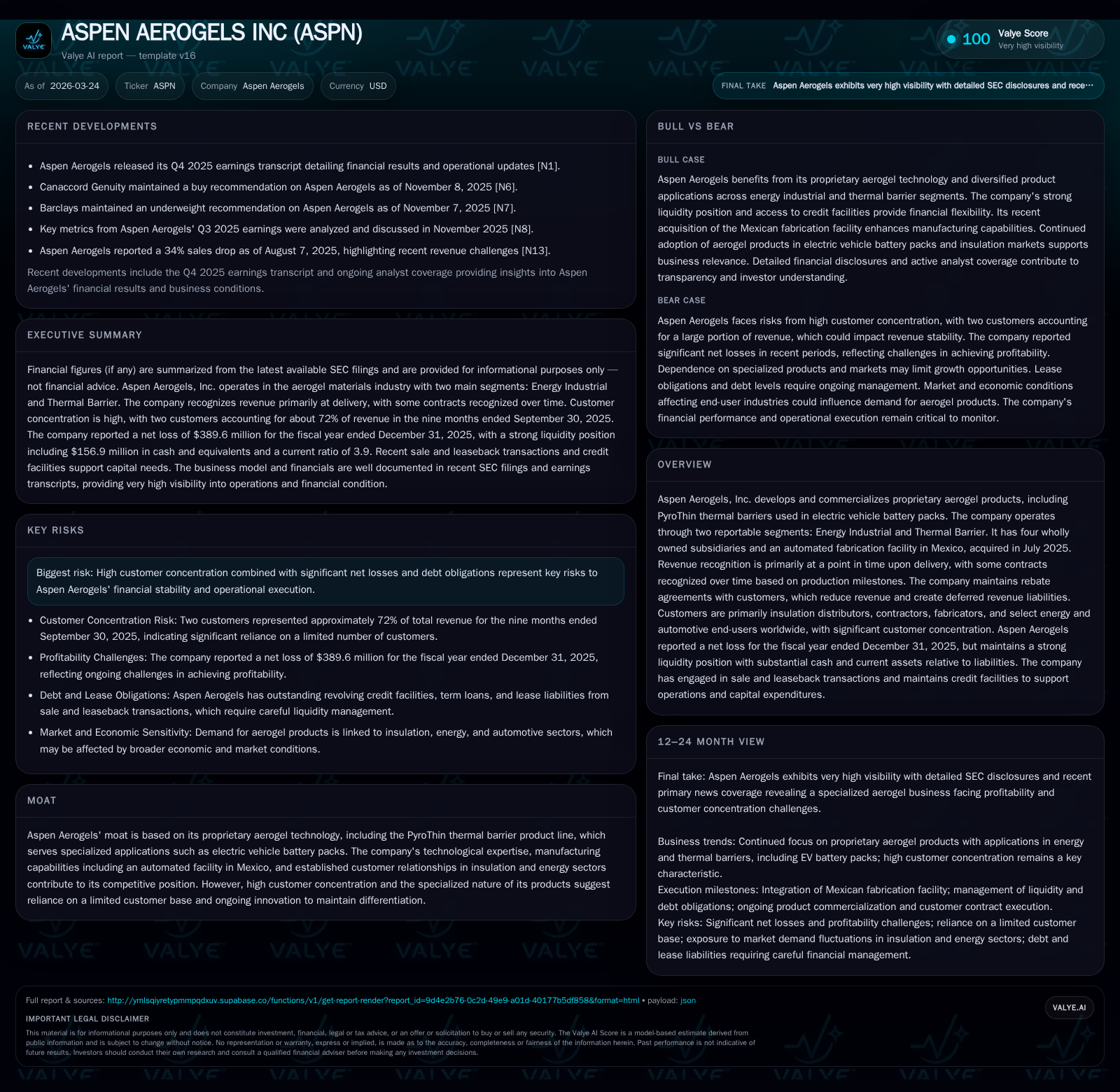

Aspen Aerogels’ Technical Edge and Financial Pressure in Electric Vehicle Materials

Aspen Aerogels advances aerogel technology for EV battery thermal barriers while navigating significant losses and capital investment demands.

Aspen Aerogels leverages its proprietary PyroThin aerogel technology, focusing on electric vehicle (EV) battery thermal management, to drive revenue growth. However, FY2025 saw a sharp transition to a large net loss due to increased costs from scaling production, R&D investments, and integration of a new automated facility in Mexico. The company faces commercial risks from customer concentration and milestone-based revenue recognition. Strong liquidity supports near-term operations, but elevated debt levels and capital expenditures require monitoring. Future performance depends on managing contract milestones, cost efficiency improvements, customer diversification, and capital structure developments.

Track Record of Growth: Revenue Momentum Versus Profit Volatility

Aspen Aerogels demonstrated notable revenue momentum culminating in fiscal year (FY) 2025 that contrasts sharply with its profitability trajectory. Historical annual revenues show a rebound from $27.6 million in 2016 to approximately $36.4 million by end-2017 [F1], marking early progress with proprietary aerogel products. In FY2025, the firm realized a growth rate of roughly +31.6% year-over-year relative to prior periods suggested by available data [F1], largely driven by increased adoption of its PyroThin thermal barriers targeted at electric vehicle (EV) battery applications.

However, this top-line growth unfolded alongside severe margin deterioration and profit volatility. Operating income flipped from positive $54.5 million recorded in FY2024 to a substantial operating loss nearing -$378.2 million by FY2025 [F1]. The net income mirrored this shift plunging to about -$389.6 million after being modestly positive at $13.4 million the previous year [F1]. Such swings reflect heightened costs tied to scaling manufacturing operations, investments into research and development (R&D), and expenses related to integrating new production capacity.

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|---|

| 2025 | -390 | 33 | -378 | 37 | -3012.5% |

| 2024 | 13 | 46 | 55 | 86 | +129.2% |

| 2023 | -46 | -43 | -49 | 175 | +44.6% |

| 2022 | -83 | -94 | -79 | 178 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2025 | -5 | -165.4 |

| 2024 | -41 | 2.2 |

| 2023 | -218 | -9.4 |

| 2022 | -272 | -18.5 |

Source: SEC companyfacts cache [F1].

Table: Historical Financial Performance Summary highlighting recent surge in losses amid top-line gains.

Underlying Drivers in a Specialized Product Landscape

Aspen's core product strength lies within highly specialized aerogel technologies distinguished by industry-specific applications such as the PyroThin thermal barrier system engineered primarily for EV battery packs [S1][N1]. These materials deliver superior insulation properties critical to thermal management challenges faced by EV manufacturers seeking lighter-weight and higher-performance solutions.

Revenue recognition is nuanced: while most sales are recorded at delivery points (point-in-time), certain contracts observe milestone-based accounting where revenue is recognized progressively through production phases aligned with contractual milestones [S1]. This methodology can create volatile short-term revenue reporting patterns compounded by deferred revenue liabilities arising from customer rebate agreements designed to incentivize volume or performance targets.

Such specialization contributes to Aspen’s defensible moat via proprietary manufacturing processes underpinning product differentiation but introduces complexity regarding timing and predictability of revenues.

Strategic Expansion Through Manufacturing Automation

A pivotal event during mid-2025 was Aspen Aerogels’ acquisition of an automated aerogel fabrication facility located in Mexico [S1], which represents an effort to enhance manufacturing scale and consistency while targeting cost efficiencies across its thermal barrier segment.

The Mexico facility enables automation capabilities aligned with aerogel fabrication that can improve throughput capacity while potentially reducing per-unit production costs over time—a critical factor for competing in cost-sensitive EV component markets where volume ramp-up is expected yet operational precision remains paramount.

While promising strategically, the integration imposed additional fixed costs and capital expenditure demands during calendar year 2025 contributing to amplified operating losses evident in reported results [S1][F1]. The sizable capex reduction by over half compared with prior years—from approximately $86 million down to $37 million—signals initial completion phases but continued investment orientation.

Customer Concentration and Its Impact on Commercial Stability

The company explicitly reports customer concentration risks given its reliance on a relatively narrow set of customers encompassing insulation distributors, contractors, fabricators alongside select energy sector participants and automotive end-users distributed globally [S1]. Two primary customers contribute disproportionate shares of accounts receivable balances reflecting ongoing commercial dependence.

This concentration poses inherent revenue volatility risks: delays or reductions from one or both dominant customers could materially affect quarterly sales flows or aggregate annual results especially given milestone recognition practices that occasionally defer revenue until specific triggering events occur.

Despite these risks, Aspen maintains established relationships within these channels underpinning insulation distribution frameworks critical for market access particularly within energy industrial sectors pursuing performance insulation innovations alongside emerging EV battery component needs.

Forecasting Future Growth: Opportunities in EV Thermal Solutions

Looking ahead, growth prospects remain anchored heavily on expanding penetration within the EV battery thermal management market where regulatory trends toward enhanced safety standards and efficiency create rising demand for advanced insulation materials such as Aspen’s PyroThin line [N1][S4].

However, management notes liquidity sufficiency concerns necessitating potential supplementary financing rounds including equity issuances or debt extensions alongside alternative structures such as equipment leasing or government grants aimed at supporting capital-intensive expansions mandated by evolving commercial opportunities in EV and energy markets [S4].

This underscores a balanced outlook: while the market opportunity supports long-term demand growth based on innovative technology application, near-term constraints linked to customer concentration risk profiles warrant careful attention.

Financial Health Deep-Dive: Liquidity, Debt, and Capital Structure

At fiscal year-end December 31, 2025, Aspen held approximately $157 million in cash and equivalents supported by current assets totaling about $242 million against current liabilities near $62 million—yielding a strong current ratio near 3.9 indicating solid short-term liquidity positioning [F1].

Long-term debt obligations are structured under MidCap Loan Facilities comprising a Term Loan Facility originally drawn at $125 million principal plus revolving credit lines capped at up to $100 million subject to borrowing base calculations; availability fluctuated between roughly $17 million mid-year rising toward about $27 million by Q3 amid covenant considerations [S4][S7].

Amendments during May 2025 adjusted borrowing entities including adding subsidiaries reflecting active capital structure management efforts; proceeds were used notably for refinancing convertible notes totaling $150 million enhancing debt profile though leverage remains elevated requiring ongoing scrutiny given cyclical demand sensitivities [S4][S7].

Capital Allocation Decisions Amid Stretched Margins

Capital expenditures declined significantly (-56.6% YoY) juxtaposed against operating cash flows decreasing nearly 28% year-over-year but remaining positive at around $32.9 million for FY2025—the first consistent cash flow recovery following several years of negative operating cash flow ranging from roughly -$42 million up to near -$94 million annually previously recorded [F1].

Free cash flow after subtracting capex stands slightly negative at about -$4.6 million underscoring that capital returns such as dividends or share repurchases have not been prioritized amid sustained net losses (~-$389 million) producing steep negative return on equity near -165% based on latest equity balances around $236 million reflecting accumulated deficit pressure [F1].

Investment focus remains weighted toward preserving liquidity for R&D aimed at sustaining competitive advantages rooted in proprietary PyroThin manufacturing processes rather than distributing cash back currently.

Signs to Monitor: Operational Milestones and Market Dependencies

Investors should watch operational KPIs throughout early 2026 including:

- Progression on milestone invoicing affecting deferred revenue unwind;

- Efforts toward diversifying customer base mitigating existing concentration risks;

- Cost structure improvements linked to Mexico automated facility integration;

- Compliance status with MidCap loan covenants amid historical caution tied to revenue declines;

- Market traction within EV thermal management amid macroeconomic factors influencing EV adoption rates.

These indicators will reveal whether Aspen can translate its technological leadership into sustainable profit improvements beyond top-line volume expansion observed thus far.

This analysis synthesizes Aspen Aerogels’ publicly filed financials through March 23, 2026 ([F1],[S#]) alongside recent earnings disclosures ([N1]). It is intended solely for informational purposes without providing investment recommendations or valuation guidance.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments