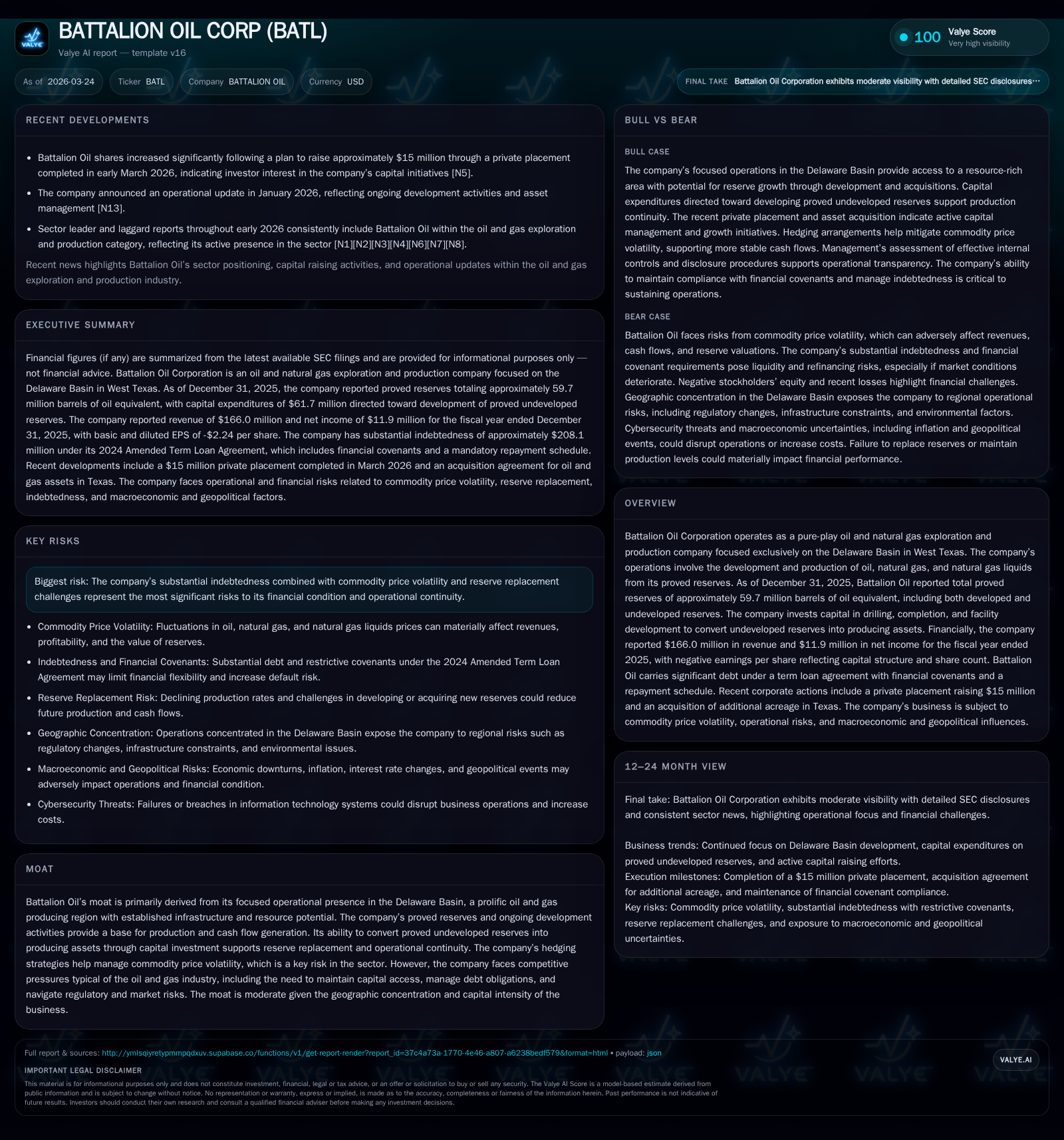

Battalion Oil Corp: Assessing Reserve Challenges and Debt Dynamics in the Delaware Basin

A focused review of Battalion Oil's reserve depletion and indebtedness reveals critical factors shaping its operational and financial outlook.

Battalion Oil Corporation, a Delaware Basin-focused producer, has experienced proved reserves decline from approximately 68.1 MMBoe in 2023 to 59.7 MMBoe in 2025, driven by production rates outpacing extensions and downward revisions linked to commodity pricing changes. Financially, the company saw revenues decrease from $359 million in 2022 to $166 million in 2025 alongside narrowing operating losses and a return to profitability at net income level in 2025 amid capital expenditure cuts. Significant debt outstanding at $208 million with stringent covenants continues to pressure liquidity and capital allocation, constraining investments needed to develop sizeable proved undeveloped reserves estimated at around 40% of total proved reserves. Battalion’s capacity to execute planned capex programs and maintain loan covenant compliance will be pivotal amid shale drilling technical uncertainties and volatile commodity markets.

Evolution of Proved Reserves: Trends and Implications

Battalion Oil’s proved reserves have declined steadily over the past three years according to SEC-filed data [S1]. Total proved reserves dropped from approximately 68.1 million barrels of oil equivalent (MMBoe) at year-end 2023 down to about 59.7 MMBoe by December 31, 2025 — a decline of roughly 12%. This depletion outpaces the extensions and discoveries which contributed only about 4 million barrels equivalent in new reserves during this timeframe.

Production substantially draws down reserves annually, with reported output decreasing total reserves by around 4.6 MMBoe in 2023 followed by further declines through subsequent years [S1]. Additionally, downward revisions totaling about 2.5 MMBoe in earlier periods and nearly three MMBoe more during recent years reflect decreased SEC pricing assumptions ($66 per barrel WTI oil average for calendar year ending Dec-25 vs $76 prior year), dampening reserve valuation [S1][S8].

All of Battalion’s proved reserves are located exclusively within the Delaware Basin — known for prolific but technically challenging shale formations requiring horizontal drilling and hydraulic fracturing techniques [S1]. About 40% of the reserves as of December 31, 2025 (approximately 24.1 MMBoe) remain classified as proved undeveloped (PUD), underscoring significant capital requirements to convert them into developed producing assets [S8].

Development plans estimate capital expenditures totaling around $270 million from 2026 through 2029 necessary for infill drilling and facility construction crucial for bringing PUDs online [S8]. Delays or reductions in this capex spend could risk lease expirations under continuous development clauses common in shale acreage contracts [S1]. This creates tension between preserving resource potential versus managing cash flow amid tight financing conditions.

| Year End | Oil (MBbls) | Natural Gas (MMcf) | NGL (MBbls) | Total Proved Reserves (Mboe) | Developed Reserves (Mboe) | Undeveloped Reserves (Mboe) |

|---|---|---|---|---|---|---|

| Dec-31,23 | 34,622 | 111,749 | 14,860 | 68,107 | 40,129 | 27,978 |

| Dec-31,24 | 34,785 | 105,413 | 12,593 | 64,947 | 36,304 | 28,643 |

| Dec-31,25 | 31,800 | 97,548 | 11,644 | 59,702 | 35,649 | 24,053 |

Proved undeveloped reserves require significant future capital investment; downward revisions driven mainly by price assumptions.

Financial Performance Trajectory: Revenue, Profitability, and Cash Flow Analysis

Financially, Battalion Oil has witnessed notable contraction across top-line metrics since FY2022 highlighted by a revenue decline from $359 million to $166 million by FY2025 representing an aggregate drop largely attributable to commodity price volatility and production fluctuations [F1]. The latest annual revenue reflects a -14.4% decrease relative to FY2024 alone.

Operating income metrics reveal incremental improvement despite remaining negative: FY2024 saw losses of approximately -$11.7 million contracting by nearly half (-43.5%) to about -$6.6 million in FY2025 [F1]. This narrowing loss is concurrent with tighter operational control possibly aided by partial hedging programs intended to stabilize cash flows [S9].

Notably net income swung back into positive territory registering $11.9 million profit for full-year FY2025 after consecutive losses totaling -$32 million and -$3 million during prior two years respectively [F1].

Operating cash flow has increased steadily despite top-line revenue declines reaching $39.1 million (+10.6% YoY), indicating improving operational cash generation capability yet challenged relative to historical highs ($78+ million CFO reported at peak commodity prices level) [F1]. Capital expenditures have fallen precipitously compared with prior cycles but still resulted in negative free cash flow near -$4 million reinforcing ongoing funding gap when measured against development needs.

Historical performance (annual)

| FY | Rev ($mm) | Net ($mm) | CFO ($mm) | OpInc ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 166 | 12 | 39 | -7 | -14.4% | +137.3% |

| 2024 | 194 | -32 | 35 | -12 | -12.2% | -946.0% |

| 2023 | 221 | -3 | 18 | 18 | -38.5% | -116.4% |

| 2022 | 359 | 19 | 79 | 152 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | ROE% |

|---|---|

| 2025 | -36.2 |

| 2024 | -773.8 |

| 2023 | -4.5 |

| 2022 | 21.9 |

Source: SEC companyfacts cache [F1].

Operating losses narrowing; CFO growth positive though FCF remains negative due to capex cuts.

Debt Profile and Covenant Landscape: Navigating Financial Constraints

Debt encumbrance forms a significant structural consideration for Battalion Oil's financial health; as of December 31, 2025 the company carried approximately $208 million aggregate principal indebtedness under its amended term loan facility originated late-2024 with no additional borrowing capacity remaining given existing covenant restrictions [S4][S6]. The facility matures December 26, 2028.

Financial covenants embedded within this agreement include maintaining minimum asset coverage ratios starting at no less than approximately 1.85x up through December 31st, 2026 before increasing thresholds thereafter; total net leverage ratio caps tightening from no greater than roughly 3.20x as of year-end ’25 gradually adjusted upward thereafter contingent on quarterly financial statements; and a current ratio floor near unity enforced monthly beginning early-2025 onwards [S4]. Breach risks here could precipitate default scenarios triggering acceleration or tightened liquidity access.

The loan bears variable rate interest indexed off SOFR plus an applicable margin tiered between roughly +7.75%-8.50% annually corresponding inversely with leverage band classifications updated quarterly adjusting borrowing costs prospectively [S5]. This interest profile coupled with mandatory scheduled amortization payments totaling $22.5 million each during calendar years ’26 & ’27 imposes substantial fixed commitments absorbing available operating cash flows limiting flexibility for reinvestment or opportunistic funding alternatives.

Recent amendments including a second amendment executed November ’25 relaxed some covenant terms temporarily but underscore ongoing need for compliant balance sheet management or alternative restructuring strategies should business execution falter [S4][S6][N6].

Capital Expenditure Retreat: Impact on Reserve Development and Production Growth

Despite future capital commitments essential for reserve maturation outlined at ~$270 million across the next four years targeting PUD conversions predominantly through drilling completions and facility expansion within Delaware Basin assets [S8], actual capital deployment contracted sharply by nearly seventy percent relative to earlier cycles as inferred from historical trends though exact recent capex figures beyond decadal norms are unavailable publicly [F1].

This decline reflects cautious operational spending amidst debt servicing imperatives compounded by macro uncertainty relating both input cost inflation — particularly regarding steel and specialized equipment prices — as well as intensified competitive market dynamics influencing rig availability and hydraulic fracturing service costs regionally [S7][N1][N9].

The downturn raises concerns over leasehold retention risk due to continuous development clauses prevalent across oil & gas acreage documentation mandating timely drilling progress; failure could result in acreage forfeiture diminishing future reserve base if capital spend continues constrained indefinitely [S1][S8]. Moreover horizontal shale reservoir complexities heighten drilling outcome unpredictability further stressing disciplined project selection criteria amid fiscal limits [S1].

Free cash flow impairment remains clear despite improving operating cash inflows — estimated negative ~$4M indicative of underinvestment-driven production plateau risk absent incremental financing solutions or capital efficiency gains.[F1]

Future Prospects: Risk Factors, Strategic Capital Deployment, and Market Position

Battalion Oil’s future trajectory hinges critically on its ability to convert its sizeable PUD inventory into producing wells under tight liquidity conditions while managing exposure concentrated exclusively within the Delaware Basin—a prolific yet regionally nuanced resource play susceptible to supply-demand imbalances impacting transportation bottlenecks and local regulatory intervention risks [S21][S27].

Commodity price volatility remains a persistent threat capable of compressing operating margins severely; mitigating these swings via active hedging strategies contributes some stability though potentially limits upside participation should prices rally sharply beyond locked-in hedge strike prices [S9].

Capital access constraints imposed through debt covenants curtail Battalion’s optionality introducing execution risk concerning timely PUD development schedules essential for sustaining production volumes over medium-term horizons while also raising refinancing concerns upon approaching amortization deadlines requiring significant principal repayments without evident excess borrowing capacity currently available [S6][N6].

Environmental regulations governing hydraulic fracturing practices continue evolving nationally introducing permitting complexities alongside increasing ESG scrutiny that may incrementally elevate compliance costs or restrict operational flexibility impacting cost structures directly or indirectly through stakeholder sentiment pressures [S15][S19].

Overall competitive positioning benefits from focused domain expertise within the Delaware Basin’s infrastructure ecosystem supporting cost-efficient operations contingent upon successful navigation of aforementioned challenges represented moderately defensible moat characteristics albeit constrained materially by external market volatility factors alongside internal financial leverage dynamics.

Monitoring Battalion’s Milestones: Key Performance Indicators to Watch

Future watchers ought focus on several critical KPIs signaling operational progress or headwinds including:

- Quarterly reporting on reserve replacement ratios against production declines indicating sustained resource base health;

- Compliance status updates tied tightly around loan covenant quarterly testing affecting leverage ratios that impact borrowing rates;

- Announcements regarding successful financing rounds including equity raises such as recent proposed $15 million capital influx associated with share price surges evidencing market confidence shifts [N6];

- Production volume statistics reflecting effective conversion of PUDs into developed production;

- Execution adherence against multi-year capex targets signaling strategic discipline. Adverse deviation along any axis would flag heightened risk layers warranting closer scrutiny.

Capital Allocation Policies: Shareholder Returns Amid Financial Pressures

Battalion Oil management currently prioritizes debt reduction and reinvestment over shareholder distributions; consistent with restrictive covenants precluding dividends or stock buybacks observed throughout recent filing periods preventing typical shareholder return mechanisms given heightened leverage burdens impeding ROE recovery evidenced around negative ~36% based on latest net income-to-equity ratio where equity is deeply negative at -$33 million reflecting accumulated losses inclusive of preferred stock impacts diluting common shareholders financially [F1][S14][S17].

Historical buyback activity is negligible post-bankruptcy reorganization events while dividend declaration absence persists aligned closely with maintenance of liquidity amid cyclical industry headwinds confirming prudent conservatism amidst structural remediations underway.

Disclaimer: This analysis draws exclusively upon legally filed financial disclosures ([F1], [S#]) combined with reputable news sources ([N#]) without projecting non-documented forecasts or making investment recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments