AGNC Investment’s Leverage and Portfolio Composition Shape Its Earnings Resilience

AGNC Investment Corp. combines active management of Agency RMBS with measured leverage to sustain growth amid interest rate variability.

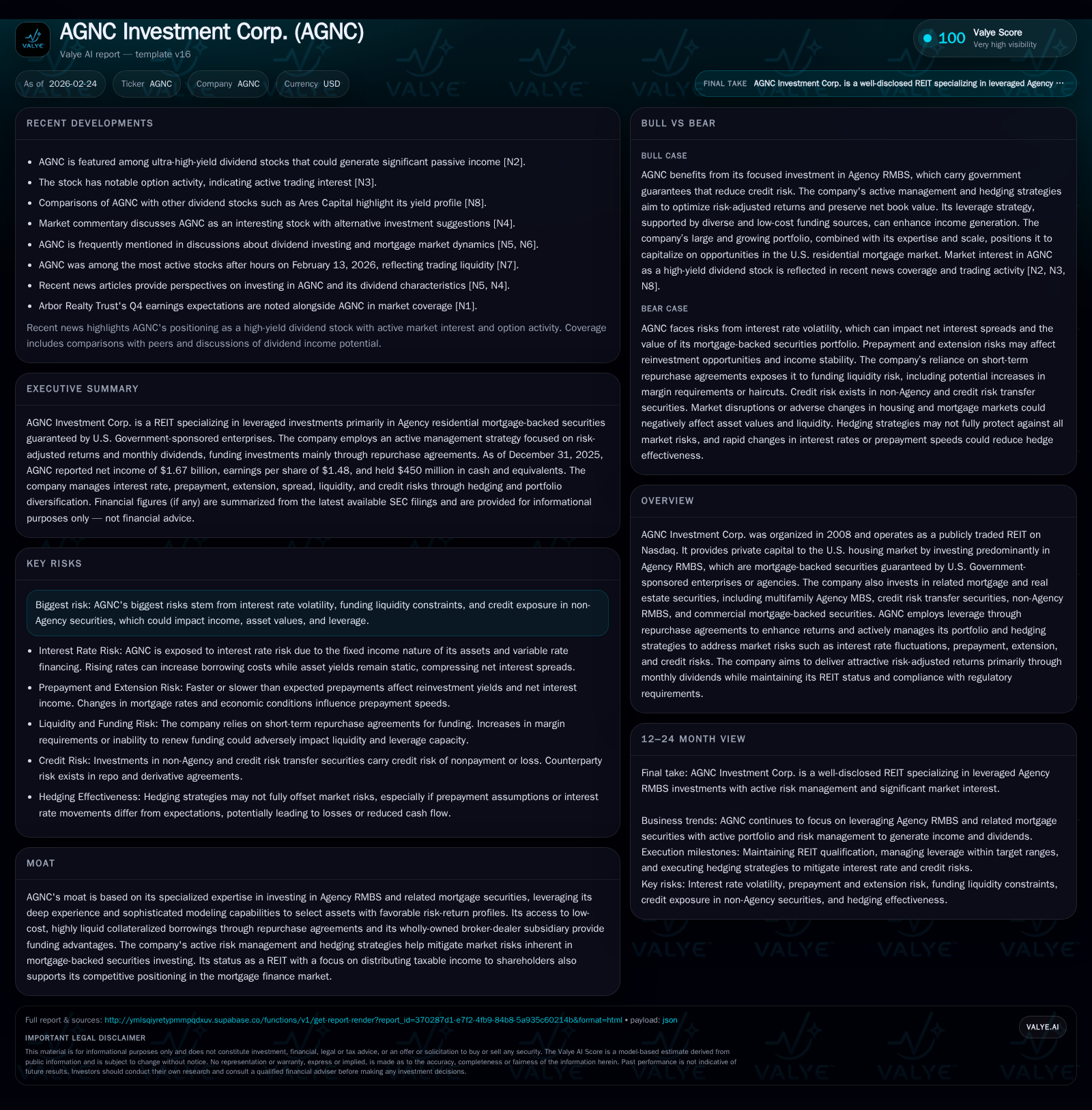

AGNC Investment Corp., a Nasdaq-listed REIT focused predominantly on Agency residential mortgage-backed securities (RMBS), reported strong net income growth in 2025 on a rising asset base and efficient leverage. The company’s active portfolio and hedging strategies aim to mitigate risks inherent in mortgage-backed securities investing, particularly interest rate fluctuations and liquidity constraints. While distributed dividends remain steady, future earnings hinge on managing exposure to market volatility and maintaining access to low-cost repo funding.

Company Background and Business Model

Founded in 2008, AGNC Investment Corp. is a publicly traded real estate investment trust (REIT) focused primarily on investing in U.S. Agency residential mortgage-backed securities (RMBS). These consist mainly of pass-through certificates and collateralized mortgage obligations guaranteed by government-sponsored enterprises (GSEs) such as Fannie Mae and Freddie Mac or a government agency like Ginnie Mae [S11]. AGNC also selectively invests in multifamily Agency MBS, credit risk transfer (CRT) securities, non-Agency RMBS, and commercial mortgage-backed securities (CMBS), broadening its exposure within mortgage markets.

Operating as an internally managed REIT listed on Nasdaq under the symbol "AGNC," the company aims to provide stockholders attractive risk-adjusted returns driven largely by monthly dividend distributions [S11]. To achieve this, AGNC employs active portfolio management tactics along with dynamic hedging strategies that tackle interest rate risk, prepayment rates, extension risk, credit exposure, and liquidity constraints inherent in mortgage-backed assets.

Notably, AGNC leverages its investments via collateralized repurchase agreements (repo), which offer short-term secured financing at relatively low cost due to high liquidity in Agency RMBS markets [S5][S6]. Further funding diversification is attained through its wholly owned broker-dealer subsidiary Bethesda Securities, LLC (BES), which accesses bilateral and tri-party repos including the Fixed Income Clearing Corporation's General Collateral Finance Repo service—lowering overall funding costs while reducing counterparty risk concentration [S10].

Historical Financial Performance: Growth Drivers and Profitability

AGNC Investment has exhibited robust growth over recent years underpinning strong operational performance. Key financials from fiscal years 2023 through 2025 illustrate substantial expansion:

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | Net YoY |

|---|---|---|---|

| 2025 | 1670 | 653 | +93.5% |

| 2024 | 863 | 86 | +15.2% |

| 2023 | 749 | -118 | +162.9% |

| 2022 | -1190 | 1013 |

Note: Omitted columns lack sufficient annual XBRL coverage in the provided tags (need ≥2 annual points): Rev, OpInc, Capex, FCF. Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($mm) | Buybacks ($mm) | ROE% |

|---|---|---|---|

| 2025 | 1601 | 13.5 | |

| 2024 | 1241 | 0 | 8.8 |

| 2023 | 1005 | 0 | 9.1 |

| 2022 | 869 | 51 | -15.1 |

Source: SEC companyfacts cache [F1].

*Leverage represents tangible net book value "at risk" ratio including repurchase agreements & TBA positions [F1][S12][S13].

The near doubling of net income from $863 million in 2024 to $1.67 billion in 2025 was driven chiefly by expanding net interest income—rising from marginally positive $18 million in 2024 to $675 million in the latest year—reflecting growing asset scale combined with slightly reduced interest expense costs [F1][S1]. Enhanced other gain components totaling approximately $1.12 billion versus $955 million the prior year also contributed materially to earnings growth.

Dividends paid remained substantial at approximately $1.6 billion in fiscal year 2025 with dividends per common share steady at $1.44 annually over the three years surveyed; reflecting the company's commitment to stable income return critical for REIT qualification [F1][S21]. Meanwhile operating expenses have remained contained around the ~$110–$130 million range despite escalating assets under management.

Total equity rose sharply from approximately $9.8 billion at end-2024 to $12.4 billion at end-2025 fueled partly by retained earnings alongside capital raised via at-the-market equity offerings during the period [F1][S21]. This equity build supports expanded portfolio investments without excessive reliance on debt beyond historically targeted leverage bands.

Operating cash flow advanced significantly—from just $86 million positive in fiscal 2024 to a robust $653 million inflow in fiscal year 2025—signifying improved cash conversion of reported earnings and better working capital management [F1]. This turnaround reduces stress related to margin calls or sudden liquidity needs characteristic of highly leveraged mortgage REITs.

Portfolio Composition and Risk Management

A cornerstone of AGNC's competitive moat lies in deep specialist expertise selecting predominantly Agency RMBS with attractive risk-return profiles backed by GSE guarantees [S11]. As of December 31, 2025, the fair value of Agency securities held was approximately $81 billion representing about a vast majority of total investments near $81.8 billion versus smaller allocations across CRT ($606 million), non-Agency RMBS ($95 million), CMBS exposures and U.S Treasury securities ($13.5 billion) for liquidity [S24][F1].

The company actively manages financing risks leveraging short-term repurchase agreements discounted off benchmark rates while tactically employing forward-settling TBA dollar roll contracts that generate incremental income through price drops between settlement dates [S10]. AGNC maintains leverage ratios generally targeting six to ten times tangible stockholders’ equity but remained near lower-midpoint range of ~7.2x at year-end [S12][S13].

Interest rate sensitivity is crucial given fixed-income nature of assets versus variable or short-term borrowing costs [S25]. To mitigate duration mismatches—where asset yields lag rising borrowing costs—and prepayment uncertainties AGNC employs complex derivative instruments including swaps/swaptions along with futures contracts tied to U.S Treasury indices that form part of an intricate hedge program designed to cushion net interest margins against volatility [S7][S11]. As of year-end the estimated duration gap inclusive of hedges was around +0.4 years implying careful balance between asset-liability sensitivities but retaining some positive exposure benefiting if rates decline sequentially.

Credit risk concentrates mostly within non-Agency holdings though these represent a minor portion overall allowing tighter control through rigorous due diligence plus post-acquisition monitoring with options for credit default swaps where warranted [S25]. The GSE-backed RMBS carry virtually no credit loss risk due their guarantees.

Liquidity remains well supported by cash reserves (~$450 million cash plus restricted cash ~$1.3 billion), diversified repo counterparties via Bethesda Securities’ activities granting improved depth beyond conventional bilateral repo markets and ongoing receipts of principal/interest payments from mortgage pools invested [S9][S10][F1]. However substantial reductions in collateral values or spikes in margin call haircuts could force asset sales potentially pressuring realized gains.

Capital Allocation: Dividends Steady amid Opportunities for Share Buybacks

Maintaining REIT tax status mandates distributions annually at a minimum of roughly 90% taxable income which AGNC targets at effectively distributing nearly all annual taxable income through monthly common dividends [S21]. In line with this policy dividends per share stayed fixed at $1.44 even as net income surged substantially.

Capital raising from equity markets using At-the-Market Offering programs has funded recent balance sheet expansion while currently open share repurchase authorizations amounting up to $1 billion remain unused suggesting flexibility pending future earnings outlook or share price valuation considerations [F1][S21]. Given steady distributions without buybacks over last three years implies cautious capital stewardship prioritizing reinvestment opportunities or leverage maintenance over direct shareholder returns beyond dividends.

Outlook: Growth Drivers and Constraints

Explicit forward guidance was not disclosed; thus investors should watch for updates on several fronts:

- Changes in interest rate regimes affecting both borrowing costs and prepayment speeds that influence asset duration/convexity dynamics.

- Efficacy of hedging programs especially under volatile market conditions where assumptions on prepayment rates might misalign.

- Continued access to favorable repo financing excluding significant haircut increases that would challenge leverage deployment.

- Portfolio pivot between Agency versus non-Agency allocations responding to spread opportunities while managing credit risk prudently.

- Equity issuance cadence balancing dilution impact with capital needed for accretive asset purchases.

The macroeconomic backdrop remains complex shaped by Fed monetary policies impacting short-term rates that drive funding expense benchmarks along with housing market developments influencing underlying collateral performance [N13]. The depth offered by BES subsidiary uniquely positions AGNC among mREIT peers for liquidity resilience but must be vigilantly managed given systemic reliance on repo markets.

Conclusion

AGNC Investment Corp.’s demonstrated ability to grow its investment base nearly doubling net income year-over-year stems from disciplined portfolio growth centered on Agency RMBS augmented with sophisticated financing via diverse collateralized repo markets accessed through a captive broker-dealer structure. Its active hedging strategy tempers interest rate risks characteristic of mREITs yet remains sensitive to market dynamics requiring continuous oversight.

Operating cash flow improvements signal enhanced earnings quality complementing stable dividend payments consistent with REIT objectives. As leverage levels keep within historically targeted ranges coupled with ample liquidity buffers the firm stands poised for incremental growth though vigilance over funding conditions and spread environment will determine near-to-medium term upside potential.

This analysis is based solely on information publicly available through regulatory filings and reputable news sources as of February 24, 2026, without offering investment advice.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments