DigitalOcean’s Scaling AI Cloud Platform Drives Record Profit Amid Debt Leverage

DigitalOcean leverages its agentic inference cloud to accelerate growth while navigating competitive and capital structure challenges.

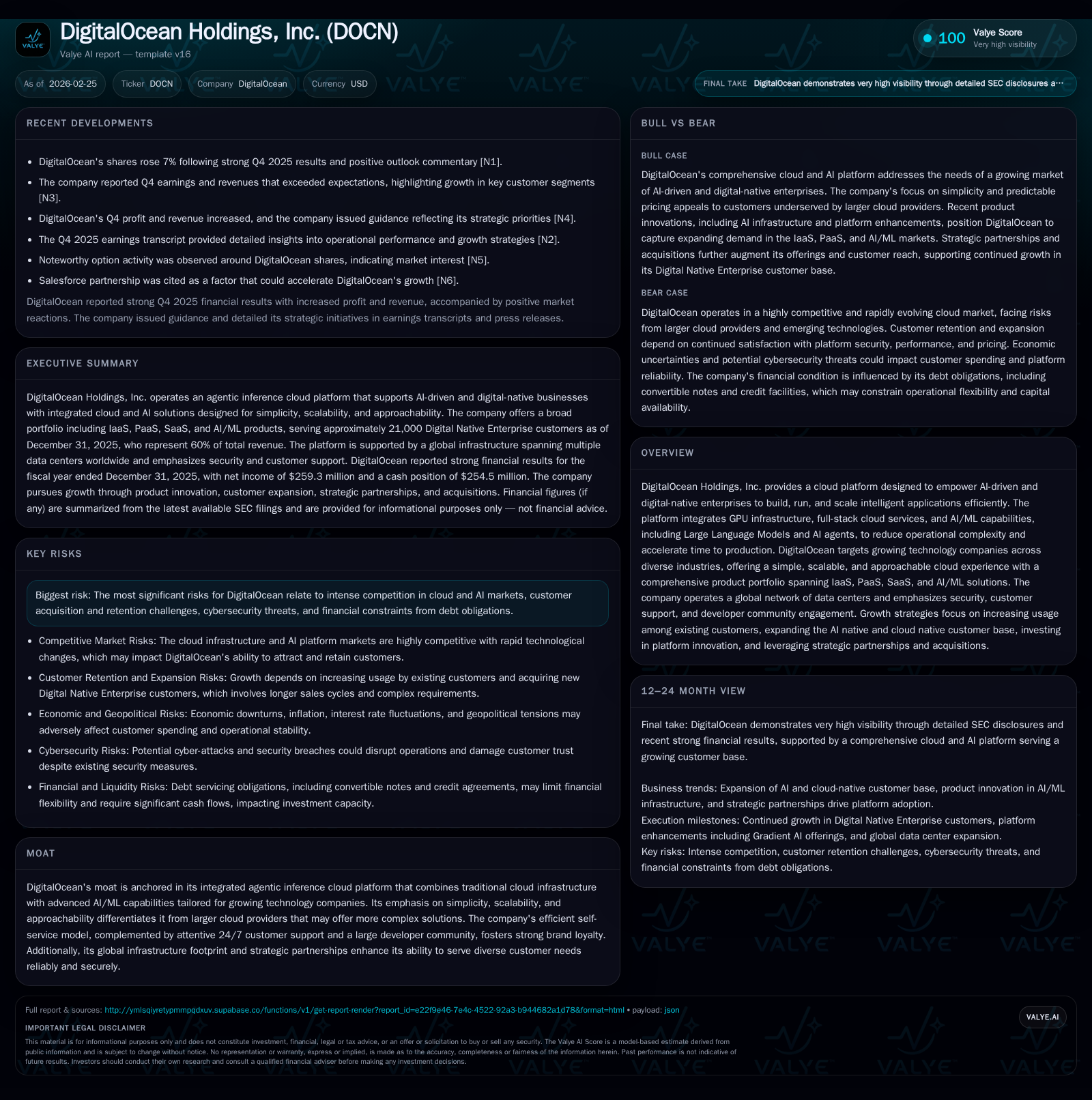

DigitalOcean Holdings, Inc. has demonstrated strong operational momentum through 2025, achieving substantial profitability growth following investments in AI-native cloud capabilities and a growing base of Digital Native Enterprises (DNEs). The company’s focus on simplicity, scalability, and approachability in delivering integrated IaaS, PaaS, SaaS, and AI/ML solutions differentiates it in a competitive market dominated by mega cloud providers. While revenue data is undisclosed, key metrics such as ARR growth and expanding DNE customer engagement signal robust future prospects. However, leverage from significant convertible note issuance and a tight current ratio underscore liquidity risks in an evolving regulatory and competitive landscape.

Historical Performance Overview

DigitalOcean Holdings has undergone a remarkable financial transformation over recent years. Operating income turned positive definitively in FY2023 at $11.9 million from a $25.7 million loss in FY2022. This was followed by accelerated improvement to $32.5 million in FY2024 and a near fivefold jump to $157.0 million in FY2025 [F1]. Net income followed suit climbing from net losses of $27.8 million in FY2022 to sequential net profits of approximately $19.4 million in FY2023, $18.3 million in FY2024 and soaring to $259.3 million in FY2025 — an outstanding YoY increase exceeding 1300% [F1].

Operating cash flow has steadily risen year-over-year from $195.2 million in FY2022 to over $309.6 million last year while capital expenditures peaked at $178.2 million in FY2024 before being trimmed down by 27.5% to roughly $129.1 million in FY2025 as the company optimized its data center expansion cycle [F1]. These cash flow trends underpin an approximate free cash flow generation of roughly $180.5 million for FY2025.

Yet, balance sheet metrics reveal some liquidity tensions with current liabilities surpassing current assets ($619M vs. $427M) yielding a current ratio of just 0.69 [F1]. Shareholders’ equity remains negative at about -$29 million at year-end 2025 reflecting cumulative losses offset partially by equity issuance [F1]. The company continued to repurchase shares totaling over $82 million during the year, scaling back buybacks from prior heftier levels [F1].

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|---|

| 2025 | 259 | 310 | 157 | 129 | +1319.4% |

| 2024 | 18 | 283 | 33 | 178 | -5.9% |

| 2023 | 19 | 235 | 12 | 119 | +169.8% |

| 2022 | -28 | 195 | -26 | 106 |

Note: Omitted columns lack sufficient annual XBRL coverage in the provided tags (need ≥2 annual points): Rev, Div. Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Buybacks ($mm) | FCF ($mm) | ROE% |

|---|---|---|---|

| 2025 | 82 | 181 | -903.7 |

| 2024 | 60 | 105 | -9.0 |

| 2023 | 488 | 116 | -6.2 |

| 2022 | 600 | 89 | -58.4 |

Source: SEC companyfacts cache [F1].

Note: Revenue not disclosed; ROE negative due to shareholder deficit.

Business Model & Product Differentiation

DigitalOcean’s focus targets "Digital Native Enterprises"—technology companies typically under 500 employees—that benefit from easy-to-use cloud infrastructure combined with integrated AI/ML stacks [S6][S12][S14]. The core platform spans IaaS offerings such as Droplets (virtual machines), flexible storage options including Spaces (object storage), Volumes (block storage), plus PaaS/SaaS managed hosting services such as Kubernetes and databases.

Notably, the Gradient® AI Agentic Cloud offers specialized GPUs via AMD and NVIDIA hardware tailored for AI workloads including Large Language Models (LLMs), Jupyter Notebooks environments for ML experimentation, bare metal GPU servers for customization, and serverless AI pipelines facilitating seamless deployment of intelligent agents [S7][S14]. This unified infrastructure enables customers to run traditional compute alongside advanced AI models without juggling disparate platforms—a distinctive moat setting DigitalOcean apart from sprawling hyperscale providers often focused on larger enterprise deals [S24][S27].

Customer engagement is further enhanced by extensive community support structures involving technical documentation, tutorials, hackathons like Hacktoberfest with tens of thousands contributions annually, global meetups through Deploy conferences across North America and Europe, plus Hatch programs nurturing startup founders [S16]. This fosters brand loyalty which underpins stable net dollar retention rates that improved from about 98% to roughly 100% between 2024-25 amid expanding usage per customer [S13][S14].

Growth Prospects & Catalysts

Several interlinked growth drivers stand out:

- Expanding DNE Customer Base: The number of customers classified as Digital Native Enterprises spending more than $500 monthly increased from approximately 18k to nearly 21k year-over-year [S8][S14], raising ARR from roughly $820 million to about $970 million.

- AI & Cloud-Native Adoption: Dedicated AI sales teams deepen penetration into AI-first enterprises while migration service expansions support workload shifts away from incumbent large providers [S11][S13][N9].

- Product Innovation: Recent releases include advanced GPU-powered capabilities; enhanced networking (e.g., VPC support); autoscale pools for Droplet compute; flexible backup scheduling/pricing; Managed Caching; multi-cloud partner connectivity; and capability-rich enhancements to the Gradient AI platform like the Agent Development Kit enabling faster agent creation [S13][S14].

- Platform Investments: IDC estimates relevant IaaS/PaaS markets serving businesses under 500 employees will grow at a CAGR ~22% through 2028 providing a healthy TAM backdrop.

- Community Ecosystem: Developer education initiatives continue fueling organic mindshare gains which are strategically converted into commercial relationships [S16].

- Strategic Partnerships & Acquisitions: While organically driven currently, strategic partnerships aim to augment reach particularly into international markets.

These factors collectively suggest sustained top-line momentum although official revenue figures are not publicly reported yet [N1][N3][N4]. Management targets further elevating net dollar retention above parity to drive expansion revenue.

Risks & Constraints

Despite promising operational traction several notable headwinds remain:

- Intense Competition: Giants like AWS, Azure and Google Cloud dominate with vast resources offering deeply integrated enterprise solutions difficult to match on breadth [S24][S27]. Smaller niche players also contest portions of the SMB market.

- Customer Retention & Acquisition Complexity: Larger DNE customers can have longer sales cycles with complex requirements increasing upfront costs without guaranteed conversion or expansion [S10].

- Leverage & Liquidity Pressure: With over half a billion dollars tied up in convertible notes due later this decade coupled with modest cash reserves relative to short term obligations ($254M cash vs $619M current liabilities), DigitalOcean faces refinancing risks particularly if credit markets tighten or internal cash generation slows [S5][F1][S20][N4].

- Regulatory Uncertainty: Emerging legal frameworks around AI/ML are evolving rapidly globally; compliance complexity could inflate costs or restrain product rollout speed [S17][S23][S26]. Simultaneously cyberscurity threats require continued investment.

- Negative Equity Position: The sustained negative shareholders’ equity position limits financial flexibility despite positive earnings recently reported [F1].

Capital Allocation & Returns Perspective

The sharp rise in operating income translating into strong positive net income along with robust operating cash flows suggests improving underlying return metrics although traditional ROE remains negative due to shareholders deficit [$(-903") return approx based on net income/equity] [F1].

Capital expenditure was scaled back after peaking during heavy data center investments indicating better capital efficiency going forward while share buybacks totaling $82 million indicate management’s intention to return capital amid rising profits despite debt presence suggesting measured confidence but also conservative governance [F1].

No dividends have been declared or indicated as per available data.

Outlook & Key Milestones To Watch

While explicit earnings guidance was provided during early-year disclosures emphasizing continued ARR growth driven by AI workload adoption and migration wins along with steady expansion of DNE customers [N2][N4], absence of full revenue disclosure means observers should monitor:

- Quarterly ARR updates and net dollar retention trends.

- Customer count progression focused on high-value DNE segments.

- Platform feature velocity especially within Gradient® AI advances.

- Sales funnel health metrics including migration pipeline conversions.

- Liquidity ratios and refinancing activities connected with convertible note maturities or credit facility utilization.

- Competitive responses particularly pricing pressure or feature parity announcements from hyperscalers.

Conclusion

DigitalOcean Holdings exemplifies a fast-scaling cloud innovator successfully marrying simplified user experience with cutting-edge AI infrastructure tailored primarily for fast-growing digital startups rather than enterprise incumbents dominating the hyperscale cloud market segment today. Its agentic inference cloud platform backed by committed developer communities provides a distinct competitive niche leveraged well through efficient self-service distribution complemented by increasingly sophisticated direct sales motions targeting AI-native enterprises.

The pronounced financial turnaround culminating in record profitability in FY2025 amidst sizeable investments aligns well with management’s strategy focusing on expanding high-value DNE customers leveraging innovative GPU-powered products designed for modern ML workflows beyond conventional IaaS/PaaS offerings.

However, considerable leverage alongside evolving regulatory pressure related to AI alongside intense competition requires prudent monitoring given the still fragile balance sheet position despite improving operating metrics.

This comprehensive profile underscores that DigitalOcean’s future hinges upon maintaining its simple yet powerful value proposition while scaling efficiently within shifting technological paradigms shaped by AI’s rapid advancement.

Disclaimer: This analysis is provided solely for informational purposes without any investment advice or recommendations regarding securities or issuer engagement.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments