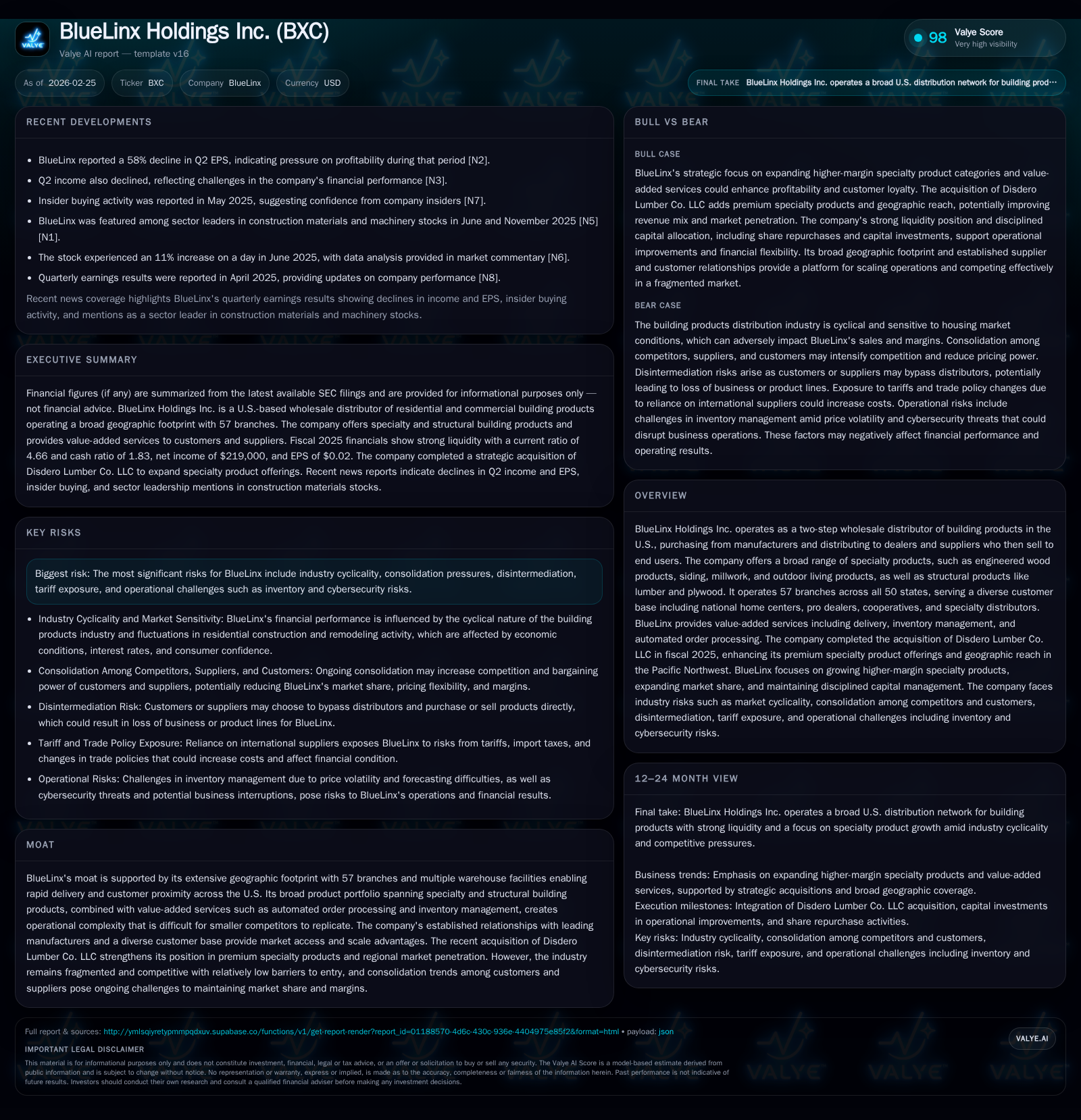

BlueLinx Holdings Faces Earnings Pressure Despite Expanding Specialty Product Reach

The company’s growing specialty product offerings and geographic footprint contrast with significant declines in profitability amid industry headwinds.

BlueLinx Holdings Inc. strategically expanded its specialty building product portfolio and regional reach through the acquisition of Disdero Lumber Co., aiming to boost higher-margin sales segments. Despite relatively stable revenues around $893 million, the company experienced steep reductions in operating and net income for fiscal 2025, reflecting significant margin compression. Industry consolidation among customers and suppliers, disintermediation risks, and tariff exposures compound operational challenges. While cash flows remain positive, returns on equity are near zero, and management’s capital allocation includes substantial share repurchases despite earnings pressures. Investors should monitor integration of specialty products, shifts in distribution channel mix, and evolving trade policies.

Historic Sales and Profitability Trends Reveal Mounting Margin Pressures

BlueLinx Holdings Inc.'s financial trajectory over recent years shows revenue stability alongside steep declines in profitability metrics [F1]. Fiscal year 2025 revenue was essentially flat compared to prior years at about $893 million. However, operating income dropped by nearly 63% year-over-year to approximately $32.5 million from $87.6 million in FY2024, signaling significant margin pressure likely due to cost inflation and pricing challenges.

Net income collapsed to $219 thousand—a decline of almost 99.6% YoY—despite stable top-line performance [F1]. Operating cash flow also declined by nearly 30% YoY to about $59.7 million but remained positive amid earnings erosion. Capital expenditures decreased by approximately one-third to $26.9 million, indicating more disciplined or deferred investment under uncertain conditions.

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|---|

| 2025 | 0 | 60 | 32 | 27 | -99.6% |

| 2024 | 53 | 85 | 88 | 40 | +9.4% |

| 2023 | 49 | 306 | 138 | 28 | -83.6% |

| 2022 | 296 | 400 | 439 | 36 |

Note: Omitted columns lack sufficient annual XBRL coverage in the provided tags (need ≥2 annual points): Rev, Div. Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Buybacks ($mm) | FCF ($mm) | ROE% |

|---|---|---|---|

| 2025 | 38 | 33 | 0.0 |

| 2024 | 45 | 45 | 8.2 |

| 2023 | 42 | 279 | 7.7 |

| 2022 | 66 | 364 | 50.2 |

Source: SEC companyfacts cache [F1].

Note: Exact annual revenue figures for FY2023-24 are not available from provided data.

Margin compression reflects rising input costs including tariffs and freight combined with softened pricing power amid intense competition and customer consolidation [S4][S8]. The company's two-step distribution model entails fixed costs such as warehousing that exacerbate margin cyclicality when volumes or prices decline.

Strategic Expansion via Disdero Lumber Acquisition

In Q4 FY2025, BlueLinx acquired Disdero Lumber Co., a distributor specializing in premium specialty building materials primarily serving upscale residential and commercial projects in the Pacific Northwest [S6][S7]. This acquisition strengthens BlueLinx's presence in higher-margin specialty categories such as decking, trim, flooring, paneling, posts, timbers, siding, and stepping.

Specialty products accounted for approximately 69% of net sales in FY2025 versus structural commodities at about 31%, underscoring a strategic shift towards engineered wood products (EWPs), siding, millwork, outdoor living products, and industrial goods that generally command better gross margins [S11]. The acquisition was funded with cash on hand.

BlueLinx operates an extensive national network with branches across all U.S states and value-added services including automated order processing via EDI, inventory stocking programs tailored for frequent reorder patterns, job-site delivery options for less-than-truckload shipments, milling/fabrication services adjacent to warehouses, and take-off estimation tools to optimize procurement accuracy [S5][S6]. These enhance customer reliance beyond simple product supply.

Industry Dynamics: Consolidation Risks and Tariff Exposure

The U.S building products distribution industry remains fragmented but is undergoing consolidation among customers (national home centers, pro dealers) and suppliers [S4][S8]. This consolidation increases purchasing power concentration that pressures distributor margins through demands for volume discounts or consignment arrangements.

Disintermediation risk arises as large customers or suppliers may bypass distributors by sourcing or selling directly through vertical integration or direct-to-customer models [S4]. This threatens BlueLinx's revenue base and pricing leverage.

Additionally, reliance on imported materials exposes the company to tariff-related cost volatility from changing U.S trade policies impacting commodity wood products or composites from Canada or Asia [S4][S28]. Such factors compress margins if cost increases cannot be passed downstream.

Distribution Channels: Warehouse Dominance Amid Capital Intensity

BlueLinx distributes products mainly via three channels: warehouse sales (80%), reload sales (subset within warehouse-related activities), and direct sales (19%) [S5]. Warehouse sales involve inventory ownership allowing rapid fulfillment but require significant working capital tied up in inventory holding costs.

Reload sales utilize third-party locations near ports or strategic customers to optimize freight efficiency for bulky imports [S5]. Direct sales ship manufacturer products directly to customers without inventory possession by BlueLinx yielding lower margins but minimal capital requirements.

Changes in channel mix affect profitability; increased direct sales dilute average margins whereas growth in warehouse/reload channels can improve margin but increase capital intensity.

Capital Allocation: Buybacks Amid Earnings Decline

Despite near breakeven net income (~$219k), BlueLinx repurchased approximately $38 million of shares in FY2025 following robust buybacks of $45 million in FY2024 [F1][S10]. This indicates commitment to shareholder returns despite weakening profit metrics.

Capital expenditures declined by nearly one-third YoY from about $40 million to $27 million possibly reflecting cautious investment post-acquisition or margin pressures limiting discretionary spend [F1].

Liquidity remains strong with a current ratio of approximately 4.66x supported by over $385 million cash balance at fiscal year-end alongside equity exceeding $617 million providing solvency buffers [F1][S14].

Return on equity approximates zero given negligible net income relative to substantial equity base—highlighting low profitability efficiency despite scale.

Dividends paid are not disclosed in the provided tags; therefore dividend policy details are unavailable.

Outlook: Growth Prospects Balanced by Market Risks

Management focuses on growing higher-margin specialty products leveraging the Disdero acquisition while expanding value-added services including technology enablement such as EDI automations aimed at enhancing customer experience [S10].

Growth drivers include multi-family residential construction demand where engineered wood products are increasingly utilized alongside geographic expansion supported by branch infrastructure.

Risks persist from ongoing customer/supplier consolidation constraining pricing leverage; disintermediation threats; tariff volatility; inventory management challenges amid commodity price fluctuations; cybersecurity risks; labor cost pressures; and regulatory compliance burdens [S4][S12][S16][S18][S20].

No explicit forward-looking financial guidance was provided requiring investors to monitor quarterly results closely along with operational metrics such as Days Inventory Outstanding.

Investor Considerations: Key Metrics to Watch

- Quarterly operating income margin trends indicating ability to stabilize profitability.

- Integration progress of Disdero reflected in specialty segment performance disclosures.

- Distribution channel mix shifts impacting capital intensity and margins.

- Updates on U.S trade policies affecting tariff exposure especially for engineered wood composites critical within specialty segments.

- Competitive landscape evolution including further consolidation among distributors impacting market structure.

- Working capital management effectiveness balancing inventory availability against capital usage under volatile commodity prices.

- Operational cost control initiatives amid labor relations dynamics including workforce unionization considerations.

Disclaimer: This analysis is based solely on publicly available SEC filings as of February 25th, 2026 without speculative projections beyond stated disclosures or verified news reports. No investment advice is provided herein.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments