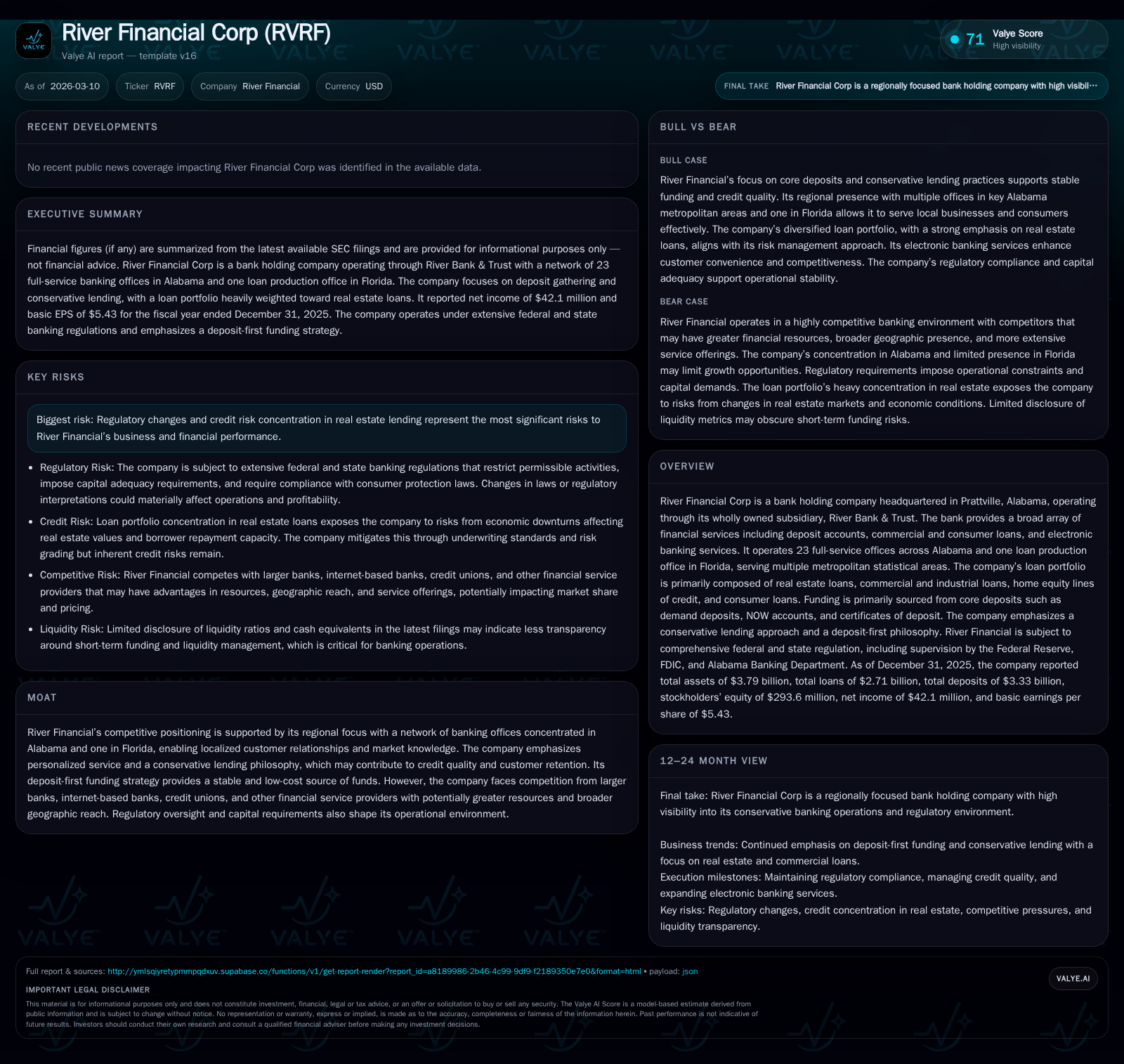

River Financial Corp’s Growth and Risk Profile Reflect Conservative Regional Banking

River Financial’s focus on core deposits and real estate lending underpin its historical income growth and position it for measured future expansion amid regulatory and market challenges.

River Financial Corporation, through its wholly owned subsidiary River Bank & Trust, operates primarily in Alabama and the Florida Panhandle with a conservative regional banking model emphasizing deposit-first funding and real estate lending predominance. Its historical financial performance reveals robust net income growth driven by loan portfolio expansion, supported by strong operating cash flows and disciplined capital investment. The company's prudent underwriting practices, capital adequacy compliance under Basel III, and steady dividend growth reflect a balance between growth ambitions and risk management. Looking forward, River Financial’s prospects hinge on local economic conditions and real estate market dynamics, with regulatory constraints and credit concentration risks as key challenges.

Historical Performance: Robust Income Growth Fueled by Loan Portfolio Expansion

Over the four most recent fiscal years ending 2025, River Financial Corp demonstrated strong financial growth highlighted by a significant increase in net income and operating cash flow. Net income rose from $27.9 million in 2022 to $42.1 million in 2025—a compounded annual increase underscored by a notable 34.4% year-over-year jump in FY2025 alone [F1]. Operating cash flow followed a similarly upward trajectory, growing 46.3% in FY2025 to $53.7 million after a dip in 2023 which reversed into robust cash generation by year-end 2025 [F1].

Capital expenditure nearly doubled from $3.68 million to $8.48 million between FY2024 and FY2025, reflecting investments likely aimed at infrastructure or technology enhancements supporting operational scalability and compliance demands [F1]. Meanwhile, total equity expanded by approximately 29% in the latest year reaching $293.6 million with return on equity sustained near 14.3%, indicative of efficient equity utilization amid expanding asset base [F1].

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|

| 2025 | 42 | 54 | 8 | +34.4% |

| 2024 | 31 | 37 | 4 | +17.1% |

| 2023 | 27 | 24 | 8 | -4.3% |

| 2022 | 28 | 47 | 6 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($mm) | Buybacks ($mm) | FCF ($mm) |

|---|---|---|---|

| 2025 | 4 | 2 | 45 |

| 2024 | 4 | 3 | 33 |

| 2023 | 3 | 1 | 17 |

| 2022 | 3 | 1 | 42 |

Source: SEC companyfacts cache [F1].

Table: River Financial Corp Annual Financial Summary

Loan Portfolio Composition and Lending Philosophy: The Pillars of Stability

River Bank & Trust’s lending approach is grounded in a conservative philosophy primarily focused on real estate loans that accounted for approximately $2.1 billion or about 76.6% of total loans as of December 31, 2025 [S1, S6]. Real estate lending segments consist chiefly of commercial real estate term loans—variable or fixed rate with amortizations up to typically 25 years—and residential first mortgages usually structured with fixed or adjustable rates for maturities spanning from 15 to 30 years [S6–S10]. Construction and land development loans are also variable rate but shorter-term (up to two years), designed to manage collateral risk prudently [S6].

The bank employs standardized yet locally informed underwriting criteria leveraging financial statement analysis for recourse-based loans complemented by collateral assessment [S7–S8]. Commercial loan officers carry responsibility for assigning risk grades based on borrower data plus external economic conditions; consumer loans are assessed primarily through borrower credit scores and debt ratios alongside repayment history with the bank [S4]. This bifurcated risk rating methodology reflects tailored risk management consistent with prudent industry practice.

Non-real estate loans—namely commercial and industrial (C&I) loans—represent roughly $427 million (15.9%) with underwriting focused on cash flow ability coupled with appropriate collateralization; consumer loans form a small residual portion (~2%) under similarly cautious evaluation standards emphasizing borrower income stability and past creditworthiness [S8–S10].

Deposit Funding Strategy: Core Deposits as a Competitive Advantage

The company’s "deposit first" philosophy emphasizes generating stable funding principally via core deposit products such as demand deposits including checking accounts (NOW accounts), savings deposits, money market accounts, and certificates of deposit (CDs) [S1, S5]. Core deposits accounted for the vast majority of River Financial’s $3.33 billion deposits at year-end 2025 providing a low-cost funding base critical amid competitive pressures from internet banks and credit unions offering alternative rates or convenience features.

Deposit rates are actively managed on a weekly basis by senior management who strive to maintain competitiveness without undermining margin stability [S5]. The bank supplements these organic deposit sources occasionally through brokered CDs when strategic or pricing conditions warrant incremental wholesale funds; however, the fundamental reliance remains deeply rooted in customer relationship-driven transactional deposits demonstrating resilience during rate fluctuations.

Capital Adequacy and Regulatory Capital Compliance: Strong Buffer Amid Evolving Standards

River Financial complies fully with Basel III capital requirements inclusive of minimum Tier 1 common equity risk-based ratios supplemented by the mandatory capital conservation buffer of 2.5%. This combination raises effective minimum capital ratios—to for example a common equity Tier 1 ratio of at least 7%, Tier 1 ratio at least 8.5%, and total capital ratio at least 10.5%—ensuring robust resilience against stress scenarios and adherence to supervisory expectations from both FDIC and Alabama Banking Department regulators [S6, S9].

Although eligible for simplified Community Bank Leverage Ratio (CBLR) treatment—which streamlines regulatory complexity for banks below $10 billion in assets—the company has elected not to utilize this option preferring the established Basel III framework to accurately reflect its risk exposures [S11]. This choice aligns with continued emphasis on transparency around capital adequacy given its regional market footprint.

Regulatory oversight significantly affects dividend policies with dividend payments subject not only to profit availability but also restrictions imposed when preservation of capital buffers is requisite per supervisory directives or prompt corrective action frameworks under federal statutes [S9].

Shareholder Returns: Dividends, Buybacks, and Capital Allocation Trends

Dividend payouts have trended upward congruently with earnings progression rising from approximately $2.9 million paid out in FY2022 to around $4.19 million paid in FY2025 [F1], underscoring commitment to rewarding shareholders while retaining earnings sufficient for balance sheet strengthening.

Share repurchase activity has been more modest but persistent—a cumulative presence ranging between $1 million and $2.56 million annually over recent years—reflecting cautious use of excess capital given regulatory conservatism concerning distributions [F1,S9,S3]. Capital expenditures notably increased sharply in FY2025 indicating reinvestments potentially targeting branch modernization or digital banking capabilities necessary to enhance customer experience within their traditional markets.

The company balances growing shareholder returns with maintaining sufficiency of equity capital required both for organic loan growth accommodation as well as regulatory mandate compliance.

Competitive Dynamics: Navigating Market Challenges with Personalized Service

River Financial confronts stiff competition spanning large national banks endowed with broader geographic reach and superior scale economies; online-only banks offering cutting-edge digital platforms; credit unions benefiting from tax advantages; as well as non-bank lenders encroaching on traditional banking functions through fintech innovations [S4].

In response, River Financial leverages intimate local market knowledge demonstrated via its network of predominantly full-service branches covering all major metropolitan areas within Alabama plus one office servicing Florida Panhandle markets [S1,S23]. A "one customer at a time" philosophy promotes relationship depth which supports loyal deposit bases and mitigates competitive poaching despite scale disadvantages.

While personalized service forms an important differentiator fostering community ties often inaccessible to larger entities relying primarily on centralized processes or digital interfaces alone—it constitutes a double-edged sword as geographical concentration inherently caps growth potential outside these entrenched regions absent significant expansion or acquisition moves which themselves would require regulatory approval impacting competitive posture.

Risks: Concentration Exposure and Regulatory Environment

Concentration risk tied closely to real estate exposures introduces vulnerability especially should economic downturns erode collateral values or impair borrower repayment capacity causing upticks in nonperforming assets jeopardizing profitability given limited geographic diversification [S14,S21]. Additionally regulatory evolutions imposing tighter capital requirements or operational constraints could curb payout capacities or necessitate slower growth pacing impacting shareholder returns.

Continued careful monitoring of credit quality indicators within these concentrated segments alongside proactive portfolio stress testing remains essential.

This report is for informational purposes only and does not constitute investment advice or recommendations regarding River Financial Corporation securities.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments